Complaint Review: first premier bank - Internet

- Author Confirmed

- first premier bank Internet USA

- Phone: 18009875521

- Web: mypremiercreditcard.com

- Category: Credit & Debt Services

first premier bank fraudulently added over the credit line fees, which only came from their finance charges. I didn't go over! Sioux Falls, South Dakota Internet

*UPDATE EX-employee responds: Just so you know.

*Consumer Comment: You seem to have the wrong idea about credit

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

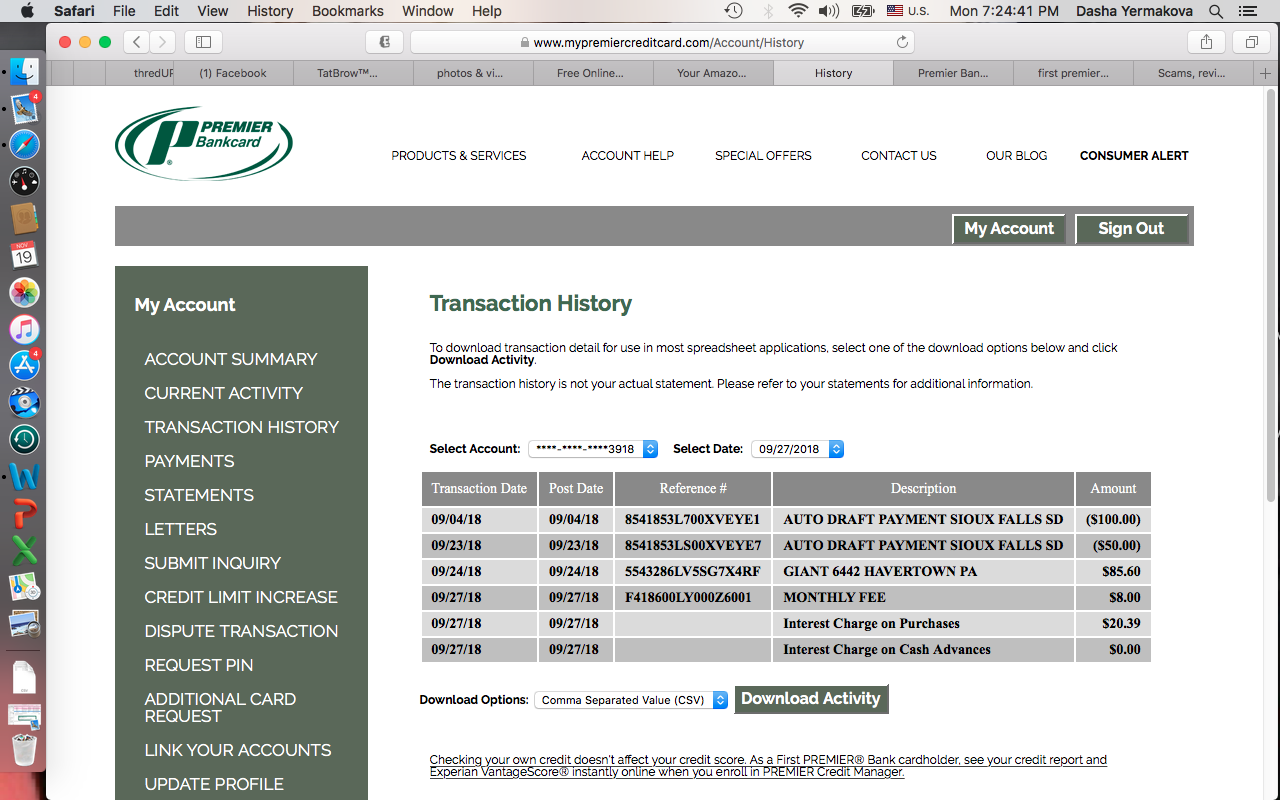

We were offered and accepted a first premier credit card. We were told there would be a $24.95 processing fee to activate the card. We paid it. This was followed by other "hidden" fees. After using the card, we paid the bill on time, every month, nearly twice the minimum payment. Still, our balance never seemed to go down, even when we stopped using the card. We decided our best option would be to close the account and just pay the balance down. Despite harassment from the customer "service" rep, we were able to close the account. Yesterday we got the first bill in the mail since closing the account. They claim the minimum payment is $137.77, which includes late fees and over the limit charge of $61.77. As the account was closed, there was NO way we went over the limit. Their fees and interest charges of $50.58 put our closed account over the limit. I have other credit cards. When their fees put us over limit, they do NOT charge us a fee. This card was primarily used for online purchases. We feel this company uses fraudulent methods to overcharge their customers and take great advantage of people who are trying to rebuild their credit. I hope this report can help to stop them! Thank you. Jess

