Complaint Review: WoodForest National Bank - Amarillo Texas

- Author Not Confirmed

- WoodForest National Bank Wal-Mart in Amarillo, TX Coulter St. Amarillo, Texas United States of America

- Phone:

- Web:

- Category: Banks

WoodForest National Bank This is the Worst Bank Ever! Amarillo, Texas

*Consumer Comment: I Couldnt Agree More!!!!

*Consumer Comment: "Truth" detector? Here is some Truth...

*Consumer Comment: Wow Indeed!

*Consumer Comment: Oh, this is PRICELESS from Ronny G...

*Consumer Comment: That's because Robert and Truthdetector are clutching at straws...

*Consumer Comment: RE: WOW

*Author of original report: WOW~!

*Author of original report: WOW~!

*Consumer Comment: TD...

*Consumer Comment: Robert, I say we let them 'opt out' of check overdrafting as well...

*Consumer Comment: Robert, I say we let them 'opt out' of check overdrafting as well...

*Consumer Comment: The grass is always greener..NOT..

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

This bank is the worst ever! I have only had the account for a few months and so far have had nothing but problems with it

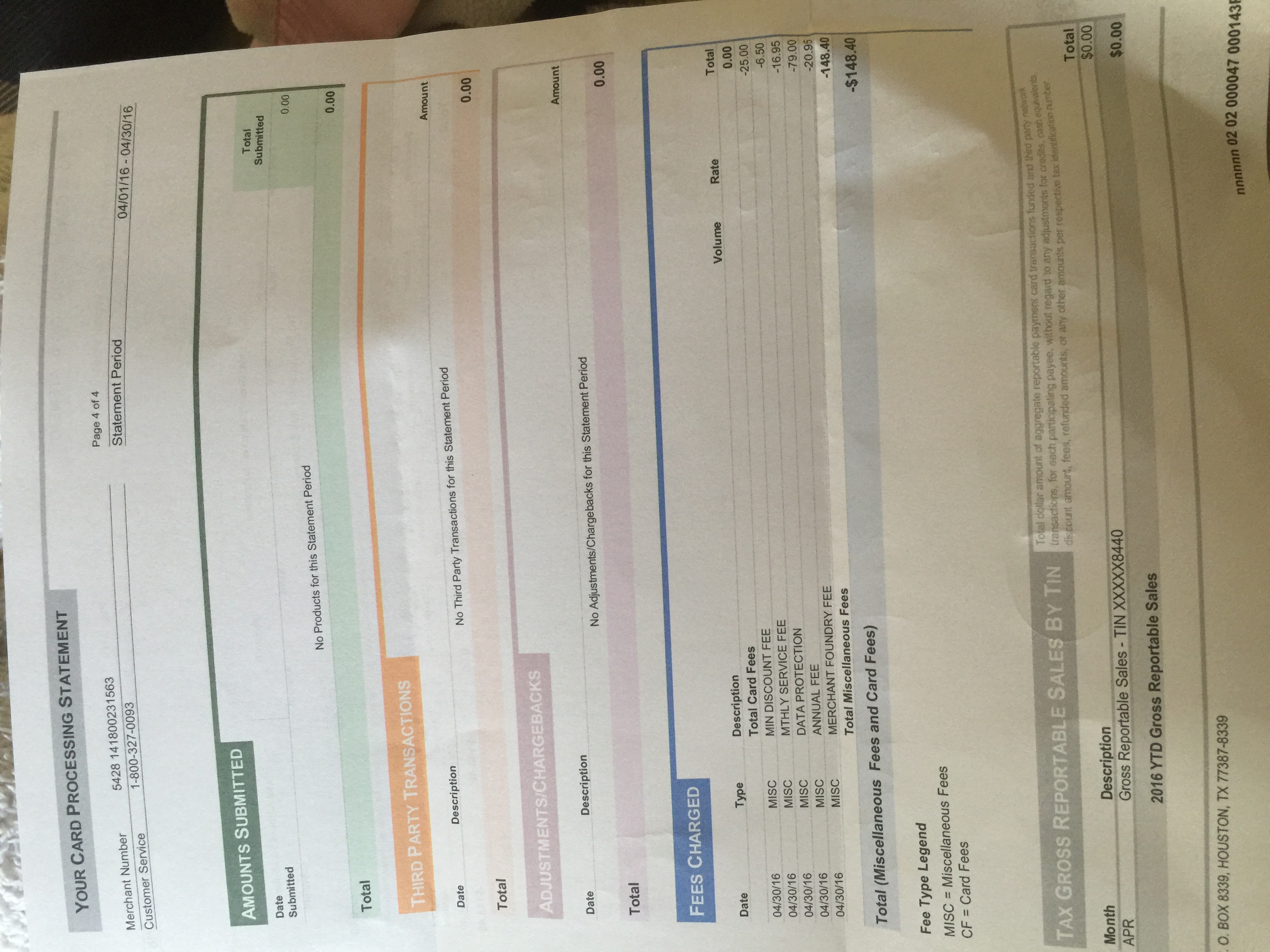

Issue no.1 - Pending charges - No matter what you do write a check, use ATM, or get cash from the Teller , they put those transactions as pending for 5-7 days which puts you in a bind when you have no idea when that money is comming out even after I recieved reciepts from the people I was paying saying they have thier money It still says pending..at other banks when you use their services it comes out that day! When you ask them about it they ALWAYS blame the merchant for not taking the money out even tho you have a reciept from the merchant and talked to them and they tell you they got their money. Why would they lie to you and after you provide the proof they say they can't help you they don't understand they are told to tell the customer that it is the Merchants fault and let it go?

Issue No.2 - NSF fees -They charge you 34.00 per transaction that gets taken out even tho you have the money in pending status. Why can't that money be taken out?if its in pending status that money should not be available for use for other transactions. If I pay someone that money should be theirs not the banks ...so lets say I have 100 dollars in the bank and I pay a bill for 100.00 and it goes into pending and I deposit 100.00 the next day then I take out 50 dollars they bank (woodforest only) takes the 50 out of my pending money first! which is crap! No other bank I have ever Had does this!!!

Issue NO.3 - OD fee - If you make a mistake and you go into the Neg and your there for more than 7 days they charge you 5 dollars a day fee.If you deposit money before the 7 th day and then use that money...even tho you were a positive in your account (on record ie- bank statment) they still charge you 5 dollars a day stating that you have to be a positive in your account for a full 24 hours even tho in the paperwork they give you when you open the account does not state this at all!

