Complaint Review: Compass Bank - Birmingham Alabama

- Author Confirmed

- Compass Bank P.O. Box 10566, Birmingham, Alabama U.S.A.

- Phone:

- Web:

- Category: Banks

Compass Bank Ripoff Unfair and Deceptive Deposit Procedure to encourage NSF Fees Birmingham Alabama

*UPDATE EX-employee responds: Lesson Learned

*Consumer Comment: Keeping track of checks doesn't work...

*Consumer Comment: Compass can and will scam you.

*Consumer Comment: Compass bank will ripoff customers with excessive NSF fees- if not illegal, certainly unjust

*Consumer Comment: Compass bank will ripoff customers with excessive NSF fees- if not illegal, certainly unjust

*Consumer Comment: Compass bank will ripoff customers with excessive NSF fees- if not illegal, certainly unjust

*Consumer Comment: Compass bank will ripoff customers with excessive NSF fees- if not illegal, certainly unjust

*Consumer Comment: I agree their terms are deceptive

*Consumer Suggestion: The best way to settle this

*Consumer Suggestion: Please help me understand

*Author of original report: My final thoughts about Robert & Compass Bank

*Consumer Comment: I don't disagree.

*Author of original report: Response to Robert's response.

*Consumer Comment: There are things you can do.

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

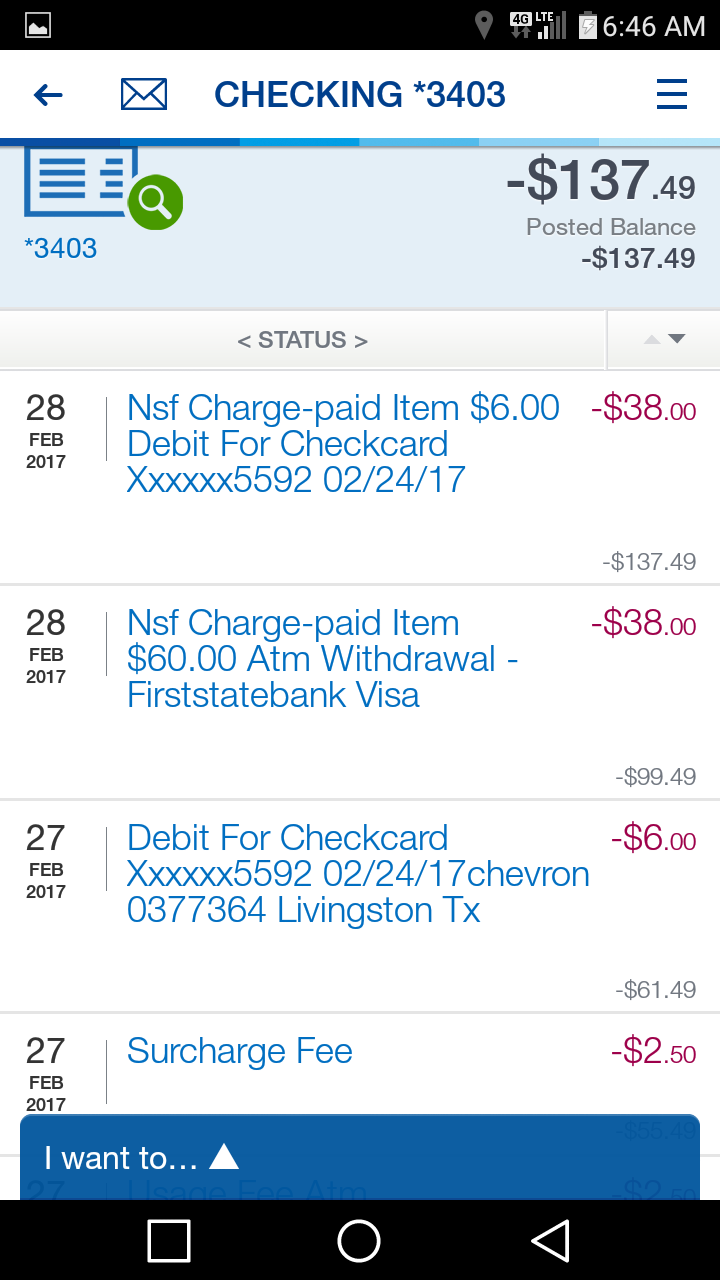

Compass Bank intentionally uses unfair practices in the way it handles the daily reconciliation of customer's accounts. They purposely use a procedure that makes the customer incur the most NSF Fees possible.

