Complaint Review: Optimum First - Fountain Valley California

- Author Confirmed

- Optimum First 8900 Warner Ave Fountain Valley, California United States of America

- Phone:

- Web: http://www.optimumfirst.com

- Category:

Optimum First Optimum First, Fountain Valley, CA, mishandled the processing of my loans Fountain Valley, California

*Consumer Comment: CONSUMER EXPERIENCES

*Author of original report: Optimum First does not care about contracts

*REBUTTAL Owner of company: Not Interested

*Author of original report: Rebuttal to Optimum First Rebuttal

*REBUTTAL Owner of company: Optimum First Mortgage Is An Upfront And Honest Company

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

Apparently Optimum First and the BBB/TrustLInk don't like negative reviews; my "one-star" review of Optimum First was removed from the trustlink review forum. I thought it was very "un-American" of Optimum First and Trustlink to squealch my review.

Optimum First of Fountain Valley was the first to call me after I filled out an on-line refi query. In fact, they called me within two minutes after I hit the enter key. The very first words out of the loan officer's (Robert Chavez) mouth were about how bad the competition was, specifically Quicken Loans, and suggested that I should avoid Quicken Loans.

In retrospect, I think it is very unprofessional for a business to bad-mouth its competition; after all, what goes around comes around. To make a very long story as short as possible, the loan officer did NOT know the schedule that a 5/1 ARM could increase after the first five years. In fact, he did not know that it could increase 5% in the sixth year. I asked the loan officer several times, "What is the max increase per year," and he repeatedly said "2% per year."

Well, I was ok with his answer, but I thought it might be a good idea to take another look at the disclosure statement. Albeit, in very confusing language, the lender's disclosure statement said it could increase 5% in the sixth year, regardless of what the Libor or rates in general do. Since my average length of loan is well over seven years, I wisely decided to cancel the loan.