Summery- I know banks are a business and are out to make money, they should not be ripping off their customers. This bank is one of the biggest legal scams in our country and the only reason they have remained a bank is because of their (we don't do credit checks to get you an account) people with bad credit history have no choice today but to get an account with them. If they were a regular Bank they would not have lasted 1 month competing with a REAL bank. My suggestion is this use a Debit/credit card and have your Direct Deposit going to the card DO NOT USE WF BANK! The card charges you a monthly fee but it is alot cheaper than getting ripped off by a BANK!

Customer Service - Well ive had 2 sided issues here.. one Branch was very helpfull and kind and another was very rude and demeaning twords me as well as the manager (she rolled her eyes at me when I showed her the bank statment) If I am off base and wrong about any of this then tell me why is woodforest bank complaints running rampant all over the internet and this website? Why so many complaints? have you looked at other banks complaint list? like CHase or Wells Fargo? Hmmm something to think about.

This report was posted on Ripoff Report on 10/26/2009 12:10 PM and is a permanent record located here: https://www.ripoffreport.com/reports/woodforest-national-bank/amarillo-texas-79109/woodforest-national-bank-this-is-the-worst-bank-ever-amarillo-texas-515016. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#12 Consumer Comment

I Couldnt Agree More!!!!

AUTHOR: Nissa - (United States of America)

SUBMITTED: Tuesday, July 20, 2010

I am an account holder also and I get ripped off all the time. I have direct deposit for my payroll and if I have a check come thru the same night as my paycheck, they will act as if the money is not there, claiming that it is still pending. Yet, I can go to an ATM and access that money. They claim it is a courtesy for the customer to get to their money when it is still pending.

If this is the case then where is this so called courtesy when a check is coming thru at the same time? THE MONEY IS THERE! THEY CAN SEE IT! But yet you are charged anyway?

Furthurmore, for you indignant small minded people that dont have to live paycheck to paycheck, there are those of us that have no choice but to rely on things going thru the bank to survive. I dont think thats an open invitation to be robbed. If the money truly isnt there, then by all means, charge me. But when you can actually SEE it and I can actually ACCESS it, then ITS THERE, MCFLY!!!!