Compass Bank holds all customer deposits, including cash, checks and EFT's for one day longer than necessary and does not apply them to the customers account in a timely manor. When they do apply credits and debits to there customers accounts they do not use a fair practice. They remove debits first taking out the largest amount first and work their way down to the smallest amount. After all of the Debits are removed (and NSF Fees are applied) then they apply credits to the account in order of smallest to largest. These Debits and Credits are all done with complete disregard to the order in which they were completed. By doing this Compass Bank makes the account balance as low as possible so multiple NSF Fees can be incurred by the customer. I also noticed that all EFT Transfers I do to Compass Bank take 1-2 days longer to hit my account than they do to my other banks.

This practice allows Compass to offer FREE CHECKING to its customers because it knows customers will pay more in NSF Fees than they could ever make charging a minimal monthly fee. It also allows them to attract customers that might be more likely to have smaller bank accounts (and incur more NSF Fees) because these customers would see more value in saving a couple of bucks a month.

This unfair and deceptive business practice should be seen for what it is, a way for Compass Bank to make money off innocent people trying to make their daily finances work. All of their employees seem to know about this practice, yet none of them will give you more than an unsympathetic I'm sorry you feel that way if you mention it. STAY AWAY FROM COMPASS BANK!!! They DO NOT have "FREE CHECKING"!

Dylan

Mesa, Arizona

U.S.A.

This report was posted on Ripoff Report on 05/16/2006 02:39 PM and is a permanent record located here: https://www.ripoffreport.com/reports/compass-bank/birmingham-alabama-35296/compass-bank-ripoff-unfair-and-deceptive-deposit-procedure-to-encourage-nsf-fees-birmingha-191804. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#14 UPDATE EX-employee responds

Lesson Learned

AUTHOR: Bill - (U.S.A.)

SUBMITTED: Sunday, July 29, 2007

Read all disclosures before you sign anything!! Ask questions??? Don't assume anything every business is different even if they are in the same field of business. Not every bank is the same. Shop before you buy. So you can accurately understand what they are asking of you.

#13 Consumer Comment

Keeping track of checks doesn't work...

AUTHOR: Kelli - (U.S.A.)

SUBMITTED: Monday, June 11, 2007

I've been researching Compass Bank for the past few weeks, preparing to go in and deal with my seriously overdrafted bank account this morning. I'm hoping to go in with some insight that will keep me from saying something to them that will not only exacerbate the problem but get me arrested as well (you know, idle threats of bodily harm and that sort of thing).

I am so tired of hearing from commenters that to solve our problem "just don't bounce checks". Are you idiots? Do you honestly think that we LIKE forking over our hard earned money so that Compass can show the world what an up and coming bank they are (reports say they made something like 1.6 billion dollars in 2006. Want to guess where all of that money came from?)

When bank fees are not honest fees, keeping track of what you spend is a moot point. There is a problem when I meticulously keep track of every penny that goes in and out of my account, keep a to-the-minute accurate check register, and then sign onto my bank account to find not one, but several NSF charges. Keeping track of my checks does nothing to prevent theft by my own banking institution.

The online banking account that I can access to find out what has cleared and what has not is a "courtesy" they tell me, and is in no way an accurate or legally binding account of what I have in the bank, unless, of course, it says that I owe them money. I have printed that account and taken it in for an explanation and have been shown THEIR computer and told that I had it all wrong. I have been able to slap print outs in front of them showing them that they levied NSF fees against checks that were still enroute in the mail, and they have told me that I was mistaken and they are right and I owe them the money. How does keeping an accurate check register prevent that?

BTW, if you do your banking with a program like Microsoft Money or Quicken, do not access your bank account with that program. You give the bank access to your register, and, in Compass's case, they will exact fees based on what your register says rather than what has cleared, thus exacting fees against checks that are still on their way to their destinations in the mail.

Now I have to go down there and be civil despite the fact that banking with them over the last year has worn down my self-confidence, caused marital problems, and has possibly cost me my promotion at work (they're concered about my handling money while I am in financial trouble).

So, if you want to think that we are all just careless fools, go ahead and bank with Compass. When you come back mumbling around your foot, we'll be sure to remind you that you wouldn't have had a problem if you just didn't bounce any checks.

#12 Consumer Comment

Compass can and will scam you.

AUTHOR: CJ - (U.S.A.)

