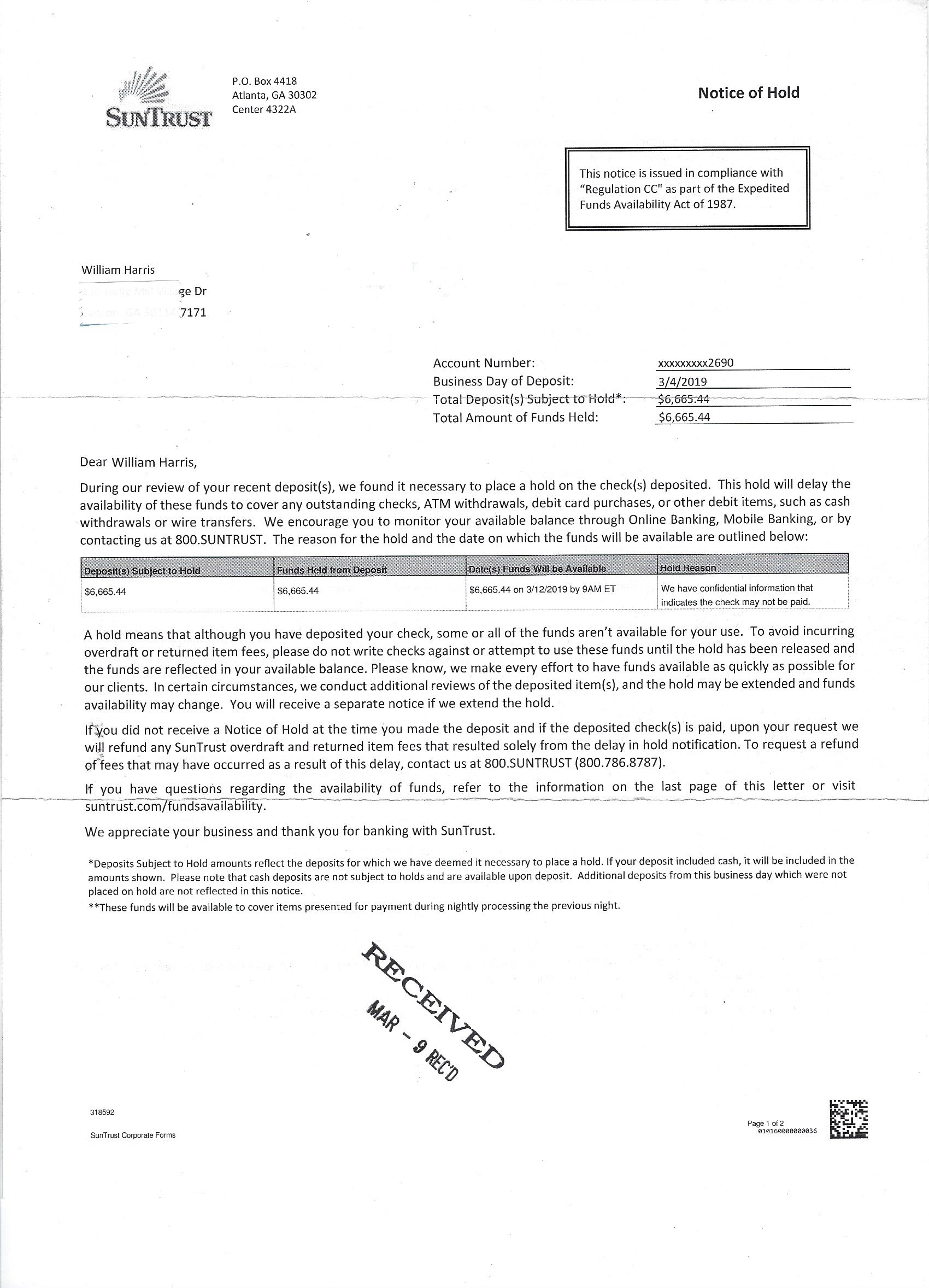

Complaint Review: SUNTRUST BANK - Internet

- Author Not Confirmed

- SUNTRUST BANK Internet United States of America

- Phone:

- Web: www.suntrust.com

- Category: Banks

SUNTRUST BANK DO NOT BANK WITH SUNTRUST!! DO NOT (TRUST) THIS BANK !! SUNTRUST RIPS PEOPLE OFF!!!! Internet

*Consumer Comment: last reply....

*Consumer Comment: Also to note...

*Consumer Comment: I am impressed...

*Consumer Comment: Steve, I get all that. Here's the problem...

*Consumer Comment: Info on those recent bank notices regarding overdrafts

*General Comment: Can't say I blame you...

*Consumer Comment: Consider my mind CHANGED on this subject...as of today...