I also have a strong suspicion that the rebuttals against the author of this complaint, were written by bankers (woodforest) to explain away how they take advantage of people. Do you have a department dedicated just to responding to your ripoffs? If not, it might be something to think about.... I have a feeling you havent heard the last of the complaints........

#11 Consumer Comment

"Truth" detector? Here is some Truth...

AUTHOR: Ronny g - (USA)

SUBMITTED: Thursday, October 29, 2009

Truthdetector "quipped":

"Ronny G quipped:

"Of course they have to make up pretend situations, like with the checks..they can't make a valid point any other way."

Is that a joke? You and your "partner" Edward have made a career out of inserting nonsense hypotheticals from the moment you both began posting here. Now, I introduce a REAL example BASED ON WHAT I HAVE SEEN WITH MY OWN EYES AND HEARD WITH MY OWN EARS, and you coin that as "pretend"?"

That is because the "hypothetical" situations you BOTH used I this case..does not apply. The OP himself had to come back and clear that up. You bank defenders only can use check 'hypotheticals" to rebut..and most of these reports had either nothing to do with checks...or it would not have mattered.

"And oh by the way, the OP stated:

"No matter what you do write a check, use ATM, or get cash from the Teller , they put those transactions as pending for 5-7 days which puts you in a bind when you have no idea when that money is comming out..."

Yes..the poster did state this...and this is an example of a "hypothetical" that has merit in this report..thank you for pointing that out.

"Sure seems like his problem with "checks" isn't quite to "pretend", does it?"

It is not pretend, I would not give it that much credence...it is irrelevant..like most of what the bank defenders have left to "clutch" at.

"Seriously, Ronny...PUT DOWN THE PIPE. Your willingness to defend the useless, irresponsible degenerate deadbeats who can't exercise 4th grade math skills and balance a checkbook is amusing, but you have morphed into something little more than a complete joke with your useless, childish rants devoid of any facts and featuring a complete disregard for REALITY."

Uh...I think you need to put something down. As this last statement proves beyond a shadow of a doubt..that the ONLY reason you come here..is to insult ripped off bank customers....you even admit that you find it amusing. Why can't you find a way to amuse yourself that does ANYBODY any good? Is your only pleasure in life the pursuit of making everyone else feel bad? It is supposed to be "the pursuit of happiness"..you have your values completely a*s backwards my friend.

"The TRUTH is that these people who opt out will have NOT changed their bankingfinances as only a deadbeat can. habits. They WILL write bad checks and authorize BAD ACH transactions. In the case of a check, they will face SEVERE civil and/or LEGAL problems (including criminal charges in some instances) if they continue their deadbeat ways and mismanage their "

If someone opts out of overdraft protection..or not..and they criminally bounce checks...that is a crime. Now enough with the checks...this issue is regarding banks tactics.

If a customer is opted out of overdraft protection...transactions at a point of sale..or an ATM will be declined if the funds are unavailable. That is all that should be taken from the banks changing of this policy and allowing this option..as well as not "automatically" enrolling EVERY customer in it..whether they want the service or not. Why are you making so much of this...bounce any checks lately?

Here are the additional bank tactics currently being looked into. Feel free not to respond..but just take them as the facts as exposed by the FDIC report. We already know in your eyes all overdrafters are deadbeats..no need to "beat" that dead horse any further. And thank you for insulting a war hero...you certainly deserve the medal of honor for that blunder.

Overdraft fees have APRs ranging from 1,067% to 3,520%.

Explains why the bank likes them..encourages them..and will continue to if allowed. Some bank defenders claim that overdrafters are some kind of burden on the bank..the report seems to prove otherwise...since if these customers were so bad for the bank..why does the bank not close the account? And why does the bank cover the overdrafts to begin with?..well that is obvious. I guess the "risk" is worth the "reward..oh the banks know what they are doing..believe me.

Banks operating automated overdraft programs reported a median transaction of $36.

This tells us the reason the bank uses for re-sequencing (to process large transactions first) is total nonsense and unnecessary... according to the report and many customers.

Young adults paid the most in overdraft fees and were responsible for the most NSF transactions.

Because these are inexperienced bankers...very easy to fall into the trap. If the bank really wanted to prevent these overdrafts from occurring..they EASILY could..but then they would not be able to make all that profit...so why would they want this to stop?

Customers in low-income areas were more likely to pay recurrent overdraft charges.