SUBMITTED: Friday, November 10, 2006

I had Compass bank over two years ago for 3 months and they are the worst bank I have ever dealt with. They have lost cash deposits (due to courier loading the deposits onto the wrong plane), dated a cash deposit for 1 day in the future (teller accidently set it a day ahead). These two fiascos cost me NSF fees that I had to take time off work to get refunded.

You can 18.00 in the bank at 9:00 a.m. in the morning, make a cash deposit at 9:01 a.m. for $100.00. You think your balance is $118.00 so that you can make purchases, think again. If you purchase anything over that $18.00 you had originally in the bank at opening of the banking day, you will be charged an OD/NSF fee. It is called maximizing profit. It is a computer algorithm that is written by programmers and implemented by banks. I had to write one for my CS class several years ago.

It doesn't matter if you balance your check book or not. You have to be aware of the banking posting procedures and plan your expenditures accordingly.

I have banked with Wells Fargo, Bank of America, Netbank, etc. and they have never pulled the stuff on me that Compass Bank did in those few months.

#11 Consumer Comment

Compass bank will ripoff customers with excessive NSF fees- if not illegal, certainly unjust

AUTHOR: William - (U.S.A.)

SUBMITTED: Friday, November 10, 2006

Compass preys on lower income people by charging excessive NSF fees. They will explain to you that "it is just how the computer works," that is rediculous. This is a scam, it may be legal, but it is wrong. I went $4.00 negative and immediately made a transfer from savings to checking to clear it. Then as you all know I spent a few dollars here and there and got 36 fees. I made several deposits to keep my account positive, but the NSF fees s****.>

#10 Consumer Comment

Compass bank will ripoff customers with excessive NSF fees- if not illegal, certainly unjust

AUTHOR: William - (U.S.A.)

SUBMITTED: Friday, November 10, 2006

Compass preys on lower income people by charging excessive NSF fees. They will explain to you that "it is just how the computer works," that is rediculous. This is a scam, it may be legal, but it is wrong. I went $4.00 negative and immediately made a transfer from savings to checking to clear it. Then as you all know I spent a few dollars here and there and got 36 fees. I made several deposits to keep my account positive, but the NSF fees s****.>

#9 Consumer Comment

Compass bank will ripoff customers with excessive NSF fees- if not illegal, certainly unjust

AUTHOR: William - (U.S.A.)

SUBMITTED: Friday, November 10, 2006

Compass preys on lower income people by charging excessive NSF fees. They will explain to you that "it is just how the computer works," that is rediculous. This is a scam, it may be legal, but it is wrong. I went $4.00 negative and immediately made a transfer from savings to checking to clear it. Then as you all know I spent a few dollars here and there and got 36 fees. I made several deposits to keep my account positive, but the NSF fees s****.>

#8 Consumer Comment

Compass bank will ripoff customers with excessive NSF fees- if not illegal, certainly unjust

AUTHOR: William - (U.S.A.)

SUBMITTED: Friday, November 10, 2006

Compass preys on lower income people by charging excessive NSF fees. They will explain to you that "it is just how the computer works," that is rediculous. This is a scam, it may be legal, but it is wrong. I went $4.00 negative and immediately made a transfer from savings to checking to clear it. Then as you all know I spent a few dollars here and there and got 36 fees. I made several deposits to keep my account positive, but the NSF fees s****.>

#7 Consumer Comment

I agree their terms are deceptive

AUTHOR: Kyle - (U.S.A.)

SUBMITTED: Saturday, October 21, 2006

Compass is the only bank that I am aware of that does this debits first credits last deal.

You deposit cash, it should be availalbe instantly. They purposely try to hook you on some OD fees if they can, I think its a very shady practice.

I had compass for a short 2 week time, they pulled the same stunt on me, but it was a case where there was enough available and I was taking meticulous records of what I had spent, they somehow figured out a way to retroactively insert 1 $36 fee in the right spot that caused a chain reaction of about 10 more fees, there was enough money + $100 in the account to cover everything.

Of course I went in there and raised hell and they refused to refund even one fee.

The bottom line is, they really do not care about what is best for the consumer, they want what will increase their bottom line the quickest, and they will act like its your fault for them being shady.

I went to a local credit union, and guess what, I have exactly 0 problems with them. I had one overdraft, it cost me a whopping $20. I make any sort of deposit, whether it be a check or cash its available instantly and they do not try to pull this whole game that compass does.