This report was posted on Ripoff Report on 03/19/2016 12:19 PM and is a permanent record located here: https://www.ripoffreport.com/reports/first-premier-bank/internet/first-premier-bank-fraudulently-added-over-the-credit-line-fees-which-only-came-from-the-1294680. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#2 UPDATE EX-employee responds

Just so you know.

AUTHOR: TheTruth0934 - (USA)

SUBMITTED: Tuesday, September 06, 2016

I just want to give you some clarifying info.

1. They are required to send you something called a disclosure document that will detail ALL fee's that bill on the CC. IT IS YOUR responsibiltiy to read through that before you apply or start using the card.

That being said. I'll give you some info. They dont charge overlimit fee's. You went over limit because you were close to the limit of the card itself when you were billed late fee's and interest. You can tell by taking the beginning balance of your card, which is $511.19. Then add in your late fee and MSF fee. Late fee looks to be $27, Monthly Serv Fee $8.25. THEN add in interest which is $15.33. Your new balance is $561.77. All of this information I got from the bill you attached. THat means your over the limit, but they are not charging you any fees for that.

Now if you are hurting on funds, you can just pay the past due amount and current min pymnt. which would $35 plus $40 = 75. That would bring you current until interest and msf hit again the next billing cycle. The system they used adds the overlimit amount to the min pymnt. Its really a suggested amount, to help you bring the acct more under control.

The thing you need to start doing is stop using the card. I can tell just by your prev balance of 511 and some change, that you have the habit of making the min pymnt on the card, then use up the available credit from that min payment. thus you leave no room for your interest and MSF to hit, so they will knock you overlimit. the payments that you make are pointless if you use up all the available credit from that payment..

IF you want to try and get the acct under control, you need to make that 75 pymnt at the very least, then don't use for a couple months making the min pymnt, but keep in mind, the larger your payments, the better off your acct will be.

Hope that clears up a few things.

#1 Consumer Comment

You seem to have the wrong idea about credit

AUTHOR: Robert - (USA)

SUBMITTED: Sunday, March 20, 2016

First off ALL of their fees and the Interest rates are disclosed when you apply for a card. This is FEDERAL law and they are not going to fail to disclose them, this is just a case of you failing to read them. If you got the offer in the mail it would be included in that and when you signed the application you also stated you read and agree to them, if you went on-line it would most likely be in a form of a link that is on the same page they require you to click/check a box that says you actually read and agree to the terms. You can't even use the "fine print" excuse as there is a standard format and it is very obvious to anyone who actually reads the fee statement.

This bank is a Sub-Prime card for people that have not proven they can handle credit. Since it is a high risk card, they charge additional fees and interest rates that other more "regular" cards do not. Now, you can come here and say that you have other credit cards so this isn't the case for you. But one statement you made shows different.

I have other credit cards. When their fees put us over limit, they do NOT charge us a fee.

- This being close to your limit and being charged various fees(Late Fees?) seems to be a regular pattern for you. So contrary to the belief you probably have or are trying to push forward, you are infact a "Sub-Prime" borrower. As people who know how to handle credit DO NOT get to the point where even if they are late that fee would not put them over the limit. Ideally you should not use more than 30% of your available credit, for the best credit, and once you get over 80% of your credit line you are considered "maxed out" which is a big negative.

Also, contrary to your belief but "closing" a credit card does not end your obligation to pay the required minimum payments, or be charged fees. As you are still subject to ALL of the terms of your card at the time of closing until your balance is zero. Only then is your credit card truly "closed".

Related Reports

07:52 PM

Pierre, South Dakota

10:14 PM

06:02 PM

10:59 AM

06:14 AM

11:10 AM

10:45 AM

07:14 AM

10:07 AM

06:51 PM

06:19 AM

03:35 PM

08:21 AM

09:42 AM

04:04 PM

01:05 PM

07:35 AM

01:15 PM

05:03 PM

04:34 PM

01:55 PM

04:55 PM

10:50 PM

12:00 PM

Advertisers above have met our

strict standards for business conduct.