Another "prime" target. The lower income customers were hit hardest by the recession..perfect time for the banks to strike. After all..the banks policies are set up to most easily overdraft customers who keep a low balance..their many tactics encourage this...and the bank can make the poor suffer more so the executives can buy another jet.

Customers were automatically enrolled in overdraft-protection programs.

Thankfully, most banks have decided on their own to stop this tactic voluntarily..before the pending lawsuits are done..and before the legislators let it rip..smart move by the banks actually..I am sure they did not want to change this policy..as when combined with the re-sequencing...nets them a fortune in profits.

Banks process large debits first; making overdrafts more frequent.

Correct..the FDIC is apparently smart enough to figure this out. As to wit..this HAS to be the ONLY reason the banks would continue to use this tactic these days.

Banks allow ATM and debit card overdrafts, but do not alert customers in advance.

No, they do not alert us. Which they should. Because how do they know the overdraft is not a result of error, fraud or theft? They just assume everyone wants to spend 35 dollars on a cup of coffee or a cheeseburger? Surely the banks are not that stupid..quite the contrary..this is NOT something the bank wants to "alert" anyone about..otherwise they will not be able to charge all the outrageous fees.

#10 Consumer Comment

Wow Indeed!

AUTHOR: Edward - (U.S.A.)

SUBMITTED: Thursday, October 29, 2009

Seems this Original Poster is up to speed already on how rebut the 'bank defenders' with common sense logic.

No assistance from me needed here. But I will only emphasize a few points.

So you use the same merchants probably. But strangely enough the transaction from these merchants post fairly quickly, if not immediately, with the majority of banks you deal with. But somehow, with this bank here, the transactions from these same merchants take anywhere from 5-7 days. Hmmm.

Then after switching banks, and discovering your new bank does things just like your previous banks did, no more problems. Just like no problems with your previous banks, prior to this one here. Hmmm.

Yes indeed. Everyone benefits from your much appreciated service for this country. Even the 'bank defenders'. I can only imagine how you feel, after putting your life in danger for the likes of individuals who do nothing more but spit in your face with off base insults that in no way reflect the true issue. Kinda like rubbing salt in the wound.

Good luck to you with your new bank, but it sounds like you won't need it. Who needs luck when you have common sense logic and math skills on your side already. As proven by the absence of these same issues at your other banks.

#9 Consumer Comment

Oh, this is PRICELESS from Ronny G...

AUTHOR: Truth Detector - (U.S.A.)

SUBMITTED: Thursday, October 29, 2009

Ronny G quipped:

"Of course they have to make up pretend situations, like with the checks..they can't make a valid point any other way."

Is that a joke? You and your "partner" Edward have made a career out of inserting nonsense hypotheticals from the moment you both began posting here. Now, I introduce a REAL example BASED ON WHAT I HAVE SEEN WITH MY OWN EYES AND HEARD WITH MY OWN EARS, and you coin that as "pretend"?

And oh by the way, the OP stated:

"No matter what you do write a check, use ATM, or get cash from the Teller , they put those transactions as pending for 5-7 days which puts you in a bind when you have no idea when that money is comming out..."

Sure seems like his problem with "checks" isn't quite to "pretend", does it?

Seriously, Ronny...PUT DOWN THE PIPE. Your willingness to defend the useless, irresponsible degenerate deadbeats who can't exercise 4th grade math skills and balance a checkbook is amusing, but you have morphed into something little more than a complete joke with your useless, childish rants devoid of any facts and featuring a complete disregard for REALITY.

The TRUTH is that these people who opt out will have NOT changed their banking habits. They WILL write bad checks and authorize BAD ACH transactions. In the case of a check, they will face SEVERE civil and/or LEGAL problems (including criminal charges in some instances) if they continue their deadbeat ways and mismanage their finances as only a deadbeat can.

#8 Consumer Comment

That's because Robert and Truthdetector are clutching at straws...

AUTHOR: Ronny g - (USA)

SUBMITTED: Wednesday, October 28, 2009

I can't apologize for the way they responded..but if you have been to this site before and read similar bank complaints..you would notice these 2 buffoons are 2 of a handful of notorious bank DEFENDERS..who like to belittle anyone who has a problem with the bank..and then place NO blame whatsoever on the bank..regardless of how many of the same complaints come in, and regardless of the evidence.

Of course they have to make up pretend situations, like with the checks..they can't make a valid point any other way.