BOA and Wells Fargo are pretty bad and insensitive to customers needs, but Compass is in a class of its own, they truely are at the bottom of the barrel in my eyes.

Customers are just cattle to them, to be harvested of every penny they can sqeeze out. DO NOT TRUST THEM!!

#6 Consumer Suggestion

The best way to settle this

AUTHOR: Anna - (U.S.A.)

SUBMITTED: Tuesday, October 17, 2006

Free checking is free as long as you don't bounce any checks. A checking account is NOT a credit card. I know it may sound a bit uppity, but the idea is to not spend money that you don't have. At times that may not be possible. But then again, if the bank is willing to pay for your financial discrepancies at all (instead of simply refusing the payment) then that should be worth paying a few extra bucks for.

I am a customer of Compass and am in no way affiliated with them otherwise. If you ask me they really do have the best deal. I once had an account with another bank where I was charged $2 a month plus $.25 for each check I wrote, plus an extra $6 a month simply for having a debit card, plus $2-3 for each time I used another bank's ATM, plus $12 each time I had to reorder checks. I no longer pay any of those fees. And at my local Compass Bank I have always received excellent service.

I'm not trying to be a jerk, but just don't bounce any checks and you'll have a lot less to worry about.

#5 Consumer Suggestion

Please help me understand

AUTHOR: Melissa - (U.S.A.)

SUBMITTED: Saturday, October 14, 2006

I've gone over my consumer deposit agreement with a fine toothed comb and it says nothing about a policy of processing debits before credits. It does say that their policy is to make funds that the customer deposits available on the day of deposit for the payment of checks presented through normal check collection channels.

Funds deposdited into the account generally can be withdrawn by other means on the following business day. This isn't what the customer service people are telling me. They are saying that if a check is presented after a deposit, but I wrote it before the deposit posted (not when they receive the deposit or even say it is available), then it will be processed first.

I even went to the branch and specifically asked for the latest, most up-to-date disclosure. They gave me a one page fee schedule which says nothing about funds availability. So I went back and asked for their funds availability policy, and they gave me a 30 page brochure on my consumer deposit agreement.

I asked three customer service people when this policy was disclosed to me and none of them could tell me if it ever was disclosed.

#4 Author of original report

My final thoughts about Robert & Compass Bank

AUTHOR: Dylan - (U.S.A.)

SUBMITTED: Thursday, May 18, 2006

Robert, what does any of that have to do with my statement? I never mentioned anything about defaulting on contracts or being released from any contractual agreements (don't even start me on binding arbitration). You are the one that even brought up the whole contract issue to begin with. I believe this is a business ethics issue, not a contract law issue. To the contrary of your assumption, I admitted that Compass Bank was under no obligation to return any of my fees, nor did I expect them to. I also don't believe I was claiming ignorance of a bank (or any companies) policy as an excuse for anything.

I have actually pointed out the same thing that you have; it is up to the consumer to find out what they are getting themselves into. Unfortunately, it is almost impossible for an average consumer to analyze every policy and procedure of any banking institution to determine its impact on their particular situation. In an ideal world every person would be as smart as you and never have this problem. As you are so obviously aware, nobody is as smart as you, because you know everything and don't care how a company does business as long as they can defend themselves in court. Since this is not a perfect world, we all go on like lemmings expecting the companies we do business with to actually have ethics. Fortunately most companies do practice good business ethics because they realize that consumer good will is a valuable commodity. When a business decides that their bottom line is more important than customer service they should expect customer backlash. Most companies would take situations like this and try to spin it into a positive by changing there policy and releasing a grandiose press release touting their dedication to customer service. Compass Bank prefers to give their customers the finger and kick them in the a** as the go on to do business with someone else.

While you choose to consistently attack the messenger, and completely ignore the message, I would rather try to deliver the message to as many people as possible. The message is STAY AWAY FROM COMPASS BANK!!! If this is the message Compass Bank wants its customers sending out, then I really don't care if they change or not. If other people can avoid Compass Bank through the dissemination of information on this site, great that is why it is here. I am all too happy to help even one person save themselves the trouble of dealing with an uncaring, poor quality bank. Your way of helping people appears to be pointing out how dumb they are for getting into the situation to begin with. I guess we just have different opinions about how we can educate consumers.

