Complaint Review: Fingerhut - St Cloud MN

- Author Confirmed

- Fingerhut 6250 Ridgewood Rd St Cloud , MN United States

- Phone: 1-800-208-2500

- Web: www.fingerhut.com

- Category: Online credit card, Credit, Credit Bureau, credit report scores, Credit score reporting, Credit Card Fraud

Fingerhut FAKE Increases Without Permission to DAMAGE Credit LONGTERM St Cloud MN

*Consumer Comment: The OP is not kidding.

*Author of original report: It's the real reason

*Author of original report: Wow Fingerhut, that the best you got?

*Consumer Comment: I use Fingerhut

*Consumer Comment: Typical Subprime Borrower

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

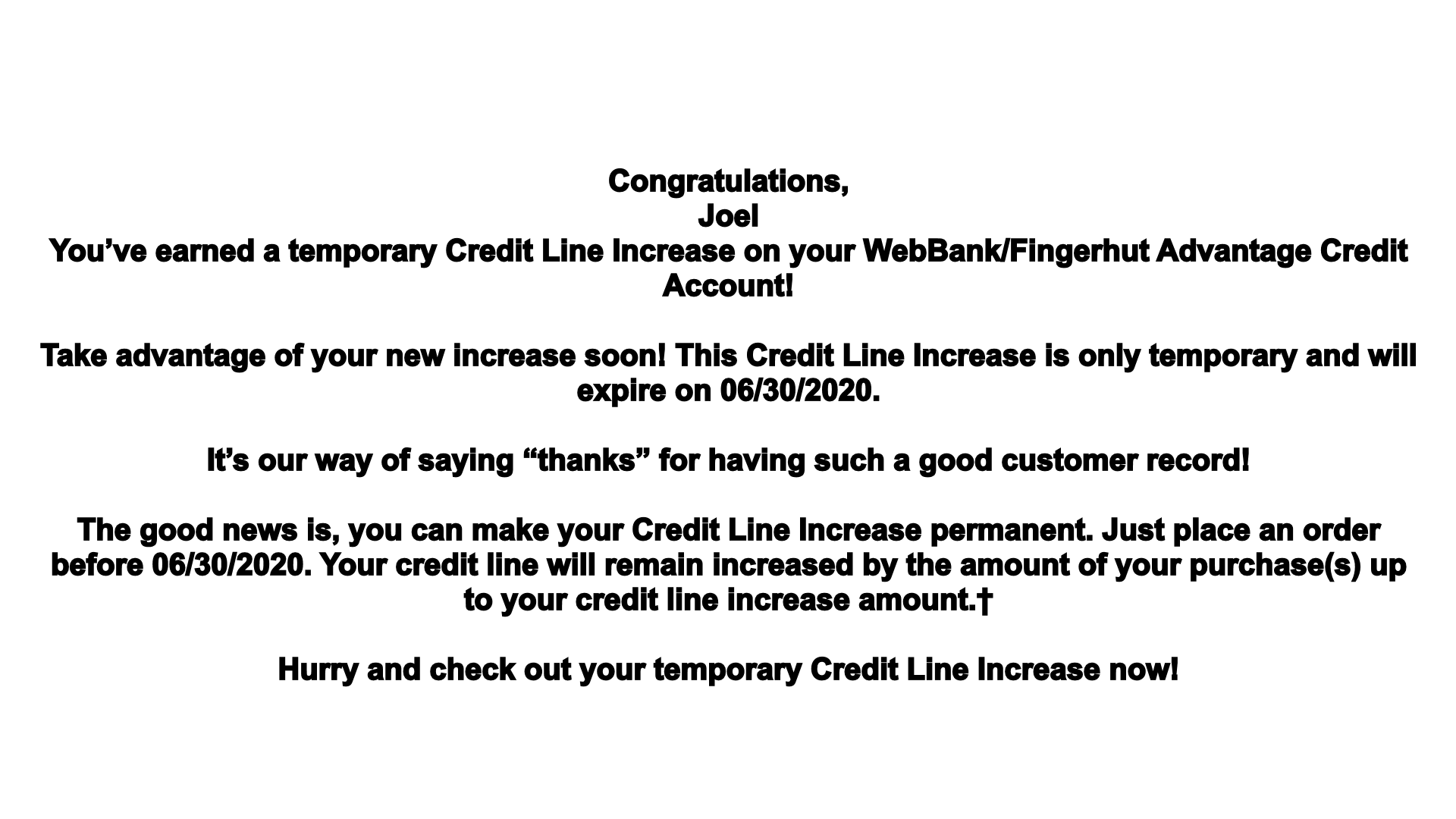

Fingerhut tells us our Credit Score is important. you and they are right, CREDIT SCORE IS IMPORTANT. So why do they intentionally tryi to hurt the scores of their good customers? I have NEVER been late on a payment and have received SEVERAL Credit Line Increases. NOW I get a "Temporary" FAKE $800.00 Credit Line Increase which WILL be reported to all Three Credit Reporting Agencies and INCREASE my Credit FICO by approximately 20 points.

Then see that Credit Line DECREASE to my present line in 3 months. Be Reported to All Three Credit Agencies Again and see a 30 point DECREASE in my FICO. In other words they are telling me I MUST OVERSPEND by $800.00 and not use my Credit responsibly OR they will (1) cost me 10 points on my FICO Score Long Term, OR (2) Remove me from receiving any future REAL Credit Line Increases. That per thier Supervisor, (after the original person gave up) and giving me only his first name PAUL and badge #154, of 6250 Ridgewood RD, St Coud, MN 56303.

He basically said Fingerhut could care less what you do in regard to Consumer Credit. I asked him if he would accept these terms on any of his accounts with ANY company. And he said he would need to read their Terms and Conditions. Good dodge so I asked him where in the Terms and Conditions for Fingerhut these FAKE increases appear? And where it says Fingerhut is allowed to impose them? He said, "well it doesn't actually say that." Ya think?? Of