What they are probably trying to imply...with MUCH FAILURE..that if you had been opted out of a part of the banks tactics that contributed to those fees and problems....known as mandatory automatic forced "courtesy" overdraft protection service..that it would have either made no difference..or would have incurred an NSF fee if you bounced a check...like that is some kind of new invention?? An NSF fee for a bounced check, imagine that???..tell us something we don't know.

Bottom line is this. If you WERE to have been opted out of overdraft protection..none of this would have or COULD have happened...since even though the banks DECEPTIONS notified you that funds were available...obviously they were not. If you are opted out of overdraft protection (which the banks normally do not like to allow) ANY transaction made at a point of sale (merchant)..or an ATM swipe...is declined if the funds are actually unavailable..regardless of what the bank says..and regardless of what your register says if you made an error.

Many of us have caught on to the banks tactics..and there have been so many complaints..that congress is putting pressure on the banks..and law suits are pending on some of these banks...so a few of them have decided...OWN THEIR OWN...before any legislation is actually past...to change some of these tactics. Makes you wonder if the banks have figured out that perhaps they were doing something wrong? I mean why else would they change any policies that would cost them to take in less fees if they felt is wasn't the right thing to do? I have yet to receive an answer for that from any ignorant bank defender..and don't expect to.

Many banks are now allowing opt out of OD protection...some are not going to re-sequence transactions anymore as it is proved unnecessary and only a means for the bank to tack on more fees....some banks are now limiting the amount of OD fees they will charge per day..and some are not charging anything if the overdraft is under a certain amount.

Anyhow you might want to consider opting out of overdraft protection as an extra safeguard. Ask the bank if they will allow you to. Worse they can do is say no.

Now I can't say you hold no responsibility..you must be more careful of your balance..and you now are fully aware of what this bank does if you overdraft for any reason..even if by deceptions and manipulations and excessive hold times...so just be careful. I don't have to insult you or anyone else to get this point across...those who do just show signs of weakness...and enjoy bulling others around since it is "safe" for them here. In person I would bet they are quite cowardly so pay them no mind. The ONLY people who agree with them..are other close-minded unforgiving nasty bank defenders..the rest know the real "truth".

#7 Consumer Comment

RE: WOW

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Wednesday, October 28, 2009

First of all READ my post I said nothing about me writing checks or nothing about using overdraft or nothing about not keeping track of my money

- Do you even know what you wrote?

No matter what you do write a check, use ATM, or get cash from the Teller ,

- So you talk about writing a check, yet it is not about YOU writing a check? So if you don't write checks what proof do you have that they hold checks for 5-7 days?

Issue NO.3 - OD fee

- Well correct me if I am wrong, but isn't the only way to get OD fees is if you are in Overdraft?

As for the rest about you saying nothing about not keeping track of your money. That was the point. Your post and update make it appear as if you are relying on the bank to tell you when you are out of money. This is a recipe for disaster especially if you use the Debit Card and keep low balances. I would suggest that you ask your new bank about their courtesy Overdraft Protection, and if you have the ability to "opt-out". If they do let you opt-out I suggest you do. It won't guarantee you can't get hit with fees, but at least it would minimize the fees when they do occur.

I want my transactions to be completed when I pay them is that hard to understand?

- No it actually makes sense, however that is NOT how it works. Even at your new bank I can guarantee you that your purchases are not POSTED immediately.

Don't go putting down people till you have walked a mile in their shoes, don't judge someone till you know them personally.

- How do you know I haven't over drafted or have been hit with fees in the past? The difference is that when I was I didn't automatically blame the bank. I figured out what I needed to do and have made very sure to never be hit with these fees since.

It is great that you found a bank that works for you right now. However, if you do rely on the bank and not your own register, this same situation will happen again. So we will be waiting here on a report on that bank as well. It may not be today or even this month, but odds are it will happen. It will be interesting to see how nice you think the bank is then.

#6 Author of original report

WOW~!

AUTHOR: hatebanks - (USA)

SUBMITTED: Wednesday, October 28, 2009

Wow I cannot believe how sad it is that I served my country for 20 years , went to war 2 times was deployed away from my family 12 times just to protect the rights of retards like you? OMG! If I had known (and prolly every soldier that ever served in WWI, WWII, Korea and NAM) That we would be responsible for letting Morons Breed in the USA we would have just said forget it! let Germany take over at least they will stop retard breeding!

