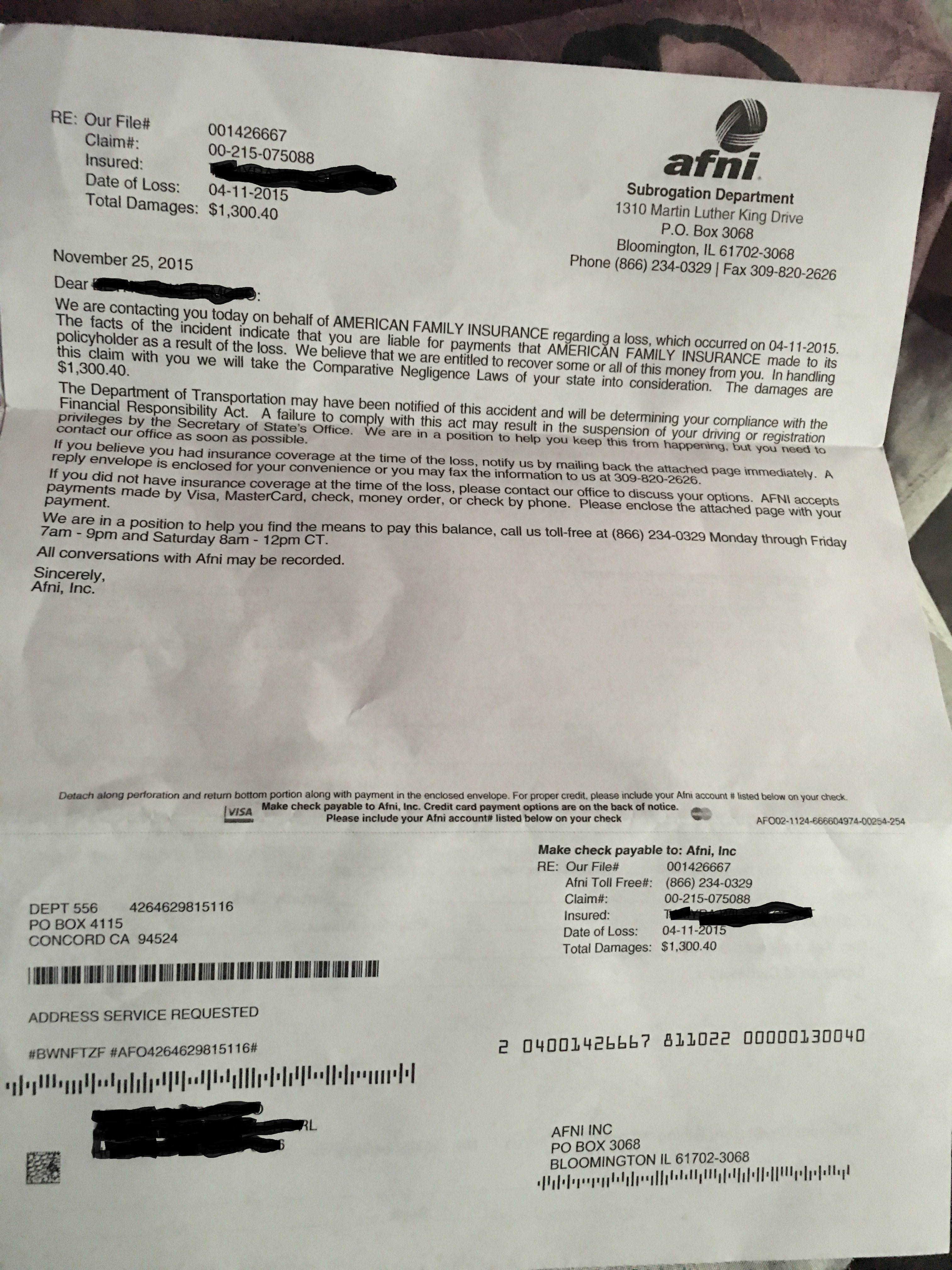

Complaint Review: AFNI - BLOOMINGTON Illinois

- Author Confirmed

- AFNI 404 BROCK DR, PO BOX 3427, BLOOMINGTON, Illinois U.S.A.

- Phone: 866-647 0885

- Web:

- Category: Collection Agency's

AFNI Collections sends collection notice for a 2001 T-MOBIL bill, a service i never had BLOOMINGTON Illinois

*Consumer Suggestion: I had the same problem and beat them.

*Consumer Suggestion: AFNI CLASS ACTION SUIT

*Consumer Suggestion: NEVER file the "fraud affidavit" as previously suggested! That is just plain stupid!

*Consumer Suggestion: Not quite right Sherri.

