Complaint Review: Suntrust Bank - Decatur Georgia

- Author Confirmed

- Suntrust Bank South Dekalb Mall Decatur, Georgia U.S.A.

- Phone:

- Web:

- Category: Banks

Suntrust Bank uses suspicious accounting to defraud checking account holders Decatur Georgia

*Consumer Comment: Actually this bill...

*Consumer Comment: Overdraft Programs

*Consumer Comment: Times are changing, Edward...Get a load of this...

*Consumer Comment: Yes Posting Order is Irrelevant....

*Consumer Suggestion: Order of debits isn't relevant if you maintain a sufficient balance.

*Consumer Comment: The Great Myth

*Consumer Comment: All Banks Are The Same

*Consumer Suggestion: Dave, a real simple solution here!

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

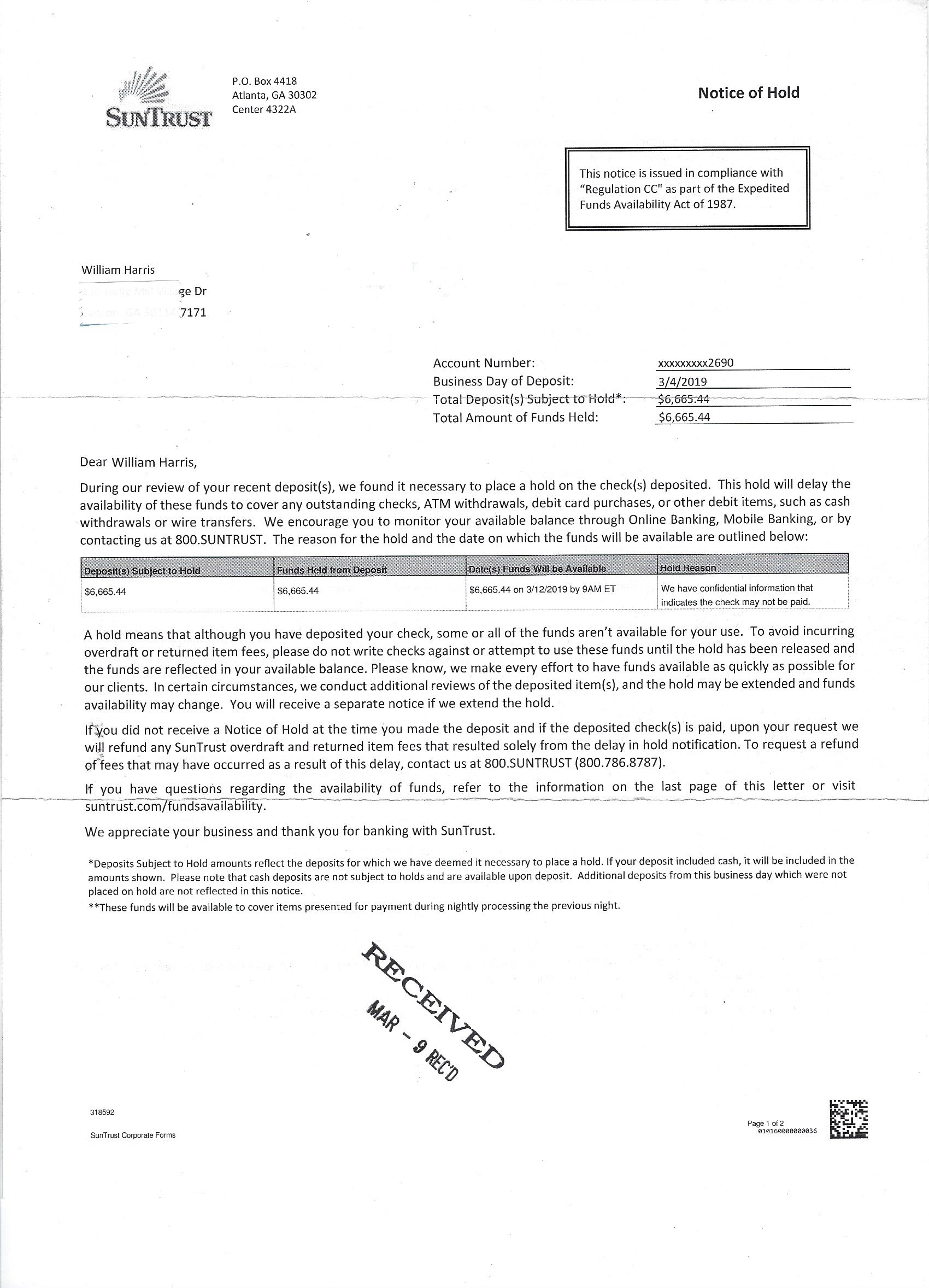

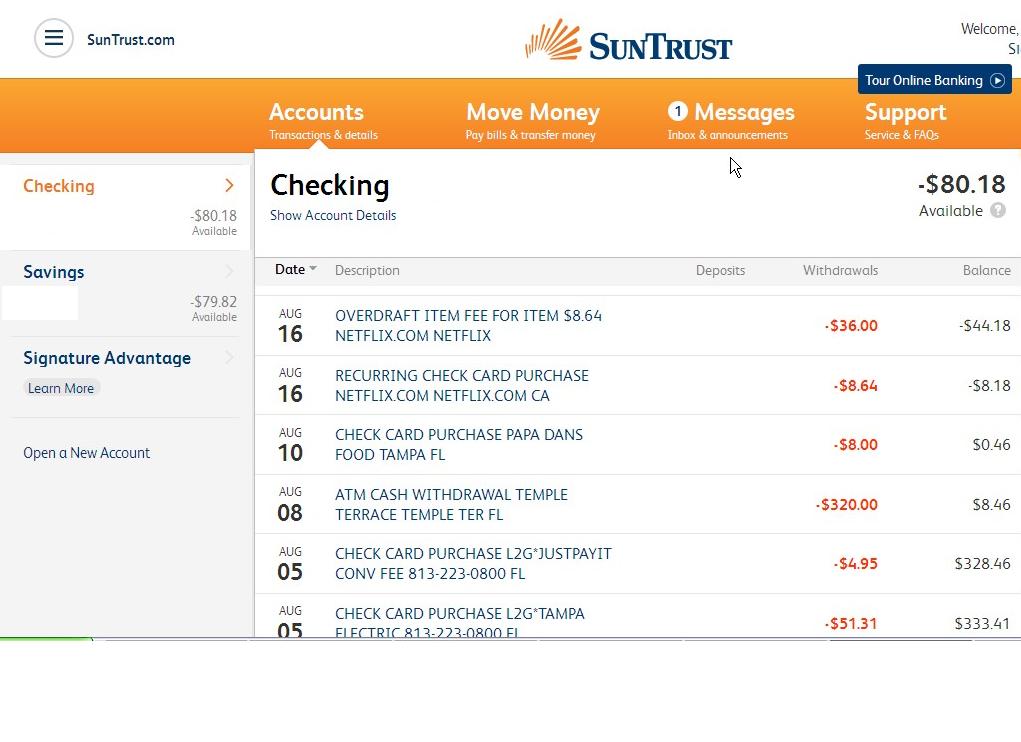

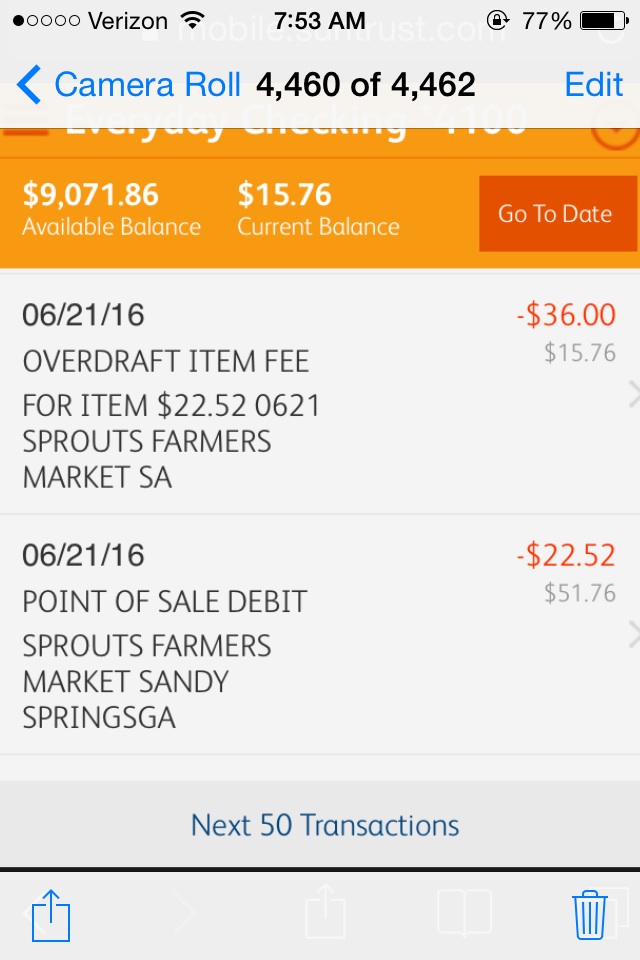

Suntrust Bank and I have heard that others do it as well, but I only have actual experience with Suntrust. When an account go nsf, the bank holds electronic transactions and small debits to your account and Processess the largest transactions first. The time span varies with slightly with the posting deadline, ie weekday or weekend, but they post the largest transactions so they can charge you a $35 fee for each of the smaller ones.

Example. I wrote a check for $100 and did not log in in the register. Later that week when the check was posted to the account, I watched as they withdrew 8 minor transactions and processed the check. Then they reprocessed the small transactions, $3.95, $8,00, $14.75, $22.00, $5.50, $6.69, $10 and $5.79 and charged me $35 each. Count them, They charge me $280 rather than process charge me $35 for the check, which by the way came in last.