*Consumer Comment: Don't take the "trolls"to heart...

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

To the consumer that posted a comment about my post regarding Suntrust..You do not know me nor my experiences with this Bank. And as far as being disgruntal, please give me a break. They do not pay their employees didly squat unless you are upper management. I left that horrible bank on good terms and my own decision and it defintely was not because I was let go and I have documentation to prove it and to prove everything else that I have experienced...You must be someone that works for that horrible bank to get offended by what I say..It is a horrible Bank in my opinion and have have facts to back up everything..I definitely am good with my finances..I have a good credit score and just bought a house..so do not talk or make comments about someone you do not know..I am not the only consumer that has had terrible experiences regarding their accounts regarding this Bank. And again, this bank is terrible and cheats it's customers out of money with overdraft fees....I will continue to make that claim...

This report was posted on Ripoff Report on 07/02/2010 01:48 PM and is a permanent record located here: https://www.ripoffreport.com/reports/suntrust-bank/internet/suntrust-bank-do-not-bank-with-suntrust-do-not-trust-this-bank-suntrust-rips-peopl-619571. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#8 Consumer Comment

last reply....

AUTHOR: Ronny g - (USA)

SUBMITTED: Monday, July 05, 2010

for now that is....

Like a "Where's Waldo" puzzle, can anyone find in any of the terms I posted directly from these banks websites where a "register" is even vaguely mentioned?

A 50 point reward to anyone who can find where the banks are recommending, suggesting, encouraging or implying a register is required to manage the debit card usage.

I am not trying to imply customers should not use one..as I certainly do and it is a bit of a chore since I have several accounts to manage and most are low balance.

However, is it also fair to knock the percentage of customers who were simply trusting the banks promotions and promises, and got sucked in and fleeced?

#7 Consumer Comment

Also to note...

AUTHOR: Ronny g - (USA)

SUBMITTED: Monday, July 05, 2010

I don't know about all banks..but I have certainly posted on this site bank debit card promotions...which typically state to the effect that the debit card SHOULD be used for small every day purchases..AND that it is convenient because you won't have to carry any change..and it SHOULD be used in lieu of cash or checks..

Better yet..I will copy and paste from several bank websites...Bank of America, Wachovia, Suntrust, US Bank to name a few..read the terms and tell me the banks are not explicitely encouraging new customers to use these for everything, and depend on online banking to be accurate. How is this justified?

Pay for all types of purchases quickly and easily.

Just use your Visa Debit card when you are ready to pay. It works fast, so there's no need to write checks or fumble for change. Plus, you'll save on trips to the ATM and can leave your checkbook at home.

Debit card transactions are automatically deducted from your checking account and typically posted within 24 hours of your purchase. So you can check your updated balance and transaction record on your card issuer's website or by phone.

In addition, every month you'll also receive a checking account statement that details your purchases, including merchant name, location, date and amount. So it's easy to see where your money goes

* SunTrust Visa Check Cards are free with all SunTrust checking accounts

* Use it for everyday purchases at places like department stores, gas stations, grocery stores, or anywhere you see the Visa logo

* Easily view your check card transactions in your monthly statement or online in SunTrust's online banking

When you sign for your purchases, your money comes directly from your checking account, but you also get security protections that help prevent, detect and resolve fraud

- No cash: reduce or eliminate the need to carry around a checkbook or a lot of cash.

- Quick record: purchases made with a debit card where you enter your PIN will generally post the same or next day to your account.2

Check Card Overview

A Wells Fargo Check Card with ATM access makes it easy and convenient to manage, protect and reward your spending.

Take control of your finances. Securely access, monitor and track your account activity and expenses automatically in one place

* Accepted at millions of locations that accept Visa debit cards.

* Use instead of cash or checks for everyday purchases.

* Pay bills online with your U.S. Bank Check Card

How it Works

* Money is always deducted directly from your checking account.

* Check card transactions are protected by the U.S. Bank Zero Liability Policy.1

* Track purchases in Internet Banking and monthly checking account statements.

#6 Consumer Comment

I am impressed...

AUTHOR: Ronny g - (USA)

SUBMITTED: Monday, July 05, 2010

That some who I thought were unreasonable, actually are very reasonable.

For example...Edgeman stated..

"TD,Like you, I've been receiving multiple mailings from banks

encouraging me to sign up for overdraft protection. I just stick them in

the shredder as I don't need the service. After all, why on Earth would

I authorize a transaction that would result in a negative balance? I

can't think of any reason to do so."

The underlined, pretty much says it all.

Now more then ever, the banks are showing their true colors, just that some of us who were unfortunate enough to suffer from it, have been met with opposition for simply lodging a report.

