Complaint Review: Freedom Life Insurance Company of America - Fort Worth Texas

- Author Not Confirmed

- Freedom Life Insurance Company of America 300 Burnett St Fort Worth, Texas USA

- Phone: 855-648-6789

- Web: http://www.ushealthgroup.com/

- Category: Health Insurance

Freedom Life Insurance Company of America US Health Group Medical or Health Insurance that does not pay for checkups and preventative maintainance Fort Worth Texas

*Author of original report: The insurance agent did say to use my insurance for wellness

*UPDATE Employee: Did you ask the right questions?

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

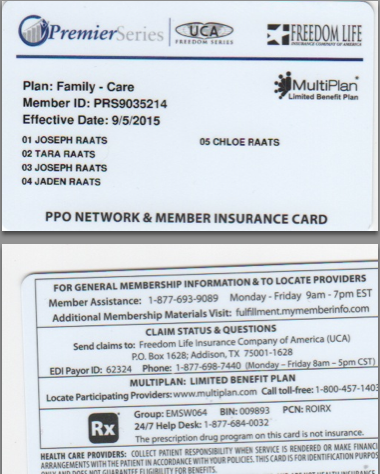

For People getting a call from any sales person selling "FREEDOM LIFE INSURANCE COMPANY OF AMERICA" OR "US HEALTH" PLEASE STAY AWAY FROM THEM!!! If you plan to use them like Health insurance from employement or some other popular Insurance such as Aetna, Blue Cross, Blue Shield or Humana they do NOT work that way! This insurance only covers if you get Ill or sick. it is not for Preventative Maintanence for doctor checkups on your bloodwork, chloestrol, blood sugar etc. I had enrolled thinking I was getting this kind of insurance and the sales reps who call have a push attitude. Unforntuantly my sales resp had passed away and she cannot help me. If you received a call before from 754-281-0223 from Stacy Eidows stay away from it!. I now owe $420 to Northwestern Hospital if not more on insurance that did not cover this for just checking myself out if I am ok or not versus I have to get sick and use this insurance. Find some other Legit Affordable Health Insurance if you are trying to bypass Obamacare on your IRS taxes.

This report was posted on Ripoff Report on 06/25/2015 11:01 AM and is a permanent record located here: https://www.ripoffreport.com/reports/freedom-life-insurance-company-of-america/fort-worth-texas-76102/freedom-life-insurance-company-of-america-us-health-group-medical-or-health-insurance-tha-1237946. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#2 Author of original report

The insurance agent did say to use my insurance for wellness

AUTHOR: - ()

SUBMITTED: Monday, July 06, 2015

So yes that is what was going on. She even told me to ignore the paper statements coming in the mail. I had followed up to find out she passed away and when I called someone else they said I was responsible. Had I known again I would NOT have signed up for such a phoney health insurance.

#1 UPDATE Employee

Did you ask the right questions?

AUTHOR: numberoneinspro - (USA)

SUBMITTED: Monday, July 06, 2015

Dear insured,

It is unfortunate that you feel this way and I understand how frustrating it can be to find out crucial information after the fact. Easily understood how you may feel mislead but that does not make the insurance policy you were sold a rip off. I cannot speak for every agent, however; every agent that I know and that is a lot of agents being one myself, prides them self on the benefit they can bring to those less informed about the whole healthcare industry. Things are changing faster than any "reasonable person" can keep up with and that is why you have an insurance agent; much like a lawyer is there to help with interpreting the law. We as agents, have to be licensed to work in this industry; which, among other things forces us to be knowledgeable about our products and to operate within a set code of ethics or potentially face the loss of our license to do business.

That being said I have to ask, did you ask your agent specifically about the “wellness visit” benefits while completing your application or call him or her before engaging in the activities you have referenced in you "gripe session"? If you did and were misled then you have a legitimate complaint and the agent that misled you should be reprimanded or at least reeducated on what he or she is selling. However, if you did not and you only "assumed" that you were covered then you have NO reason to complain! You not only had the opportunity to ask questions you have been issued a policy, the legal contract, for your specific policy which has included, in very precise language, all of the inclusions and exclusions related to that specific policy. Even though the language is mostly standard it has been reviewed by countless lawyers and approved by the State's Insurance Commission before ever being released. That is required for all insurance materials intended to be released to the public by any means available. Therefore, it is more likely you have made an assumption based on incorrect information. Understandable as we all do it from time to time.

Here is what you should have been told. . .