*Consumer Comment: ACTUALLY, UNDER FEDERAL UCC, THE STATUTE OF LIMITATIONS IS TWO YEARS....

*Consumer Comment: It's simple

*Consumer Suggestion: STAY OFF THE PHONE!!! Never speak to any third party collector / junk debt buyer!!

*Consumer Comment: RE:

*Consumer Comment: RE:

*Consumer Comment: RE:

*Consumer Comment: RE:

*Consumer Suggestion: Statute of limitations.

*Consumer Suggestion: I had the same problem...

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

AFNI sent me a collection notice for a purported T-Mobil bill. I've never been a customer of T-Mobil.

I called AFNI & was told the bill was for Omnipoint, bought by T-Mobil, & that the charge was from 2001. I've never been a customer of Omnipoint; but when I heard 2001 , and October, I became unsure (audibly). That was a hazy & difficult time for me and a lot of other New Yorkers; did I possibly??? have a cell phone company briefly??? at that time?

However, the rep ("Dave") offered no explanation as to why I had not been billed previously, and no other information about the purported account.

I almost paid just to get it off my desk--but finally said I did want to check my records first. (I was pressed as to when the payment would arrive before I hung up.)

So. no, in fact, I was never with Omnipoint. And I see AFNI has a very bad history. I am writing AFNIi a letter disputing the debt and requesting validation. I hope that will take care of it (???)

Since I see others have recently been pursued by AFNI for fake T-Mobil, I'm just sharing my story. ( . . . . Why would someone scam me for only $44.00? The 9/11 memories made this particularly nasty) I am sharing my story. It looks like T-Mobil is their latest disguise.

LR

brooklyn, New York

U.S.A.

This report was posted on Ripoff Report on 11/22/2008 05:58 PM and is a permanent record located here: https://www.ripoffreport.com/reports/afni/bloomington-illinois-61702/afni-collections-sends-collection-notice-for-a-2001-t-mobil-bill-a-service-i-never-had-bl-394048. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#13 Consumer Suggestion

I had the same problem and beat them.

AUTHOR: Dave - (U.S.A.)

SUBMITTED: Tuesday, February 10, 2009

Check out my post if you get a chance. The same thing happened to me and I beat them in court.

#12 Consumer Suggestion

AFNI CLASS ACTION SUIT

AUTHOR: Chris - (U.S.A.)

SUBMITTED: Saturday, February 07, 2009

I was also contacted by an attorney- from Illinois and I agreed to participate in the Class Action Suit. I suggest that anyone who is being harassed or have AFNI hit their credit report join the class action.

Let's put these guys out of business by busting them out through legal fees trying to defend themselves

#11 Consumer Suggestion

NEVER file the "fraud affidavit" as previously suggested! That is just plain stupid!

AUTHOR: Steve - (U.S.A.)

SUBMITTED: Wednesday, January 14, 2009

More BAD "advice" from someone who has no clue at all.

NEVER do the "fraud affidavit" thing. AND, Never call the original creditor!

The 'fraud affidavit" used by collections agencies is just a sneaky way of getting your information that they currently do not have, and will enable them in further collections activities.

Anyone who does not have the basic common sense to figure this out is a genuine moron.

And, NEVER call the original creditor or company who owns the account!

You ONLY communicate with the company who is doing the collections.

You do this ONLY in writing and ONLY by certified mail, return reciept requested.

STAY OFF THE PHONE!!

Do NOT sign ANYTHING that goes to a collector. Just print.

You see, the LEGAL BURDEN OF PROOF is on the collector to prove that you owe the money. There is no legal burden of proof on you to prove that you don't.

That's just the law.

Education is power.

Get some.

>>

Submitted: 1/10/2009 6:42:09 AM

Modified: 1/10/2009 12:56:52 PM Diochick

Bethlehem, Pennsylvania

U.S.A.

It's simple

to get the info on the account that you claim isn't yours, you would have to file a fraud affidavit with either the collection agency or the original company (in this case it would be t-mobile). I would recommend speaking with T-Mobile's risk assessment dept and they would be able to investigate whether this account is yours or not, and validate any claims. From the amount you said ($44.00) it sounds as though possibly you may have looked around at different cell phones and possibly spoke with a dealer who mistankingly activated an account in your name, but then cancelled it- but cancelled it under the wrong code, which would cause the 35.00 activation fee to still charge. If that's the case R.A. would be able to remove that charge as well.

>>

#10 Consumer Suggestion

Not quite right Sherri.

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Wednesday, January 14, 2009

The section of US code you cite is NOT the UCC. The UCC IS NOT LAW, however, every State has adopted portions of the UCC in some degree. The UCC was developed by a group of lawyers in an attempt to unify commercial law between the states, but the States decide what should be adopted into State statutes.