I had verified the balance earlier that day to see if I had enough to make a purchase. I decided not to make the purchase because the balance was low. On my electronic statement, the check had not been presented. The following day, I watched as they withdrew my paid debits, posted the check and then paid the electronic debits again and charged me $35 each time. Letters to everyone in the bank here in Atlanta, in Florida and two other cities yielded no positive results.

the first time it happened, it was only one fee. But the second time, I saw the technology in action and closed my account. We are still in dispute about the debt.

Dave

Decatur, Georgia

U.S.A.

This report was posted on Ripoff Report on 03/26/2009 12:16 AM and is a permanent record located here: https://www.ripoffreport.com/reports/suntrust-bank/decatur-georgia-30034/suntrust-bank-uses-suspicious-accounting-to-defraud-checking-account-holders-decatur-georg-437767. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#8 Consumer Comment

Actually this bill...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Tuesday, March 31, 2009

only deals with overdraft protection transfer fees. If passed in it's present form then the customer must in writing request overdraft protection and any fees associated with the transfer of money to cover overdraft items must be disclosed to the customer. The banks that I know of that have overdraft protection already require the customer to request it. This would just create another form the customer was asked to sign when opening the accounts that they would then claim to have never seen. It won't have any effect on OD fees, processing order, items returned, etc. Only the protection transfer fee. Basically 'do you want to authorize a $10 fee to transfer money each time to keep from being charged $35 per item that is returned or paid into a negative balance?'

#7 Consumer Comment

Overdraft Programs

AUTHOR: Ken - (U.S.A.)

SUBMITTED: Tuesday, March 31, 2009