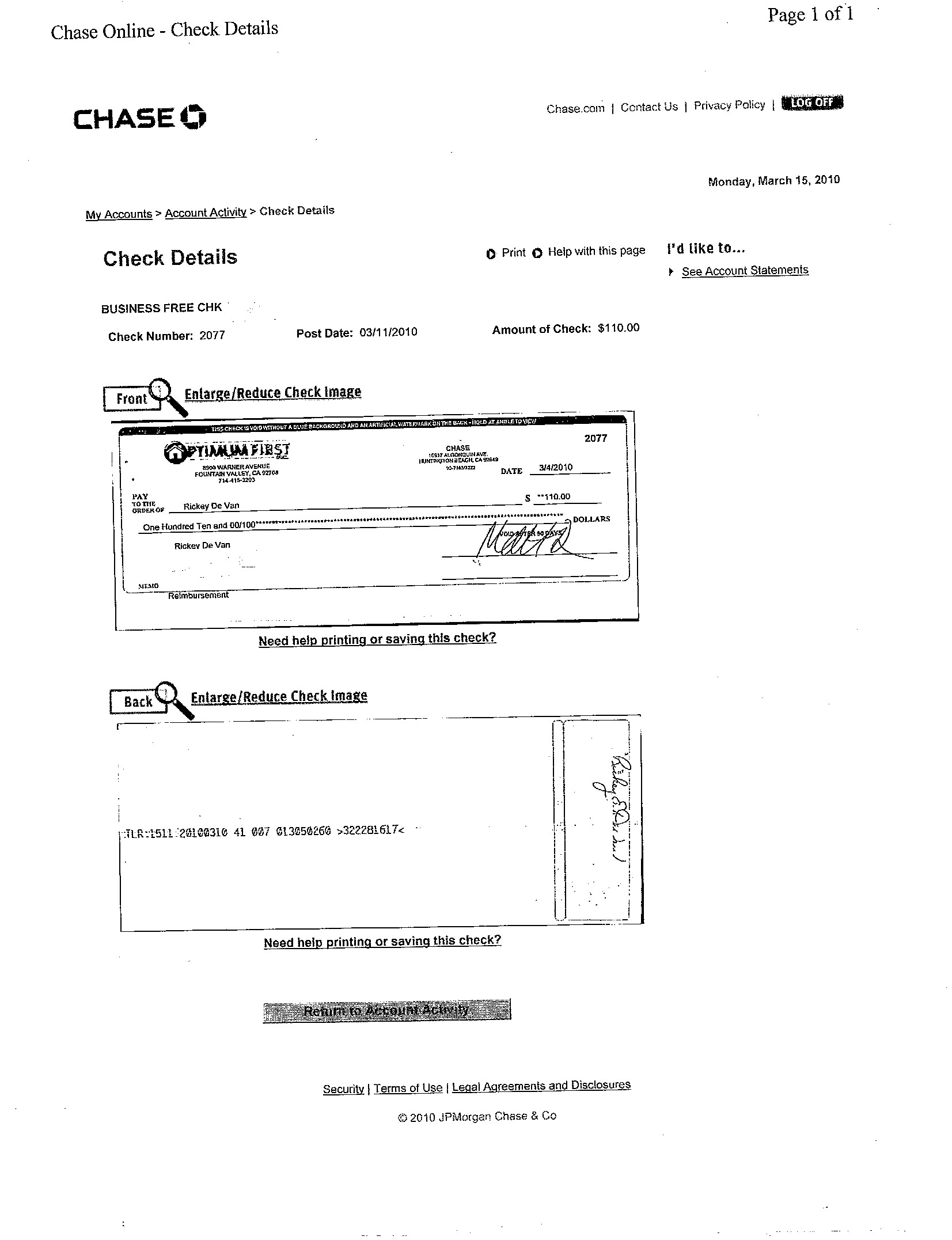

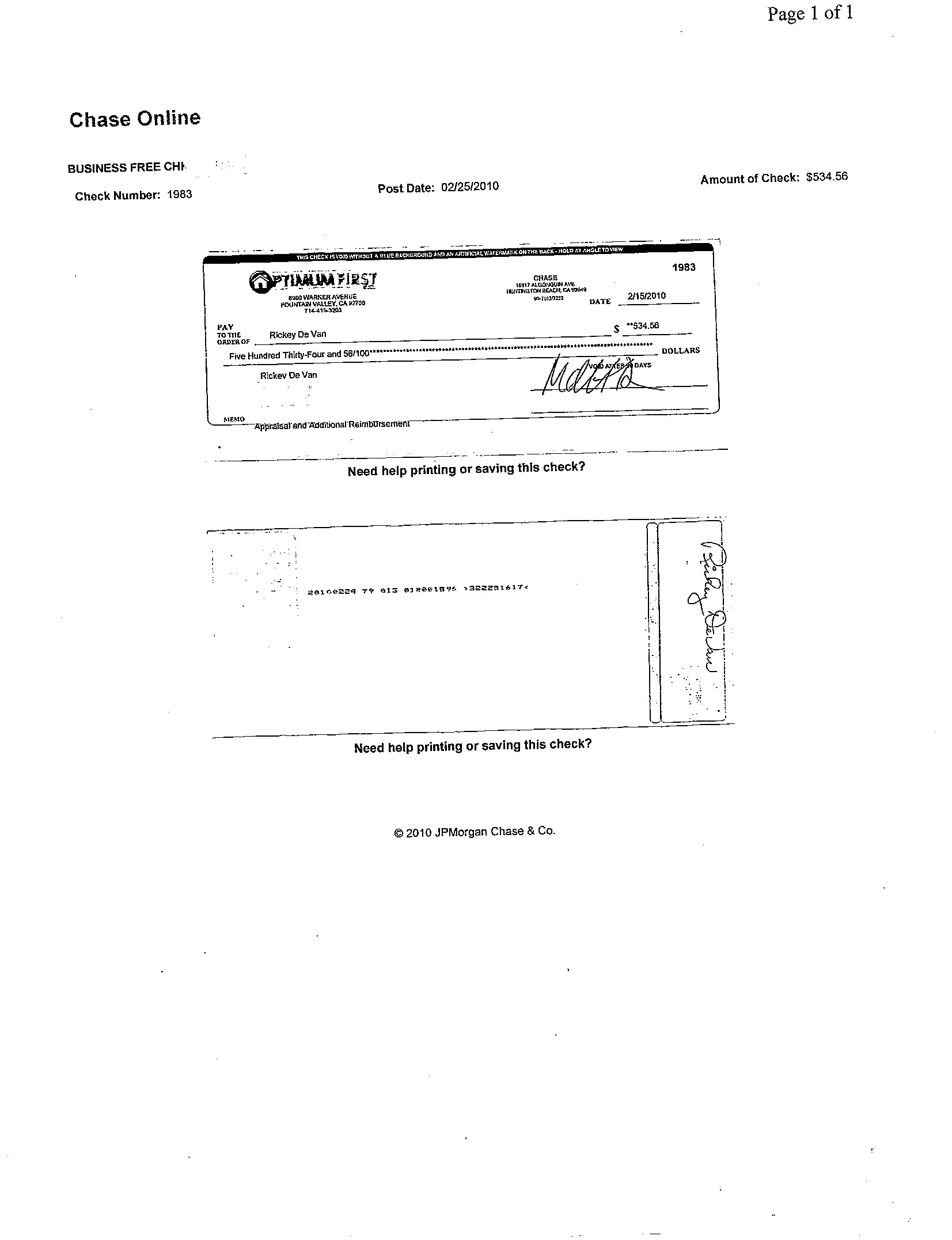

I had two loan applications with Optimum First; on the other loan the appraisal fee was estimated at $434 and I was charged %536--a 23% difference. And then, about two weeks later, Lendervend (the appraiser) charged an ADDITIONAL $110 to my credit card WITHOUT my knowledge or authorization. This was for a "rent analysis," which I was NOT informed of up front. Now the total overcharge was over 65%. Optimum First also failed to disclose early in the process, several requirements of the lender they were working with (Provident). Like, oh by the way, you need to write us a letter telling us what you are going to do with the cash out. No problem. After I wrote the letter the loan officer called back and said I need to get estimates for the upgrades/repairs that I said I was going to use the money for. Why wasn't I told that UP FRONT? Why didn't they know it was coming? I wanted to cancel this load, too, but was "made aware" of the cancellation fee.

Although I asked about paying the mortgage payments online, I wasn't told that Provident charges a $15/transaction fee to pay online if you don't sign up for automatic bill pay. (Wells Fargo doesn't charge this fee.) Paying online manually is preferrable to automatic bill pay because if I have a little left over each month I apply it to the principal. That $15/month fee would go a long way toward paying off the principal. (In fact, if applied to the loan it would reduce the loan's term by more than a year--13 months!!)

So, how does this hurt me? I'm out the appraisal fee for the cancelled loan, and the appraisal fee overcharges for the second loan; both of which Optimum said they would refund. (NOTE: Optimum First sent a partial refund, but still owes me $112.) I'm also out the cost of my time and effort getting all the documents required by the lender and the hours spent on the phone. Not to mention stamps and envelops...and checks.

In addition, I didn't get the cash out from the second loan and simply settled for refinancing the balance. I decided it was a violation of my ethics to say I was going to use it for home repairs (as suggested by Robert Drenk of Optimum First) when in fact I was planning to use it for something entirely unrelated.

