Complaint Review: Wachovia Bank - Cumming Georgia

- Author Confirmed

- Wachovia Bank wachovia.com Cumming, Georgia U.S.A.

- Phone:

- Web:

- Category: Banks

Wachovia Bank Steals from the Little Man Cumming Georgia

*Consumer Comment: Which Banks Do NOT Post High-to-Low

*UPDATE Employee: request for input...

*Consumer Comment: Striderq, I Agree With You

*UPDATE Employee: Response to Edward's question...

*UPDATE Employee: Response to Edward's question...

*UPDATE Employee: Response to Edward's question...

*Consumer Comment: Here's One Example - Stay Tuned For More.

*UPDATE Employee: Gee Edward, maybe you need to read my post again...

*Consumer Comment: Edward - It's Inevitable

*Consumer Comment: Yet Another Bank Error - Surprise, Surprise

*Author of original report: Thanks Edward

*Author of original report: Thanks Edward

*Author of original report: Thanks Edward

*Author of original report: Thanks Edward

*Consumer Comment: lbracy, you need to check your facts before posting...

*UPDATE Employee: Wow, I must have struck a nerve, Come on everybody dogpile on striderq

*Consumer Comment: I Agree - Yeah, yeah.....blah, blah

*Author of original report: Yeah, yeah

*UPDATE Employee: RE: Judy's suggestion

*Consumer Comment: This is a joke, right??

*Consumer Comment: Interesting

*Consumer Comment: NSF's Are Meant to be Punitive

*Consumer Comment: I agree

*Consumer Comment: What lawsuit did BOA settle?

*Author of original report: Baffling?

*Consumer Comment: Baffling..

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

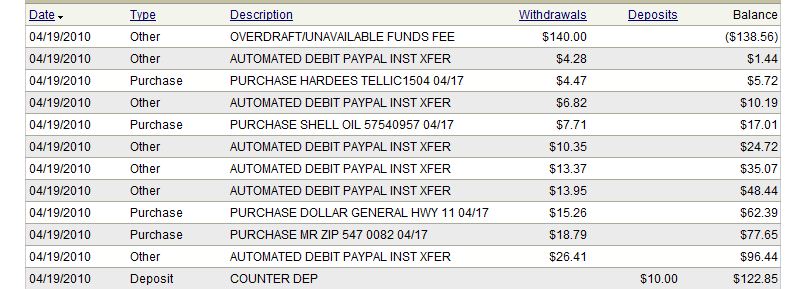

I believe Wachovia uses deceitful, unfair business practices to steal money out of my bank account. And if you call and attempt to talk with someone you will only hear how you overspend and should keep a register.

I do not understand how a bank can put my card transactions on hold, deduct the amounts from the available balance in my checking account so I certainly couldn't spend the money, but then they choose to give the money back, pay a check and charge an overdraft fee of $35 each for all the little $1 debit card transactions.

I'm an adult and I know not to write checks I can't cover. Life brings extenuating circumstances too though. My ex-husband should have made a deposit on Monday, with the holiday on it should have been Tuesday. I had to write a check for my power bill last week and he was late making the deposit. When I checked my account online last night everything was fine. All the card transactions were there and deducted from the available balance in my account. When I pulled up my account this morning Wachovia had paid the check presented on 11/13/2007 THEN ran all the card transactions that were dated between 11/8-11/12 charging a $35 fee for each of them, 14 transactions for a total of $490. My paycheck is direct deposited so they already have my money. I was told if I went and closed the account today they would just reactivate it and put my pay in the account.

Times are tough for me right now like most. I live paycheck to paycheck and now can't pay my rent because they robbed me. When you talk with someone at Walk-Ovah-Ya you can expect a snotty attitude, financial spending lectures and a tight grasps on the money they just stole.

L

Cumming, Georgia

U.S.A.

This report was posted on Ripoff Report on 11/14/2007 12:25 PM and is a permanent record located here: https://www.ripoffreport.com/reports/wachovia-bank/cumming-georgia-30041/wachovia-bank-steals-from-the-little-man-cumming-georgia-284804. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#26 Consumer Comment

Which Banks Do NOT Post High-to-Low

AUTHOR: Ga_consumer - (U.S.A.)