Here is a recent notice I received from one of my banks, I have plenty of others as well but this is most recent.....

You are not opted in for over the credit limit coverage

Help to Avoid Declined Transactions.

In the event you have to use your credit card for unexpected reasons that could bring you over your allowable credit limit, Over the Credit Limit Coverage may allow you to avoid having transactions declined.

To learn more visit the Customer Service tab to request Over the Credit Limit Coverage. If you request Over the Credit Limit Coverage, you will receive a confirmation of your request.

You can remove this coverage at anytime by visiting the Customer Service tab in your online account, then click Request/Cancel over the credit limit coverage or by calling the Customer Service number on the back of your card.

If you have any questions, click here to contact us.

Sign up today

"request over the limit coverage" "remind me later"

Now why would the bank be "encouraging" anyone to have this coverage? nah..the banks do anything wrong?

Even though time and time again I stated that customers need to be responsible for keeping a register, I was still called an advocate of irresponsibility. Yes, I am passionate about the matter and may over react, but the bottom line here to many, is the banks simply want to fleece customers due to human error, and encourage this error in anyway possible, INCLUDING.. promoting online banking as a great way to manage the account.

In addition, since there seems to be no regulations as far as I can find regarding how much and for how long a merchant can hold an authorization charge, which can certainly result in overdrafting since this is done without the consumers knowledge or consent, how can the register defense possibly hold up in every case? And if it can't hold up in every case, the defense may not work at all in a class action suit.

#5 Consumer Comment

Steve, I get all that. Here's the problem...

AUTHOR: Truth Detector - (USA)

SUBMITTED: Monday, July 05, 2010

No one has had your back more than me during these discussions. I STILL maintain that any moron who refuses to manage his/her account in a responsible fashion deserves NO sympathy from us, the bank, or anyone else when fees are assessed.

But what I am receiving in the mail runs 100% contradictory to what these same banks have communicated in the past regarding overdraft protection i.e. overdraft fees...and there is no regulated, mandated verbiage required during the notification process of this opt-in/opt-out process.

How do I know this? Today, the bank I use to save for my kids' college notified me via email in the following manner:

Beginning August 15, 2010, no fees will be imposed on ATM or everyday debit card overdraft transactions if you have opted out of Huntington Debit Overdraft Service. If you havent already told us yes to Huntington Debit Overdraft Service, your existing service will end on August 15. If you opt in, fees may be imposed for covering overdrafts created by check, in-person withdrawal, ATM transaction, debit card purchase or other electronic means.

Now, compare that to THIS notice - courtesy of a completely different bank:

You will lose the ability to withdrawal cash at the ATM in the event of an emergency or experience the inconvenience or embarrassment of being denied for everyday purchases made with your debit card, like groceries or gas, when your account does not have sufficient funds.

The issue here is the verbiage and rationale used to sell the service. For years, banks and credit unions have sold the service to consumers predicated on its ability to save salient, large-scale transactions (i.e. Would you rather that rent check bounce?). Now, when consumers are about to be opted out by default on August 15, they are singing a song about "convenience" and "embarrassment", as though the $35 fee for each item and having to borrow money from a payday lender after the fees were taken wasn't embarrassing in the first place.

I'm sorry, but I'm not buying the communications from these people. Debit cards will STILL be convenient. Debit cards will NOT be prohibited from use. Rent checks will STILL be accepted - and if they result in an overdraft, they will be assessed ONE fee (unless there are other checks or ACH transactions that come through). What will cease are the endless numbers of debit card overdrafts...and by virtue of these mailings, it is appallingly clear THAT is what the banks are worried about, not "convenience" or "embarrassment".

...and before you or anyone else tries the "Gee, if they just kept an account register..." talking points, SAVE THEM. I have uttered them more than anyone knows on this site. That isn't the issue here. Honest, consistent and forthright disclosure regarding overdraft protection IS.

#4 Consumer Comment

Info on those recent bank notices regarding overdrafts

AUTHOR: Steve - (U.S.A.)

SUBMITTED: Monday, July 05, 2010

Those notices that everyone has been recieving regarding the opt in or opt out of overdraft protection were mandated by recent changes to federal law.

They have absolutely nothing to do with bank policy.

Just federal law.

#3 General Comment

Can't say I blame you...

AUTHOR: Edgeman - (U.S.A.)

SUBMITTED: Sunday, July 04, 2010

TD,

Like you, I've been receiving multiple mailings from banks encouraging me to sign up for overdraft protection. I just stick them in the shredder as I don't need the service. After all, why on Earth would I authorize a transaction that would result in a negative balance? I can't think of any reason to do so.