What is insurance? Insurance simply put is risk sharing. If I insure one person there is risk; however, if I insure more than one person statistically the risk goes down. Much like the old adage "lightning never strikes twice in the same place" would be referring to the same principle. Well it is easy to see how that makes sense when you enroll more people the risk should go down; however, that makes one critical assumption; that everyone has the same likelihood of having a need for service. That is simply not the case. Unless you prequalify the people you are allowing to join your group there is no way of determining the associated risk of the individuals enrolled. When you retain the service of an insurance company, and this used to be true for all types of insurance, there is a little thing called underwriting; it is the process or estimating your risk.

What does this have to do with wellness visits?

Well let me explain further, the premiums you are charged for your insurance policy are based, in the real world, largely on this estimated risk. The other part of the charge is based on the services provide. Agreed, pretty easy to see that to be true. What ACA plans do is charge premiums based on the highest risk for all to make it possible to offer insurance to everyone with or without any medical history or medical conditions and they are very proud to tell you so! You hear it all the time, "we think everyone deserves healthcare," and so they do. I sincerely think that is great; however, what I am not particularly interested in paying premiums at the highest possible rates to support others that have higher risk. You see the ACA plans can afford to make a big deal out of visiting the doctor when there is only a preventative desire to do so because they can afford to. They charge the highest rates with huge deductibles, the typical Bronze plan deductible starts at $5000.00, and then require you to pay a co-pay of 80/20, 70/30 or even the latest co-pays since Obamacare went into effect of 60/40 or even 50/50; meaning even after you pay the huge deductible you still have to pay your percentage of the rest. The reason for both the deductible and the co-pay is to avoid “sticker shock” if you will. If there were neither of these and you had to pay the full amount it actually costs to include these “wellness visits” in the plan you would look at those benefits in a new light.

Statistically 97.6% of all insureds never reach their deductibles in any given year. So the ACA plans charge significantly higher premiums, many times nearly double, and then pay out next to nothing in most cases except for those occasions when you visit your doctor well. We are lead to believe this is to save us all from some unseen illness, and maybe it is, but maybe the real reason is only selfish in nature only meant to serve as a preventative reason for ACA to reduce paid benefits. It is true early detection IS a major issue in continuing good health and I believe everyone MUST take all preventative steps to avoid any and all potential illness. However, if my much more affordable private insurance, like with Freedom Life, saves you hundreds or even thousands of dollars a year, depending on how many are included in your policy, wouldn't it seem frugal to put aside some of that savings to cover your required checkups when you are not actually ill? If you do not agree with that then you are most likely a person who cannot wait for a tax return failing to realize it is only money that was yours to begin with, that the government over charged you, and that the government has had all year to use without paying you interest.

When it comes down to the bottom line. . .

What Freedom life and many other private insurers do is prequalify individuals as they join the group, provide more comprehensive benefit coverage, and in a way that reduces excessive use or abuse. If a person is a good steward of their health insurance dollars it is easy to see the benefit of controlling how and when these dollars are spent. Things like drug abuse, mental illness, and even wellness visits are all areas of medicine that are largely ambiguous and difficult to evaluate risk as there are such a wide range of opinion, even among the professionals, for the proper use of and care for these areas of medicine. One person might think they need a wellness visit every month, trust me I have seen it, others might think once a year is perfect. One person might need ten labs and another none at all. What is important to remember is healthcare is not a God given right; it is a service and somebody has to pay for that service. How you pay is your choice. Join the ACA and enjoy your sponsored "wellness visits," a catchy phrase invented by, you guessed it, the ACA, while paying the highest premium, huge deductibles, and co-pays after all else is paid, or find a private insurer that offers a plan with real comprehensive benefits you can use, priced according to your risk group, save hundreds if not thousands of dollars a year, and keep some of your savings to pay for those necessary "wellness visits."

You still have the choice to find affordable healthcare that suits your specific needs and pay premiums commensurate to the benefits provide or purchase insurance with the highest premiums ever seen in the history of healthcare with their deductibles and co-pays to receive those wellness visits at a discount. The individuals that are more likely to choose private insurance policies like those provided by Freedom life are those that understand this principle. The principle that the government doesn't want you to know. So please, ask the questions before you use or even purchase insurance policy so you know the facts because no one likes to feel ripped off; even if they were not!

I hope that helps to understand the key reasons for the difference. Thank you for taking the time to read this post. Here’s to your success finding peace and security through the proper insurance plan for you.

Related Reports

01:01 PM

12:54 PM

11:47 AM

10:52 AM

04:40 PM

10:05 AM

04:37 PM

01:17 PM

01:54 PM

03:28 PM

Advertisers above have met our

strict standards for business conduct.