SUBMITTED: Sunday, May 10, 2009

I just found this report after watching a new story on high-to-low bank processing. The report here appears to be dated. Does anyone have a list of banks in Georgia that DO NOT post high-to-low, but instead use chronological posting methods? Thank you.

#25 UPDATE Employee

request for input...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Tuesday, December 04, 2007

Edward, I can accept and appreciate what you're saying. With that in mind, if there's any WAMU customers reading this report: please let us know where your branch is and how they post. Thanks & Merry Christmas to all

#24 Consumer Comment

Striderq, I Agree With You

AUTHOR: Edward - (U.S.A.)

SUBMITTED: Sunday, December 02, 2007

It was ALWAYS my understanding that individual branches all follow the corporate posting policy standard. So when I discovered that Washington Mutual here in Dallas posted chronologically and not in order of Largest amount to Smallest amount, I assumed that WAMU did this Nationwide at all of their branches.

But when I was trying to be discrete and not single out WAMU by name, I posted the FDIC's list of top National banks and stated not all of the banks on this partial list post in order of amount WAMU of course is on the list. Many posters responded with the names they KNEW for a fact who did. And these responders were emphatic that they had PERSONALLY talked to employees or customers of these banks who confirmed this. I don't live in their cities, so I don't have first hand access to other WAMU branches to confirm or deny what the rebuttals said. I simply took the word of these rebuttals because I didn't have any evidence to contradict them? What else was I supposed to conclude?

But based on your response as a bank employee, let me say that I agree with you that I also suspect that all branches use the same corporate posting policy. And if THIS IS TRUE, then this means that Washington Mutual can now be considered a top National bank that DOES NOT post transactions in order of amount, if ALL branches follow the same chronological posting policy that the DALLAS branch does here which I DO KNOW FOR A FACT!

#23 UPDATE Employee

Response to Edward's question...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Saturday, December 01, 2007

Edward,

I can say that the corporate policy of Wachovia is to post largest to smallest. I can also say that I do not believe that the corporate office will allow a branch to post in some fashion other than the corporate method. First of all the corporate computers are the ones that do the posting not each individual branch. There fore I believe than all branches will post per corporate.

If corporate allowed otherwise, they are basically asking people to sue them because "the people at XYZ branch" are being treated differently than others. Now, I also believe than when you speak to an employee at the branch that they may give out false information and state that the posting order is something other than it really is.

But to say that I believe one or more branches posts chronologically, smallest to largest or in some fashion other than corporate standard then I would have to see continued evidence (more than one day posting from more than one account) to accept that a branch is doing things their own way.

#22 UPDATE Employee

Response to Edward's question...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Saturday, December 01, 2007

Edward,

I can say that the corporate policy of Wachovia is to post largest to smallest. I can also say that I do not believe that the corporate office will allow a branch to post in some fashion other than the corporate method. First of all the corporate computers are the ones that do the posting not each individual branch. There fore I believe than all branches will post per corporate.

If corporate allowed otherwise, they are basically asking people to sue them because "the people at XYZ branch" are being treated differently than others. Now, I also believe than when you speak to an employee at the branch that they may give out false information and state that the posting order is something other than it really is.

But to say that I believe one or more branches posts chronologically, smallest to largest or in some fashion other than corporate standard then I would have to see continued evidence (more than one day posting from more than one account) to accept that a branch is doing things their own way.

#21 UPDATE Employee

Response to Edward's question...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Saturday, December 01, 2007

Edward,

I can say that the corporate policy of Wachovia is to post largest to smallest. I can also say that I do not believe that the corporate office will allow a branch to post in some fashion other than the corporate method. First of all the corporate computers are the ones that do the posting not each individual branch. There fore I believe than all branches will post per corporate.

If corporate allowed otherwise, they are basically asking people to sue them because "the people at XYZ branch" are being treated differently than others. Now, I also believe than when you speak to an employee at the branch that they may give out false information and state that the posting order is something other than it really is.