The proposed legislation is a little bit of a red herring. It has no real benefit to the consumer. If a bank or credit union decides to allow a certain dollar amount in which they will pay a check rather than returning it, they charge the same fee that they would charge if they returned the check unpaid.

So, if I bounce a check, my options are to have it paid and assessed a $35 fee, or to have it returned and be assessed a $35 fee.... plus whatever I am going to get charged on the other end by whoever got the bounced check back.

Pretty much any financial institution that offers this service has an opt-out request. They question is why would you want to opt out? You don't want to make the incorrect assumption that if you opt out that your debit card will be declined when you are overdrawn. It won't, that's not the way the system was designed.

#6 Consumer Comment

Times are changing, Edward...Get a load of this...

AUTHOR: Truth Detector - (U.S.A.)

SUBMITTED: Monday, March 30, 2009

The Consumer Overdraft Protection Fair Practices Act is back!

Yep, Rep. Carolyn Maloney (D-NY) has re-introduced this legislation - which would require full disclosure of all bank overdraft programs and advanced consumer consent i.e. no more automatic enrollment/NSF's.

This isn't 2007, when this sort of legislation was last introduced. Banks and their so-called 'credibility' have taken a deep plunge into the sewer - and the fact that many of them are now on federal welfare means they are pretty much beholden to PUBLIC interests, not their own. Something tells me that legislation aimed at allowing customers to preempt overdraft protection (NSF fees, that is...), thus saving customers billions and forcing banks to make money in an honest manner, will be very well received this time around now that Bush isn't there to veto the legislation when it passes congress...