I would have cancelled out of this loan, too, but was threatened with a stiff fee. In retrospect, with all their mistakes, I should have taken them to court.

In summary, beware of businesses that "bad-mouth" the competition; they probably have something to hide. My experience with Optimum First is the very worst refinance experience of my life. Without the cash out I'm really no better off now than before the refi.

It is the responsibility of management to make sure their employees know how to do their jobs, especially in a business dealing with other peoples' money.

This report was posted on Ripoff Report on 03/04/2010 11:51 AM and is a permanent record located here: https://www.ripoffreport.com/reports/optimum-first/fountain-valley-california-92708/optimum-first-optimum-first-fountain-valley-ca-mishandled-the-processing-of-my-loans-f-578006. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#5 Consumer Comment

CONSUMER EXPERIENCES

AUTHOR: MIKE - (United States)

SUBMITTED: Thursday, July 23, 2020

Matt, As both a retired CA RE & Mortgage Broker, and then a consumer that ended up with your people - along with my previous YEARS of experience as a business consultant - I would give you & Bob the benefit of the doubt about your stated intents; And having read many of the comments from dissatisfied consumers - which is the benchmark of why companies do not always work efficiently & effectively - and why I never wanted anyone to work under my license, no matter who was doing the asking!

However, these issues usually come because personnel that are not monitored regularly, to wit: I made several calls because the individuals LIED to me about the BASIC realities of what needs to disclosed to borrowers upfront, and I was hoping to get someone who didn't remind me of a 'used car' salesperson! Because I was - due to circumstances beyond my control - on a shortened time-frame of about 38 days, I was hooked up with someone touted as very exeperienced - HAH!!! If I didn't personally have background in the business, I would have lost the house, and possibly my $25,000 deposit!!