But to say that I believe one or more branches posts chronologically, smallest to largest or in some fashion other than corporate standard then I would have to see continued evidence (more than one day posting from more than one account) to accept that a branch is doing things their own way.

#20 Consumer Comment

Here's One Example - Stay Tuned For More.

AUTHOR: Edward - (U.S.A.)

SUBMITTED: Sunday, November 25, 2007

Striderq, Referring to me you asked 'do you really believe each branch does the posting for the accounts delegated to it instead of the corporation doing the posting the same for all accounts in that bank?'. I agree with you about how this is confusing or impossible. I too was under the same impression that all of the branches of National Banks all followed the same Corporate posting policy of that bank.

But I'll explain how I reached my NEW CONCLUSION. When I first made the statement that not all top tier national banks post items from high to low I used the following list as a reference.

Top National Banks (Directly from fdic.gov as of June 30, 2007)

1. Bank of America

2. JPMorgan Chase

3. Wachovia

4. Wells Fargo

5. Citibank

6. Washington Mutual

7. SunTrust

8. U.S. Bank

9. Regions Bank

10. BB&T

11. National City

12. HSBC

16. Keybank

23. Fifth Third

32. Chase

44. Capital One

Then I made the statement that some of the banks you see on this list DO NOT post item in order of largest to smallest. Several people responded with the names of banks on this list that they know WHO DO post using this method. One of those banks mentioned was Washington Mutual. And there are some OP's here on the ROR against Washington Mutual regarding this specific issue. This created my dilemma. Because I know FOR A FACT that at least one Washington Mutual branch here in Dallas, posts items in chronological order.

So it's very simple. I assumed that since Washington Mutual here in Dallas posts items chronologically, they must do this at all of their branches. Once I received information to the contrary, I assumed that apparently the branches must each be autonomous and use their own policies. So I carried it one step further and said, if Washington Mutual branches do things differently, then whose to say that Bank of America, Wachovia and others aren't the same way?

So there's your answer. Now, I ask you as an employee of Wachovia, are you willing to go on record and confirm that ALL Wachovia branches adhere to the same policy and THEY ALL post items from high to low? Because Washington Mutual apparently is not this way. And there may be others......stay tuned. I'm not withholding information, I just have yet to confirm or deny who does what for certain.

#19 UPDATE Employee

Gee Edward, maybe you need to read my post again...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Sunday, November 25, 2007

Wow, I must be a terrible person. I wait in hiding to "pounce" on people and attack them. Edward if you were to reread my post, especially the title, you will find that the post was in response to a suggestion by Judy, not an all out attack on the OP.

But in one of your posts you state that Lbracy did not overspend her account. Unfortunately that is exactly what happened. I understand she expected ex-husband to make a deposit, but she chose to spend that money before it was there. Therefore, yes once again, the response is keep your register and don't overspend.

And I see that you're still claiming to "know" not all banks post largest to smallest, but then admitting you're not sure which ones. As for checking the individual branches, do you really believe each branch does the posting for the accounts delegated to it instead of the corporation doing the posting the same for all accounts in that bank? There MAY be some banks that post smallest to largest or in chronological order for items posting that day, if I find any I'd be glad to put their names on a post. It's not endorsement it's just informing and validating my statements.

#18 Consumer Comment

Edward - It's Inevitable

AUTHOR: Jim - (U.S.A.)

SUBMITTED: Saturday, November 24, 2007

Edward, you talk about how the major banks within a city in Texas doesn't post high to low. However, it is inevitable these banks will change their tune as well to be consistent with all other banks; to recommend people search for the virtually impossible in places other than Texas would seem a waste when we all know using a Credit Union in any state would deliver better service and lower fees. On top of this, the OP can avoid the bank switching policies year(s) down the line and have this happen all over again.