#5 Consumer Comment

Yes Posting Order is Irrelevant....

AUTHOR: Edward - (U.S.A.)

SUBMITTED: Sunday, March 29, 2009

if you maintain a sufficient balance.

So why did the banks all CHANGE their policies to this new order of posting large items first to suit those who risked bouncing their mortgage auto loan checks?

#4 Consumer Suggestion

Order of debits isn't relevant if you maintain a sufficient balance.

AUTHOR: I Am The Law - (U.S.A.)

SUBMITTED: Friday, March 27, 2009

Ok, let's do some thinking here.

First off, if you write a paper check, the bank doesn't know about it until it's presented to them for payment. That's common sense, I'd hope. From your story, you'd apparently used your card to purchase some other things while that check was still outstanding and there wasn't enough money to pay for everything. So, when the check finally rolls in, surprise, there's not enough money in the account. Dude, that's your bad accounting, not the bank's.

Second, I'm pretty sure that all banks apply credits first, and then take large debits down to small debits. This is the way it should be. Large debits are typically more important than small ones. If your account is short, wouldn't you rather have your mortgage or car payment considered before things like a $10 check you wrote to your local grocery store? I know I would. Now, granted, since people typically have many more small transactions post to their account than large ones, by default this would cause more fees. No arguement there. However, you still need to consider that all this isn't relevant if you maintain a sufficient balance and avoid respending money. Trust me, there is no conspiracy at your bank to gyp you out of money.

#3 Consumer Comment

The Great Myth

AUTHOR: Ken - (U.S.A.)

SUBMITTED: Thursday, March 26, 2009

It's a myth that banks hold electronic transactions. They process them on the day they come in, which has nothing to do with the day that the purchase was made. Merchants batch their electronic transactions and submit them on their own schedule. Each night, the bank is going to process all transactions that came in THAT day. They process them all at once, and in the case of your (and most commercial) bank, they process them largest to smallest.

Look at it this way, they process tens of thousands of these a day, or in the case of BoA, probably millions. WHo do you think sits and says 'hrm... I think I will set these charges aside because I think that Dave may be overdrawn later this week'?

The above points about account management are well taken. The cost of an overdraft is just too high to allow yourself to fall into that trap. One suggestion I would add is that you only use your debit card in an occasion where formerly you would have written a check. The people who use debit cards to buy coffee and gum are just plain nuts, in my humble opinion.

#2 Consumer Comment

All Banks Are The Same

AUTHOR: Jim - (U.S.A.)

SUBMITTED: Thursday, March 26, 2009

What happened to you would happen to you anywhere because you're mismanaging your finances. You have all of the classic symptoms of money mismanagement; (1) you don't keep an accurate written check register, (2) you rely on an online system to tell you your balance, and (3) you use a debit card like a credit card. People like you will always overdraft their account because you fail to exercise any proper money management skills.

If you become more diligent about your register, look at your register for your available balance, and stop using your debit card will be the steps you need to take to at least protect yourself. Oh, and no bank holds transactions - they wait for merchants to verify the transactions as legitimate. If you want to blame someone for your predicament - look in a mirror. This is all on you.

Not a rip off. Best of luck to you.

#1 Consumer Suggestion

Dave, a real simple solution here!

AUTHOR: Steve - (U.S.A.)

SUBMITTED: Thursday, March 26, 2009

Dave,

I have a real simple solution here!

Don't spend money you don't have!

No NSF fees...

And, DO NOT rely on your online banking to determine your available balance!!

This will ALWAYS get you in trouble!

Rely ONLY on your ACCURATE checkbook register.

Do not "float" transactions.

The days of "floating" are over.

FYI...Almost every bank processes transactions that way.

No rip off here...Just another case of poor account management.

Related Reports

09:06 PM

11:29 PM

11:31 PM

12:17 PM

08:04 AM

10:38 AM

06:54 AM

02:30 PM

12:08 PM

09:36 AM

02:39 PM

09:51 AM

03:00 PM

04:42 PM

07:04 PM

09:21 PM

08:12 AM

06:36 AM

01:25 PM

04:20 PM

08:20 AM

10:51 AM

01:10 PM

11:38 AM

08:32 PM

Advertisers above have met our

strict standards for business conduct.