The section of law that you cite is not applicable to consumer telephone bills-it's for commercial enterprises and license carriers who do business with the FCC. An example would be my computer services firm providing servers for ANOTHER business that provides WEB HOSTING to consumers. If this company fails to pay their lease fees to my company, my company has 2 years to sue the hosting company that is leasing my servers.

It's a lot more complicated than this, but I'm trying to give you a simplistic example of an applicable situation.

The STATES set the statute of limitations for consumer debt, including telephone/cable TV billings.

#9 Consumer Comment

ACTUALLY, UNDER FEDERAL UCC, THE STATUTE OF LIMITATIONS IS TWO YEARS....

AUTHOR: Sherri - (U.S.A.)

SUBMITTED: Saturday, January 10, 2009

Telegraphs, Telephones, and Radiotelegraphs - 47 USC Section 415 Sec. 415. Limitations of actions

415. Limitations of actions

(a) Recovery of charges by carrier

All actions at law by carriers for recovery of their lawful charges, or any part thereof, shall be begun within two years from the time the cause of action accrues, and not after.

(b) Recovery of damages

All complaints against carriers for the recovery of damages not based on overcharges shall be filed with the Commission within two years from the time the cause of action accrues, and not after, subject to subsection (d) of this section.

(c) Recovery of overcharges

For recovery of overcharges action at law shall be begun or complaint filed with the Commission against carriers within two years from the time the cause of action accrues, and not after, subject to subsection (d) of this section, except that if claim for the overcharge has been presented in writing to the carrier within the two-year period of limitation said period shall be extended to include two years from the time notice in writing is given by the carrier to the claimant of disallowance of the claim, or any part or parts thereof, specified in the notice.

(d) Extension

If on or before expiration of the period of limitation in subsection (b) or (c) of this section a carrier begins action under subsection (a) of this section for recovery of lawful charges in respect of the same service, or, without beginning action, collects charges in respect of that service, said period of limitation shall be extended to include ninety days from the time such action is begun or such charges are collected by the carrier.

(e) Accrual of cause of action for transmission of message

The cause of action in respect of the transmission of a message shall, for the purposes of this section, be deemed to accrue upon delivery or tender of delivery thereof by the carrier, and not after.

(f) Enforcement petition

A petition for the enforcement of an order of the Commission for the payment of money shall be filed in the district court or the State court within one year from the date of the order, and not after.

(g) Overcharges defined

The term overcharges as used in this section shall be deemed to mean charges for services in excess of those applicable thereto under the schedules of charges lawfully on file with the Commissio

#8 Consumer Suggestion

STAY OFF THE PHONE!!! Never speak to any third party collector / junk debt buyer!!

AUTHOR: Steve - (U.S.A.)

SUBMITTED: Saturday, January 10, 2009

LR,

This is the FIRST and MOST IMPORTANT rule!

STAY OFF THE PHONE!!

Speaking to a third party collector / junk debt buyer will NEVER do anything positive for you, and will usually make things worse as they record these conversations and you could accidentally say something that could legally validate the debt..

And, NEVER call an "original creditor". Big mistake!

The legal burden of proof is NOT on YOU to prove that you do not owe the money.

The LEGAL BURDEN OF PROOF is ON THEM to prove that you do.

Communicate ONLY in writing, and ONLY by certified mail, return reciept requested. Be sure to put the certified# on the letter itself, and keep a copy of that letter for your records as it proves exactly WHAT you sent.

By the means above, simply dispute the debt, and DEMAND a full account history that itemizes all charges as well as something with your signature on it that created the alleged debt. DO NOT provide any personal information like SS#, DOB, employer, etc...and most important DO NOT sign the letter, just print.

Now, with this done, BY LAW all collections must cease immediately until they prove the debt is valid.

Have fun with these idiots, then sue them for your damages for the bogus collections attempt.

#7 Consumer Comment

It's simple

AUTHOR: Diochick - (U.S.A.)

SUBMITTED: Saturday, January 10, 2009

to get the info on the account that you claim isn't yours, you would have to file a fraud affidavit with either the collection agency or the original company (in this case it would be t-mobile). I would recommend speaking with T-Mobile's risk assessment dept and they would be able to investigate whether this account is yours or not, and validate any claims. From the amount you said ($44.00) it sounds as though possibly you may have looked around at different cell phones and possibly spoke with a dealer who mistankingly activated an account in your name, but then cancelled it- but cancelled it under the wrong code, which would cause the 35.00 activation fee to still charge. If that's the case R.A. would be able to remove that charge as well.