Now that I've said that again, I will also say again that the OP is blaming the bank for something that is not the bank's fault. If her ex-husband doesn't pay her timely, her problems cascade downward to all the bills she owes, and the NSF fees she incurs. I'm all for nailing a bank for errors they commit (like the one they committed); the customer had the proof of error and the bank reversed the charges. That's good for both the bank and the customer. The rest of the fees are hers to own all by herself - and hers by her own admission. We should consider whether any of this would have happened if the payment was received timely - the likelihood is that virtually none of the NSF's would have happened......

#17 Consumer Comment

Yet Another Bank Error - Surprise, Surprise

AUTHOR: Edward - (U.S.A.)

SUBMITTED: Saturday, November 24, 2007

Lbracy, I'm VERY GLAD to hear you were reimbursed SOME of your fees, given the fact that it was partially caused by a BANK ERROR. This is all you can hope for. The bank will always fight tooth and nail to give back ANYTHING, even when THEY are at fault. Their scapegoat here is the deposit.

To Striderq, You have already found the OTHER THREAD I was referring to and you have now offered a suggestion to that AUTHOR. It's just sad that it took you THIRTEEN DAYS to respond to that OTHER THREAD where the problem was caused by.....you guessed it.....yet ANOTHER BANK ERROR. But yet on this thread, you responded in just THREE DAYS. What's the difference? On this thread Lbracy stipulated that she made mistakes based on an innocent assumption about a deposit. So you Striderq saw the opening and you pounced on the opportunity.

Regarding certain bank practices and policies, yes you can always count on me popping up and stating 'I know all banks don't do it this way but I can't tell you who'. You know why Striderq? Because I attempt to keep my posts factual as well, like you. To clarify for everyone else's benefit, more than once I've made the statement that not ALL branches of top tier National Banks use the Largest-To-Smallest posting order that most customers detest. To answer Striderq's accusation, I can't tell you who these banks or branches are because each one is unique.

After making this statement, I gave EVERYONE the PERFECT WAY to CONFIRM or DENY this. Simply call the Dallas branches for the well known National Banks and ask them YOURSELVES. To this day, still NOT A PEEP out of ANYONE, not even Truth Detector who more than once called me a LIAR and FRAUD regarding this issue. And you Striderq are a BANK EMPLOYEE so you CERTAINLY should be in the know about this! So PLEASE everyone, put up or shut up!

Finally, you said 'I've attempted to keep my postings factual and not attack anyone'. It was not my intent to attack you either, personally. But I felt I had to use accusations that were stinging enough to cause you to respond, especially on the OTHER THREAD and you have done so and hopefully your suggestions will benefit that complainant. And Lbracy has received some of her fee refunds here as well, so EVERYONE'S happy, right? See how easy that was?

#16 Author of original report

Thanks Edward

AUTHOR: Lbracy - (U.S.A.)

SUBMITTED: Friday, November 23, 2007

I truly appreciate your constructive criticism. We did discover an error made by the bank in that they paid a bill prior to the actual date I had it scheduled for. I was reimbursed for some of the fees, the others I had to as you say bite the bullet. I fully understand now how they work and I suppose it was my fault for not studying all the fine print they constantly send out. Logically thinking when the transactions were posted and the money had been deducted it seemed to me as though they gave the impression that stuff had been paid. For them to decide outside of that how they will spend my money by arranging transactions as they see fit, as opposed to how they come in, seemed illogical. I've got it now.

The others that chose to just flame made me find this experience rather sour. It just seems if you have something constructive to say it could be said in a constructive manner. Most just obviously need somewhere to vent. Find something better to do with that energy in a more positive way.

Oh, and I did research before I posted.

#15 Author of original report

Thanks Edward

AUTHOR: Lbracy - (U.S.A.)

SUBMITTED: Friday, November 23, 2007

I truly appreciate your constructive criticism. We did discover an error made by the bank in that they paid a bill prior to the actual date I had it scheduled for. I was reimbursed for some of the fees, the others I had to as you say bite the bullet. I fully understand now how they work and I suppose it was my fault for not studying all the fine print they constantly send out. Logically thinking when the transactions were posted and the money had been deducted it seemed to me as though they gave the impression that stuff had been paid. For them to decide outside of that how they will spend my money by arranging transactions as they see fit, as opposed to how they come in, seemed illogical. I've got it now.