No doubt that overdraft fees have been a boon to the banks- I've written as much here at ROR. However, these are fees that are so easily avoided. Every bank account agreement that I have in my home tells you that they may authorize transactions that will result in a negative balance and the bank will most likely process from highest-to-lowest (or any order).

Knowing this, wouldn't it be prudent to stay within one's available balance?

I know you still advocate responsibility and it's a point I've been making for years. Read a bank agreement and know what it says. If the bank agreement is not to your liking, walk away without signing it.

If you sign it, be aware of your available balance and your transactions. I cannot think of a good reason for not keeping track of one's finances.

#2 Consumer Comment

Consider my mind CHANGED on this subject...as of today...

AUTHOR: Truth Detector - (USA)

SUBMITTED: Sunday, July 04, 2010

Before I begin, I would like first to make clear the fact that I am in no way retreating from my position that EVERY checking account holder should ALWAYS keep an accurate and current check register. The responsibility for your account is YOURS - regardless of what the bank does or doesn't do.

That being said, I have come to the conclusion that banks and credit unions have misrepresented themselves and misrepresented positions to consumers where overdraft protection is concerned...and I have come to this conclusion via their own communications with me, their customer.

Verbiage from BOTH the local credit union and the bank (curiously congruent) trying to convince me that I should opt into their overdraft protection:

You will lose the ability to withdrawal cash at the ATM in the event of an emergency or experience the inconvenience or embarrassment of being denied for everyday purchases made with your debit card, like groceries or gas, when your account does not have sufficient funds.

Now wait just a d**n minute...wasn't the previously-stated reason for overdraft protection that the larger items - like rent, mortgage payments, etc. - would be allowed to clear? What the hell is this "inconvenience" and "embarrassment" nonsense?

In the past, my banks and credit unions have always maintained that I should build an emergency fund via THEIR savings accounts (which I have) and that I shouldn't use my debit card for everyday purchases (After all, those little debit transactions add up fast. Withdrawing money via the ATM within the available balance has ALWAYS been the key to "everyday" transactions if one is to avoid the overdraft).

I have been a responsibility advocate for years on this site - and I will continue to be. But in my estimation, banks and credit unions have exposed their motives with their desperate attempts to convince me to opt into their overdraft protection programs. Ergo, I no longer support them or their obvious attempt to siphon money from consumers in lieu of what they had previously stated was their goal with overdraft protection: to protect the American consumer.

#1 Consumer Comment

Don't take the "trolls"to heart...

AUTHOR: Ronny g - (USA)

SUBMITTED: Friday, July 02, 2010

I am often accused of being a troll myself. But the internet and blogging and forums are really new to our culture. So the definitions and terminology are open for debate, and some psychological factors can be taken into consideration.

Here is how many currently define it..

Trolls

Essentially, a troll

is a person who posts with the intent to insult and provoke others. The goal is to disrupt/divert a discussion or topic beyond repair. They often target new users, who

are more likely to take offense, hence the term "troll" (as in

"trolling" for newbies). I was introduced to this sector of society myself from lodging a report here against bank tactics. Since then I have been following similar reports on this site, and defending those who are victims to these trolls, at the expense of being called a troll myself. So if I am to be considered a troll, I am okay with that..as long as it is known that I am actually trolling for trolls, the "anti-troll" if you will.

Many trolls are characterized by having an excess of free time and are probably lonely and seeking attention. They often see their own self-worth in relation to how much reaction they can provoke.

Trolls can be categorized in the following ways:

- Spamming troll: Posts to many newsgroups with the same verbatim post.

- Kooks: A regular member of a forum who habitually drops comments that have no basis on the topic or even in reality.

- Flamer: Does not contribute to the group except by making inflammatory comments.

- Hit-and-runner: Stops in, make one or two posts and move on.

- Psycho trolls: Has a psychological need to feel good by making others feel bad.

I could name names, but it is self evident to those who frequent this site.

I personally am torn between the fact that there really are no moderators here to police this forum from the disruptive topic diverting kooks and flamers, but at the same time I strongly feel it is an asset to this forum that all are allowed to post freely and the posts and replies will not be edited or deleted.

Yes, we have to take the good with the bad. Many do not like that I devote free time to this site and point out when someone is being one of the above, but what does have me concerned, is that a site like this that actually can and does do something to help consumers rights, business rights and victims of scams and ripoffs, that these types of trolls are potentially taking away credibility of this site.

But truth often prevails, at least to those that can see and appreciate the truth, for whatever it is worth these days.

Related Reports

09:06 PM

11:29 PM

11:31 PM

12:17 PM

08:04 AM

10:38 AM

06:54 AM

02:30 PM

12:08 PM

09:36 AM

02:39 PM

Advertisers above have met our

strict standards for business conduct.