First of all READ my post I said nothing about me writing checks or nothing about using overdraft or nothing about not keeping track of my money.I have had many diffrent bank accounts over the years because of getting deployed to many diffrent duty stations and I have NEVER had any problems with any bank I ever had till now what does that tell you retards? I am sorry if you work there and I am insulting your workplace but I am hoping educated people read this post and steer clear of this bank I could care less if you MIKE and your annomous lover there argue till your face is blue. Today there is no customer service anymore companies only care about 1 thing MONEY! If you have a billion customers who cares if you loose 100-300 customers? I want my transactions to be completed when I pay them is that hard to understand? I want that money out of my account that day not pending for weeks. It is not an issue of overdraft or not keeping record of my money, It is common sense if I pay some one I no longer have the money on me I don't want to see it pending and I don't want the bank to tell me that money is still in my account , none of the other banks I have ever had did it. People are humans and we ALL make mistakes..yes even you Mike..so why put down people for making mistakes? I tell you what you post a complaint about something and I will post a rebuttle on it showing you how wrong you are and see how it makes you feel? Don't go putting down people till you have walked a mile in their shoes, don't judge someone till you know them personally.

Go ahead and say what you want I don't care anymore I have seen and done more in my life than you can ever dream about and I am thankfull for that cause that makes me a better person for it.

By the way I did switch banks and my new bank is wonderful , they treat me like a person not a number and my transations are up to date and I have no complaints about them at all. - see things work out for the best so go and breed some more retards and I hope they all get bank accounts at Woodforest and I hope they thank you for reccomending them to your bank.

#5 Author of original report

WOW~!

AUTHOR: hatebanks - (USA)

SUBMITTED: Wednesday, October 28, 2009

Wow I cannot believe how sad it is that I served my country for 20 years , went to war 2 times was deployed away from my family 12 times just to protect the rights of retards like you? OMG! If I had known (and prolly every soldier that ever served in WWI, WWII, Korea and NAM) That we would be responsible for letting Morons Breed in the USA we would have just said forget it! let Germany take over at least they will stop retard breeding!

First of all READ my post I said nothing about me writing checks or nothing about using overdraft or nothing about not keeping track of my money.I have had many diffrent bank accounts over the years because of getting deployed to many diffrent duty stations and I have NEVER had any problems with any bank I ever had till now what does that tell you retards? I am sorry if you work there and I am insulting your workplace but I am hoping educated people read this post and steer clear of this bank I could care less if you MIKE and your annomous lover there argue till your face is blue. Today there is no customer service anymore companies only care about 1 thing MONEY! If you have a billion customers who cares if you loose 100-300 customers? I want my transactions to be completed when I pay them is that hard to understand? I want that money out of my account that day not pending for weeks. It is not an issue of overdraft or not keeping record of my money, It is common sense if I pay some one I no longer have the money on me I don't want to see it pending and I don't want the bank to tell me that money is still in my account , none of the other banks I have ever had did it. People are humans and we ALL make mistakes..yes even you Mike..so why put down people for making mistakes? I tell you what you post a complaint about something and I will post a rebuttle on it showing you how wrong you are and see how it makes you feel? Don't go putting down people till you have walked a mile in their shoes, don't judge someone till you know them personally.

Go ahead and say what you want I don't care anymore I have seen and done more in my life than you can ever dream about and I am thankfull for that cause that makes me a better person for it.

By the way I did switch banks and my new bank is wonderful , they treat me like a person not a number and my transations are up to date and I have no complaints about them at all. - see things work out for the best so go and breed some more retards and I hope they all get bank accounts at Woodforest and I hope they thank you for reccomending them to your bank.

#4 Consumer Comment

TD...

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Monday, October 26, 2009

I personally agree with you on this. After all if a person wants the bank to stop them from spending money they don't have, they should do it for every transaction. After all we are talking common sense right.

So if a $300 check comes in, and they have $100 in their account, if they "opted-out" of Overdraft Protection the bank should honor that request in all cases. Yes this means returning the check. However, from what I have been looking at the banks didn't get enough backbone to do that. Unfortunately I still don't think that it would click with some people that they actually did something wrong. As a result it would just change these reports from the Banks to companies like Telecheck, SCAN, or ChexSystems that are charging them Returned Check fees.

Oh and I have also seen the Debit Card declined..whip out the Checkbook more than once myself. Which does make you want to say Doh! Because we all know that the bank will let you spend and spend and spend. So for them to get to the point of the bank actually shutting them off you know they are already pretty deep.