The others that chose to just flame made me find this experience rather sour. It just seems if you have something constructive to say it could be said in a constructive manner. Most just obviously need somewhere to vent. Find something better to do with that energy in a more positive way.

Oh, and I did research before I posted.

#14 Author of original report

Thanks Edward

AUTHOR: Lbracy - (U.S.A.)

SUBMITTED: Friday, November 23, 2007

I truly appreciate your constructive criticism. We did discover an error made by the bank in that they paid a bill prior to the actual date I had it scheduled for. I was reimbursed for some of the fees, the others I had to as you say bite the bullet. I fully understand now how they work and I suppose it was my fault for not studying all the fine print they constantly send out. Logically thinking when the transactions were posted and the money had been deducted it seemed to me as though they gave the impression that stuff had been paid. For them to decide outside of that how they will spend my money by arranging transactions as they see fit, as opposed to how they come in, seemed illogical. I've got it now.

The others that chose to just flame made me find this experience rather sour. It just seems if you have something constructive to say it could be said in a constructive manner. Most just obviously need somewhere to vent. Find something better to do with that energy in a more positive way.

Oh, and I did research before I posted.

#13 Author of original report

Thanks Edward

AUTHOR: Lbracy - (U.S.A.)

SUBMITTED: Friday, November 23, 2007

I truly appreciate your constructive criticism. We did discover an error made by the bank in that they paid a bill prior to the actual date I had it scheduled for. I was reimbursed for some of the fees, the others I had to as you say bite the bullet. I fully understand now how they work and I suppose it was my fault for not studying all the fine print they constantly send out. Logically thinking when the transactions were posted and the money had been deducted it seemed to me as though they gave the impression that stuff had been paid. For them to decide outside of that how they will spend my money by arranging transactions as they see fit, as opposed to how they come in, seemed illogical. I've got it now.

The others that chose to just flame made me find this experience rather sour. It just seems if you have something constructive to say it could be said in a constructive manner. Most just obviously need somewhere to vent. Find something better to do with that energy in a more positive way.

Oh, and I did research before I posted.

#12 Consumer Comment

lbracy, you need to check your facts before posting...

AUTHOR: Truth Detector - (U.S.A.)

SUBMITTED: Friday, November 23, 2007

'the BOA settlement for transaction processing practices I believe was in 2005 or 2006.'

There has been no lawsuit ever won or settled for the actual assessment of overdraft fees or the ordering process. The only lawsuit EVER settled regarding overdraft fees was settled by Nationsbank (for failing to properly DISCLOSE the process, not for the actual overdraft policy - which the plantiffs' own lawyer said was perfectly legal), which was subsequently bought out by Bank of America. There is substantial case law and regulatory provisions that support banks' ability to order transactions. If you do not agree with the provisions, then elect different politicians who can appoint different judges. Of course, since the Bush-appointed federal judges are in for life, you may be wishing on a star.

Then again, it is so much easier to blame a deep-pockets, big-name bank in an effort to rally support to your cause. The only trouble with that is there are many educated people watching you and your facts. Therefore, it would behoove you to make sure you have your facts straight.

Now, regarding the REAL issues here related to the OP:

'I do not understand how a bank can put my card transactions on hold, deduct the amounts from the available balance in my checking account so I certainly couldn't spend the money, but then they choose to give the money back, pay a check and charge an overdraft fee of $35 each for all the little $1 debit card transactions.'

*We have advised customers many times to STOP swiping debit cards when they make point-of-sale transactions. Businesses batch these types of transactions - and banks hold the funds until the transactions are processed. Swiping your card and ENTERING A PIN will result in a real-time transaction and immediate posting.

Another thing...you would do well to stop with the little $1.00 debit card transactions. The more you use the card, the more transactions you have to keep track of. Try cash for a change, regardless of what those commercials from Visa or MasterCard try to tell you.

'My ex-husband should have made a deposit on Monday, with the holiday on it should have been Tuesday. I had to write a check for my power bill last week and he was late making the deposit.'