#6 Consumer Suggestion

Statute of limitations.

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Saturday, January 10, 2009

Just so you know, the statute of limitations for this type of debt is 6 years.

IF anyone should file a suit against you for this, an expired SOL is an affirmative defense against the suit.

#5 Consumer Comment

RE:

AUTHOR: John - (U.S.A.)

SUBMITTED: Friday, January 09, 2009

Send a letter via Certified Mail + Return Receipt to AFNI stating:

Per the Fair Debt Collection Practices Act, I am requesting written validation of this alleged debt, which includes:

- a copy of the original signed contract with my signature

- validation of the original "Date of Delinquency" for this alleged debt

- validation of the "Date of Last Activity" for this alleged debt

- validation that this alleged debt is within the statute of limitations.

Per the Fair Debt Collection Practices Act, the burden to validate the debt falls on the debt collector. It is not my responsibility to validate this alleged debt for you.

Receipt of this letter is being officially time stamped per the USPS.

===============================

If this fails...file complaint with the central Illinois BBB and the Illinois Attorney General...AFNI is located in Illinois

#4 Consumer Comment

RE:

AUTHOR: John - (U.S.A.)

SUBMITTED: Friday, January 09, 2009

Send a letter via Certified Mail + Return Receipt to AFNI stating:

Per the Fair Debt Collection Practices Act, I am requesting written validation of this alleged debt, which includes:

- a copy of the original signed contract with my signature

- validation of the original "Date of Delinquency" for this alleged debt

- validation of the "Date of Last Activity" for this alleged debt

- validation that this alleged debt is within the statute of limitations.

Per the Fair Debt Collection Practices Act, the burden to validate the debt falls on the debt collector. It is not my responsibility to validate this alleged debt for you.

Receipt of this letter is being officially time stamped per the USPS.

===============================

If this fails...file complaint with the central Illinois BBB and the Illinois Attorney General...AFNI is located in Illinois

#3 Consumer Comment

RE:

AUTHOR: John - (U.S.A.)

SUBMITTED: Friday, January 09, 2009

Send a letter via Certified Mail + Return Receipt to AFNI stating:

Per the Fair Debt Collection Practices Act, I am requesting written validation of this alleged debt, which includes:

- a copy of the original signed contract with my signature

- validation of the original "Date of Delinquency" for this alleged debt

- validation of the "Date of Last Activity" for this alleged debt

- validation that this alleged debt is within the statute of limitations.

Per the Fair Debt Collection Practices Act, the burden to validate the debt falls on the debt collector. It is not my responsibility to validate this alleged debt for you.

Receipt of this letter is being officially time stamped per the USPS.

===============================

If this fails...file complaint with the central Illinois BBB and the Illinois Attorney General...AFNI is located in Illinois

#2 Consumer Comment

RE:

AUTHOR: John - (U.S.A.)

SUBMITTED: Friday, January 09, 2009

Send a letter via Certified Mail + Return Receipt to AFNI stating:

Per the Fair Debt Collection Practices Act, I am requesting written validation of this alleged debt, which includes:

- a copy of the original signed contract with my signature

- validation of the original "Date of Delinquency" for this alleged debt

- validation of the "Date of Last Activity" for this alleged debt

- validation that this alleged debt is within the statute of limitations.

Per the Fair Debt Collection Practices Act, the burden to validate the debt falls on the debt collector. It is not my responsibility to validate this alleged debt for you.

Receipt of this letter is being officially time stamped per the USPS.

===============================

If this fails...file complaint with the central Illinois BBB and the Illinois Attorney General...AFNI is located in Illinois

#1 Consumer Suggestion

I had the same problem...

AUTHOR: Dave - (U.S.A.)

SUBMITTED: Friday, January 09, 2009

Do a google search for AFNI and T-Mobile. My report will be the first one to pop up. AFNI and T-Mobile both refused to give me validation of debt. T-Mobile is clueless. They pulled the same stunt. From what I read on here all the cellphone companies do this. If you need help, contact me, I will give you some advice and what I did and what others have told me. This was a good learning experience, but at OUR expense.

Related Reports

07:46 AM

Wichita, Kansas

06:59 PM

09:15 AM

07:08 PM

07:57 PM

10:25 PM

10:19 AM

07:48 PM

07:53 PM

08:25 PM

07:20 PM

08:08 PM

06:17 PM

03:52 PM

04:52 PM

08:15 AM

05:33 PM

05:09 PM

06:09 AM

06:47 PM

11:33 PM

10:21 AM

09:55 PM

04:40 PM

12:06 PM

Advertisers above have met our

strict standards for business conduct.