I agree with all those who have posted about the general lack of professionalism & honesty in communications in the lending INDUSTRY - it's anti-thetical to why I got into the industry years ago, VERY sad to be a consumer these days, especially with the example in DC!! what really got me P.O.'d was: after the COE is the agent called me - NOT to thank me for getting the loan in spite of his ignorance - but to remind me that HE got PAID, without even offering to forward a fee split of the commission for the hours I spent doing what was supposed to be HIS job!!!!!!!!!!!!!!

#4 Author of original report

Optimum First does not care about contracts

AUTHOR: DesertRat - (USA)

SUBMITTED: Monday, September 19, 2011

So, Matt Dohman chose not to honor the contract he gave me? Sounds like he's setting the stage to get sued for fraud. If he didn't plan on continuing to do business with me then why did he give me a no-cost "Rate Reduction Guarantee?"

#3 REBUTTAL Owner of company

Not Interested

AUTHOR: Robert Drenk - (United States of America)

SUBMITTED: Monday, September 19, 2011

This borrower received an automatic email that was sent out to all of our previous customers, it seems we could never make him happy with all the efforts made so we simply chose not to do business with him. If he was so dissatisfied with our service then why is he still seeking them?

#2 Author of original report

Rebuttal to Optimum First Rebuttal

AUTHOR: DesertRat - (USA)

SUBMITTED: Monday, June 20, 2011

Received the following email from Matthew Dohman last week:

-----------------------------------------

From: "matt@optimumfirst.com "

I am sending an email to all my past clients to see if you would be interested in taking advantage of that free Rate Protection Guarantee you received last time we completed your refinance. Let me know if you are interested in a no cost rate roll down and I will check the rates to see if it is possible.

Hope all is well.

Thanks,

Matthew Dohman

Optimum First Mortgage

Phone: 877-816-7846 x127

Fax: 800-948-0245

www.optimumfirst.com

------------------------------------------

LOL!! (Sarcasm)

The above is the SECOND email I received from Optimum First regarding their "free" rate reduction guarantee. However, their "follow up" is to say that I don't qualify.

If I don't qualify then why do they keep sending the offer?

Is it because Optimum First is NOT an upfront and honest company? They certainly weren't upfront and honest with my loan application and followup.

Why don't they "honor" the rate reduction certificate they gave me when the loan closed?

Optimum First has no intentions of honoring its "guarantees." It's all "hype" and "lies" to get customers.

Neither Robert Drenk nor Matthew Dohman have the courage to follow through on their written promises.

Perhaps a lawsuit (for failing to follow through on their contract) will spark a little fire under their butts

#1 REBUTTAL Owner of company

Optimum First Mortgage Is An Upfront And Honest Company

AUTHOR: optimum first - (United States of America)

SUBMITTED: Monday, March 15, 2010

Bottom line is one of our newer loan officers did misinform him of how a 5/1 ARM loan adjusted. Upon learning of our new loan officer's mistake management call this customer and canceled the loan per the customer's request. We reimbursed this customer for the entire appraisal fee and made him whole (checks have been cashed by customer). The customer decided to continue the refinance of his rental property in which we completed for him at the exact interest rate and fees agreed upon prior to starting the process.

We truly feel like we have done everything possible to accommodate this customer and this customer feels it best to report very negative and inaccurate things to several different websites in the effort to prevent customers from dealing with us. As a company we complete over 100 refinances per month and we have never had a complaint such as this. In fact we have over 200 positive reviews from customers who have done business with us. We do everything possible to make sure each and every customer is completely satisfied.

This customer posted another review on ripoffreport.com about Wells Fargo. He was displeased with their service and mentions that we were able to get him an interest rate better than Wells Fargo and in half the time.

http://www.ripoffreport.com/real-estate-services/rels-valuation-wells/rels-valuation-wells-fargo-r-c5a4f.htm

If you have any questions or concerns please feel free to contact me, Matthew Dohman, at 714-415-3203 x127 or mdohman@optimumfirst.com.

Customer service and satisfaction is very important to myself and my company. We pride ourselves on always trying to do the right thing and what is best for our customers.

Related Reports

07:42 PM

12:09 AM

03:10 PM

04:52 PM

09:57 PM

04:33 PM

Advertisers above have met our

strict standards for business conduct.