*With all due respect, this is an issue you should be going after your ex-husband for, not blasting a bank for. You wrote a check you did not have the funds to cover. Would you rather Wachovia have paid all the little debit card transactions - then bounced your check to the electric company? I don't know about that company, but when the telecom I work for receives a bounced check, the service is immediately shut off and the customer is placed on cash-only status. Would you rather have had your power shut off?

Your ex-husband's lack of responsibility is what caused this nightmare, not Wachovia. This is a country full of choices. Your pal Edward speaks constantly about how there are banks and credit unions out there who will conduct business in a different manner than most of the large banks. Instead of crying like a little girl about how big, bad Wachovia has 'ripped you off', why not take your ex-husband to court to recover the losses you incurred as a result of his negligent act?

Then, go find a bank or credit union that better works for you and stop playing the victim. No ripoff here with regards to the bank. The ex-husband? He MUST be a ripoff of some sort, or he wouldn't be an 'ex'.

#11 UPDATE Employee

Wow, I must have struck a nerve, Come on everybody dogpile on striderq

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Wednesday, November 21, 2007

I didn't mean to upset anyone but I'll be glad to try to explain the process.

When you use your debit card to make a purchase and the mechant runs your card, that creates a checkcard hold for the amount. We subtract that from your posted balance to give you your available balance. This is the amount you have left to spend on things that are not posted to your account or on hold WITHOUT getting charged a fee. The hold is usually for the day you do the transaction and through posting two business days later. If the merchant has not sent the documentation needed to get the money, then the hold expires and that amount goes back into your available balance. However the merchant can still request and receive the payment. If this money is spent before the merchant requests it, when the item posts it will cause overdraft fees.

When an item is on hold is has NOT been paid. We are just reminding you of the purchase you made with this merchant. Once the card has been approved we can not refuse payment when the merchant asks for it. So if you pay $150 say to your insurance and then withdraw all the money out of your account, when the insurance company asks for the money it will post and cause fees. When we do the posting, yes we do post debits from largest to smallest. But if a register is kept of all transactions, then there would not be any fees because the customer has not overspent their account.

I understand that your problem came about because you believed the deposit had been made when it had not been. I'm sorry to hear this, but it does come down to your responsibility to make sure the money is there before you spend it.

Now I guess this brings me to Edward. I find it very ironic that you use such phrases as "right on cue" and "high horse" when referring to someone elses post. The readers of ROR can always count on you popping up with your line of "I know all banks don't do it this way but I can't tell you who". As far as answering all the postings regarding Wachovia, wow I'm sorry I didn't know that I was under any obligation to answer everything. Just as I notice you don't post to everything. But I'll make you a deal. If there is a particular posting on Wachovia that you want me to respond to, let me know which one and I'll be glad to post.

I've attempted to keep my postings factual and not attack anyone. I do understand living paycheck to paycheck, but that situation makes it more important to understand how the bank processes the transactions so that you do not get any OD fees. I understand the customers work hard for their money, I've just been trying to help them understand how to keep more of it for their use.

#10 Consumer Comment

I Agree - Yeah, yeah.....blah, blah

AUTHOR: Edward - (U.S.A.)

SUBMITTED: Monday, November 19, 2007

Lbracy, in your OP you said - 'And if you call and attempt to talk with someone you will only hear how you overspend and should keep a register'. Then right on cue, Striderq adds his contribution almost exactly on script - 'It basically comes down to personal responsibilty. Keep your register and only spend what money you have in your account after it is in your account'. Boy Lbracy, you must be psychic!

You see L, bank employees like Striderq look for OP's like yours where it's EASY to find blame, and from THEN ON, that's ALL they want to EMPHASIZE. Don't get me wrong, the advice they give is good, don't overspend your account, but everyone can see that's not what you did here. The problem occurred with the deposit that wasn't made. This wasn't the banks fault, that's true but you have a legitimate gripe, does the punishment fit the crime?