course it doesn't. So again, WHY do they want to HURT the Credit of their Best Customers? You know, the ones that pay ontime each and every month Why hurt the Credit of the Customers that PAY On Time? And why force customers to either hurt themselves Short term financially OR Limit themselves Longterm? Paul sure didn't know, and I'll add DIDN'T CARE. But maybe someone with their group will!!

This report was posted on Ripoff Report on 04/10/2020 03:52 PM and is a permanent record located here: https://www.ripoffreport.com/report/fingerhut/st-cloud-mn-fake-increases-1493917. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#5 Consumer Comment

The OP is not kidding.

AUTHOR: Don - (United States)

SUBMITTED: Monday, January 11, 2021

They have been doing the same thing to me for 2 years now. Started my account after BK and was given a 200.00 limit. They gave me an increase to 500 in 6 mos. then ever other month after that, temporary increases started showing on my account and credit score. One time I actually made a purchase for a large item and the increase stayed. But 4 times in 2 years fingerhut gives me a Temp raise in limit and I don't need anything so I don't spend and then they take the increase away. Last time was this past december 31. An increase of 2200.00 up from my 1250.00 limit. Increased my score by 25 points but didn't want or spend anything of it.

They took away the increase and as son as it hit the big 3 my score dropped 40 pts. because of avail credit amount and usages that was 25% was increased to 55%. There has to be a law regarding this. I am doing some research and will post more information when I get it.

#4 Author of original report

It's the real reason

AUTHOR: Joel - (United States)

SUBMITTED: Sunday, April 12, 2020

If someone knows anything about Credit, you keep cards under 30% as that accounts for 30% of your Credit Scoring on each account and 30% totals on all combined accounts, 30% of your overall Credit Score. And that is REGARDLESS of your Credit Score. People understanding the basics of Credit adhere to how the system works in order to get the best score possible.