#3 Consumer Comment

Robert, I say we let them 'opt out' of check overdrafting as well...

AUTHOR: Truth Detector - (U.S.A.)

SUBMITTED: Monday, October 26, 2009

This will add some new fun to the equation, will it not?

First, by virtue of their proven deadbeat ways, it is inevitable that they will write a check to cover a declined debit card transaction. I have witnessed this many times at grocery stores. A customer will use the debit card, it will be declined, and the same moron will write a check from the same bank account (Most merchants will not allow the check to be issued - causing the deadbeat to ask for a manager, who promptly tells the deadbeat CASH ONLY).

Hello, McFly? You obviously don't have enough money in the account to make the purchase because your debit card was declined. Therefore, you write a check that is certain to bounce?

Personally, I hope they let these people opt out of ALL overdrafting. When their checks bounce and the merchant presses charges, those piddly little $35.00 fees will be a wet dream compared to the fines they pay and/or jail time they will do for writing bad checks (Remember, once that debit card was declined, they just knowingly wrote a check for which they did not have the funds to cover. That's a FELONY in some states).

And just for good measure, when their accounts are closed and they are reported to Chex, they will keep the local check-cashing store in business paying $25.00 a pop to cash their payroll checks.

Play it safe, people. Use a check register. Be an ADULT. Exercise some RESPONSIBILITY.

#2 Consumer Comment

Robert, I say we let them 'opt out' of check overdrafting as well...

AUTHOR: Truth Detector - (U.S.A.)

SUBMITTED: Monday, October 26, 2009

This will add some new fun to the equation, will it not?

First, by virtue of their deadbeat overdrafting habits, it is inevitable that they will write a check to cover a declined debit card transaction. I have witnessed this many times at grocery stores. A customer will use the debit card, it will be declined, and the same moron will write a check from the same bank account.

Hello, McFly? You obviously don't have enough money in the account to make the purchase because your debit card was declined. Therefore, you write a check that is certain to bounce?

Personally, I hope they let these people opt out of ALL overdrafting. When their checks bounce and the merchant presses charges, those piddly little $35.00 fees will be a wet dream compared to the fines they pay and/or jail time they will do for writing bad checks (Remember, once that debit card was declined, they just knowingly wrote a check for which they did not have the funds to cover. That's a FELONY in some states).

And just for good measure, when their accounts are closed and they are reported to Chex, they will keep the local check-cashing store in business paying $25.00 a pop to cash their payroll checks.

Play it safe, people. Use a check register. Be an ADULT. Exercise some RESPONSIBILITY.

#1 Consumer Comment

The grass is always greener..NOT..

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Monday, October 26, 2009

Issue no.1 - Pending charges - No matter what you do write a check, use ATM, or get cash from the Teller , they put those transactions as pending for 5-7 days which puts you in a bind when you have no idea when that money is coming out even after I received receipts from the people I was paying saying they have their money It still says pending..at other banks when you use their services it comes out that day!

- Wow, so I guess that every other report that says the same thing about their bank is lying? Or could it be that it actually does depend on the merchant to put through the final debit. Oh there is a real simple way to know when the money will come out of your account. Treat it as it came out as soon as you swipe your Debit Card or write a check.

Hmmm something to think about

- Yes..let's think about it. You do not use a check register do you? Because it appears that you are relying on the bank to tell you when you are out of money instead of taking responsibility for your own money. Guess what it does not matter how long an item is pending. If YOU write down the transaction when you make it YOU know it is unavailable to use. Now, the good news for you is that banks are changing and you will be able to "opt-out" of this protection. However, if you do not keep a register you will still have Overdraft fees. Because it will only stop you from using your Debit Card if you are currently at or below $0, and does not cover any checks that you have written.

Related Reports

07:19 PM

Jalandhar

09:08 PM

WILLIAMSBURG, Virginia

10:09 AM

WILLIAMSBURG, Virginia

06:32 AM

07:59 AM

01:40 PM

05:08 PM

10:21 AM

08:25 PM

09:47 AM

12:46 PM

06:34 AM

07:57 AM

04:22 PM

10:20 AM

09:01 PM

10:44 PM

10:43 PM

02:29 PM

09:39 AM

09:52 AM

06:36 AM

01:58 PM

06:13 PM

06:34 AM

Advertisers above have met our

strict standards for business conduct.