Striderq probably gets a kick out of sitting on his high horse and throwing out this advice, meant to always leave the bank blameless. However, I find it funny that on OTHER RECENT THREADS against THIS SAME BANK, Striderq is noticeably ABSENT when the facts obviously confirm the problem was caused by a BANK ERROR and the bank tries to cover up or make excuses for the error. Hmmm...

You see L, YOU are supposed to be a perfect mathematician and take responsibility, when YOU make a mistake, albeit and innocent one, but THE BANK doesn't have to. No other advice than to bite the bullet, take your loss and tell Striderq and this bank what they can do with their SELECTIVE advice! Good Luck!

#9 Author of original report

Yeah, yeah

AUTHOR: Lbracy - (U.S.A.)

SUBMITTED: Monday, November 19, 2007

Let's see...the settlement for BOA disclosing customer's confidential info was this year...the illegal trading practices in the mutual fund industry settlement was in 2004...the BOA settlement for transaction processing practices I believe was in 2005 or 2006.

Eh, I suppose it's easy for you to sit back and judge saying I spend money I don't have. You probably don't have to worry about such a thing. I understand your point but still think it's deceitful to show transactions in my account as being paid and the only outstanding transaction that could be returned was the check, then the bank spends my money how they see fit and rearranges payments to accomodate their pockets.

#8 UPDATE Employee

RE: Judy's suggestion

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Saturday, November 17, 2007

Judy,

The best thing, as most of these posts show, is to not overspend your account. I know that it is hard living from paycheck to paycheck as I do it also. However, as for your suggestion that some poeple receive a monthly fee for overdrafts as opposed to receiving one per item overdraft...that's rather ridiculous.

Everyone would try to claim membership in the monthly fee club. And then most would feel free to spend way more than they have in their account. And some of those would decide that once they have made their purchases and the fee comes in that they could just walk away with all of the items they had purchased. let's see if wachovia did that for some,most,all of their customers they would soon close their doors. While some here would say that is a good thing.

The reality is, when you open your account you receive a Schedule of fees & services that spells out things like posting order, OD fees, etc. I would suggest that everyone read this before they open an account at a particular bank. most of them are going to be the same but there will be some differences. if you don't think you can live with the rules of that bank, find one that you can accept. A lot of people here have suggested credit unions. I have belonged to them before. They will give more personal service, fewer and lower fees but may not have all of the services or branches/locations available with a major bank.

It basically comes down to personal responsibilty. Keep your register and only spend what money you have in your account after it is in your account.

#7 Consumer Comment

This is a joke, right??

AUTHOR: Peter - (U.S.A.)

SUBMITTED: Thursday, November 15, 2007

Obviously you are being charged NSF's because you are charging a greater amount than that which you have in your account -- regardless of what has already posted and what is pending. To put it simply, you are spending money that you do not have. Therefore, you must pay a fee the same as everyone else who engages in such behavior.

If you do not have enough funds to cover all your "$1 debit card transactions" then perhaps you should refrain from using your debit card until you have at least a few dollars in your account.

#6 Consumer Comment

Interesting

AUTHOR: Cory - (U.S.A.)

SUBMITTED: Thursday, November 15, 2007

Was reading an article this morning in CR that stated, in one study, that found that people who use their DEBIT card more then 20 times a year AND overdraft their accounts, pay OVER $200+ in fees each year. $200+ frickkin' dollars in fees. Yep, things are getting better. The banks are telling us how much better it is FOR US to use debit cards. Here's a women who has $490 in OVERDRAFT FEES ON 14 TRANSACTIONS. The truly sad part is she is using her debit card on "ALL THE LITTLE ONE DOLLAR debit card transactions". A banker's dream. She goes on to state she is living paycheck to paycheck. She states "I know not to write checks I can't cover". Too bad the same thing can't be said about debit card transactions, which are just about the same thing. Instead of a few debit card transaction for a larger amount, she has dozens of "little $1 transactions", each one racking up a $35 overdraft fee for each. PATHETIC.

#5 Consumer Comment

NSF's Are Meant to be Punitive

AUTHOR: Jim - (U.S.A.)