At time 10 points is important (Mortgage for instance), sometimes not as much. But ALWAYS worth protecting if you have any sense whatsoever. Rate increases = Good, Decreases = Bad. 100% of the time. Anyone not understanging the basics of the system. Look it up.

#3 Author of original report

Wow Fingerhut, that the best you got?

AUTHOR: Joel - (United States)

SUBMITTED: Saturday, April 11, 2020

Notice the actual complaint which deals with Raising the Credit Score (short term) then lowering it longterm wasn't really addressed. So, anyone saying they don't understand FICO and how it works read carefully. When ANY account has its Limit Raised and is reported to the Reporting agency. Your Score automatically rises because

(1) you pay on time and earned the increase, and

(2) you credit ratio (debt vs limit) is reduced. That's a good thing. But if a company DECREASES your Credit Line, each of those same two factors are calculated against you. And if anyone has any real expereince with the Reporting agencies they know for a fact the negative total is ALWAYS greater then the positive. That really is Cresit 101 for beginners. SO, my choice was BUY something for $800 on a temporary FAKE increase by June 30th OR have my Credit Line decreased on July 1st, Leading to a reduction in Credit Score for using my Credit RESPONSIBLY. Now if some genius thinks that's a good choice and wants to play the game while obviously not understanding the process to learn a very bad lesson. Raise your little hand.

For those that understand, and especially for those that don't. Here's the text from the e-mail.

#2 Consumer Comment

I use Fingerhut

AUTHOR: Stacey - (United States)

SUBMITTED: Saturday, April 11, 2020

Make my payments every two weeks and have had no decrease in my FICO score because I PAY them. So what is the real reason you wrote this report when you state you payed on time every time?? These "fake" credit increases is just asking you to spend more money. IF you do not then hey, no big deal. SO what is the real story?

#1 Consumer Comment

Typical Subprime Borrower

AUTHOR: Robert - (United States)

SUBMITTED: Saturday, April 11, 2020

He basically said Fingerhut could care less what you do in regard to Consumer Credit.

- They are right...just like every other credit card. They don't care what the affect on your credit score is by their actions.

Good dodge so I asked him where in the Terms and Conditions for Fingerhut these FAKE increases appear? And where it says Fingerhut is allowed to impose them? He said, "well it doesn't actually say that." Ya think??

- Typical Strawman Argument. Of course it doesn't state that they can put in a "fake" increase. The credit increase was real, you could use the extra $800 if you chose to. Your score increase is based on the increased credit line causing your credit utilization to go down. Once they reduce your credit line, your utilization is based on your new lines. If you haven't paid your balances down your utilization increases causing your score to decrease.

But the customer service agent was wrong. The Terms do actually allow them increase or decrease your credit limit at THEIR option and for any reason. They could close your account out or reduce your credit line to $100 tommorow if they wanted to. They are the ones taking the risk on extending you credit with their money, and they can change that amount at any time. Oh..and this is what you agreed to when you opened the account.

If you are worrying about a 10 point change in your FICO your credit must really be in the toilet. Unless your FICO is around 620 or less a 10 point change is insignicant. Of course if your score is in that range that explains why you are with a Sub-Prime Creditor and worrying about a 10 point change.

There is nothing unique here, this is how ALL credit cards work.

* If you don't know what a Strawman argument is...go look it up

Related Reports

12:20 PM

12:07 PM

08:42 AM

07:33 PM

01:30 PM

12:11 PM

01:27 PM

09:02 AM

09:34 AM

09:44 PM

08:37 AM

09:24 AM

12:26 PM

03:11 PM

08:16 AM

06:03 AM

02:53 PM

08:48 AM

01:30 PM

06:24 AM

10:35 AM

06:31 AM

08:02 PM

08:23 PM

Advertisers above have met our

strict standards for business conduct.