SUBMITTED: Thursday, November 15, 2007

Judy, to some extent I agree with you. However, let's understand NSF's are clearly made to be punitive in nature; no one should be overdrawing their account as the NSF paid by the bank amounts to an unsecured loan the bank may never recover from a customer. Banks will not allow themselves to be open to that sort of liability - regardless of the situation - and the NSF is both additional revenue to the bank and a heck of a penalty for the person who overdrew the account.

As you said, living hand to mouth is how many people live their lives, but it is not an excuse to overdraw an account. I don't say this because I have an abundance of wealth - I say it because people who live hand to mouth will never extract themselves from that situation if they incur avoidable expenses all of the time. I can't tell you how many people have written ROR's here and claim they pay hundreds of dollars per month in NSF fees - and many will even say, " I knew I was going to overdraw the account, " and then claim the bank is taking food out of the mouth of their children. These are people who wish they were rich but clearly do not understand how to get there. They will always be the "little man" as the OP put it in the title.

In this case, she blames the bank. She needs to blame the ex-husband for being late with the payment and his late payment cascaded downward.....

#4 Consumer Comment

I agree

AUTHOR: Judyndskies - (U.S.A.)

SUBMITTED: Thursday, November 15, 2007

I agree with you on robbing the small man. It is no more than right to be punished for intentionally overdrawing day after day, but for us little people that live from week to week, why can't we be charged a monthly fee instead of being charged $35.00 for overdrawing 1 cents. It just doesn't make sense, and I say everyone try and find a Credit Union to join. I don't think the penalities are as harsh and won't send you into bankruptcy.

#3 Consumer Comment

What lawsuit did BOA settle?

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Thursday, November 15, 2007

I hope you're not gonna say the one from a few years ago. That wasn't BOA (it was a bank BOA purchased) and it was about DISCLOSING overdraft fees - not the actual fees.

#2 Author of original report

Baffling?

AUTHOR: Lbracy - (U.S.A.)

SUBMITTED: Wednesday, November 14, 2007

I didn't think I had any extra money. Where did I say that? What I'm saying is that the transactions for debit charges between 11/8 - 11/12 were deducted from my account. Those funds were certainly not available for me to spend and my available balance reflected that. On the 13th the bank put the money back in, paid a check, and NSF'd all the debit transactions. I'll be the first one to admit the money wasn't there to cover that check because the deposit was made late. So charge me for ONE $35 NSF fee. Don't show in my account that all my transactions are covered then decide oh no, we lied, instead we chose to pay something that was presented AFTER all the other transactions so we can rip you off for $490.

Baffled? Do some research on the class action lawsuit that Bank of America just settled.

#1 Consumer Comment

Baffling..

AUTHOR: John - (U.S.A.)

SUBMITTED: Wednesday, November 14, 2007

"I do not understand how a bank can put my card transactions on hold, deduct the amounts from the available balance in my checking account so I certainly couldn't spend the money, but then they choose to give the money back"

So how did you account for sudden "extra" money beng in your account?

By your own admission, you had to have seen the card transactions "on hold" and knew that you were at least that much less in your account.

You certainly must have gone back and looked as you state that they "choose to give the money back".

Did you think they were giving you a gift?

Did you think the merchants were suddenly giving you a gift?

You still had to know that the money was not there to spend as you admit to seeing that they "gave the money back" as you put it. So, you went and wrote checks anyway by your own admission.

"I'm an adult and I know not to write checks I can't cover."

Well, anybody can pretty much write a check - you just have to write one that would actually be covered by the funds in the account.

The rest of the non-ripoff is just BS bailout excuses. You willingly admit that you had to write checks on money you clearly didn't have posted to the account.

Related Reports

09:05 PM

12:21 PM

06:09 AM

10:45 PM

02:47 PM

05:46 AM

12:44 AM

09:58 AM

04:31 PM

12:06 PM

09:44 PM

04:08 PM

02:53 PM

04:58 PM

09:42 PM

11:13 AM

03:34 PM

01:09 PM

07:14 AM

10:31 AM

04:01 PM

01:21 PM

08:30 AM

10:13 AM

04:34 PM

Advertisers above have met our

strict standards for business conduct.