Oh, by the way, to answer your pointless questions you asked in your reply; as a business owner I do not attempt use a contract for the purpose of getting someone to agree to something that is not the industry standard just so I can say Sorry, you should have read the contract better. I also do not intentionally market my products and services to a consumer group that I know I can take advantage of just to make a buck. I make my money the old fashioned way; I offer a quality product at a fair price and back it up with customer service. It is not rocket science, but it does seem to still work.

So instead of chastising people for making bad decisions why don't you get of your high horse, shut the hell up and let people express their opinions without trying to make them feel stupid. If you truly have no interests in Compass Bank what purpose could any of your posts on this site serve except to inflate your pampas ego? That was a rhetorical question; I seriously hope you don't feel any need to reply as I truly don't care.

I could be wrong, please forgive me if I am, but I see that you have posted rebuttals to several posts about Compass Bank complaints. Looking at complaints about other banks I could not find any posts from you. Why does it appear that other banks are not worth defending, but Compass Bank must be defended at all costs?(also rhetorical) If you are not being compensated by Compass Bank for your work, you might want to approach them about it as you could probably work freelance for there Public Relations department. I don't think you would cut it in Customer Service for them as you do seem to be educated and some what polite (not traits they appear to be looking for in CS).

Compass Bank may continue to go on making large profits (which I personally love) by charging outrageous fees and using the over-played marketing of the word FREE in everything they do forever if they like. I would just point out to them that they do obviously have some PR problems whether they admit it or not. Most other large banks have realized that they are now more of a retail service business than a financial institution. Compass Bank refuses to embrace the new retail sales culture in the banking industry and it is going to hurt them if they don't change. Compass bank needs to realize that fancy marketing campaigns are NOT customer service. Just because new customers flock in for all of the free gimmicks they offer, it doesn't mean there churn rate won't go through the roof and eventually run the well dry. Many good companies have made this mistake and I see it coming for Compass Bank. I would warn their executives and board members that this usually ends in a merger (AKA Acquisition) with a better run company resulting in a change in management and culture.

I must go now as I have already wasted more time on this matter than I ever intended to. Please feel free to continue wasting your time defending this bank as you see fit, but please forgive me for no longer carrying about or responding to your posts. Good Day.

#3 Consumer Comment

I don't disagree.

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Thursday, May 18, 2006

I do not now nor do I ever plan to have an account with Compass, BOA, Wells Fargo, Wachovia nor any other national banking institution for the very reason that their terms are unacceptable.

So as a business owner you have no problem if a new customer or vendor defaults on a contract simply because they didn't read it before or after they signed it? You would let them without penalties?

My only point being, that as a consumer it is my responsibility to be aware of what I have agreed to and what rights I have waived. Claiming ignorance of a banks policies doesn't cut it. If the bank doesn't give you their policies, ask for them. If they don't provide them when asked, go elsewhere for your banking needs.

It seems people don't put much thought into who they have handling their money.

The bank is not my accountant or bookkeeper. They are acting as my agent to process financial transactions as directed by me. If the bank is not doing so in a timely manner per the account terms, I'll raise holy hell. If there are still problems that seem to reoccur then I'll move on to another bank that works for me.

#2 Author of original report

Response to Robert's response.

AUTHOR: Dylan - (U.S.A.)

SUBMITTED: Wednesday, May 17, 2006

Robert, while I appreciate your uncontrollable urge to defend Compass Bank to the end (which I personally hope is soon). You do not need to patronize me as if I am an idiot that can't balance a check book and understand contracts. I am the owner or president of three companies and have direct financial control over two of these companies. I also currently do business with four different banks/credit unions (was five until I closed the Compass Bank account yesterday) and have never in my twenty years in business had an NSF charge until I made the mistake of doing business with compass bank. So please spare me your empathetic instructions on how to pick a bank.

As nice as your response sounds, it does not address the issue that Compass Bank has a policy that directly and intentionally costs its customers money. Using a check register is a great idea, however when a business is processing thousands of dollars each day with multiple deposits and credits going through everyday it is imperative that bank transactions are completed in a timely fashion. Compass Bank either refuses to update their procedures/computers to make this happen (as it does at every other bank I have ever used) or it doesn't want to.

I see in your MANY replies to unhappy Compass Bank customers that you like to build the straw man argument that the customer can't spend money that they don't have in their account and that the bank should not be responsible for floating them money. While in theory this is true, it does not apply to many of the situations that customers complain about. For example; on a day that I have four dollars in my account, I can walk into a Compass Bank at 9:00am and give them a thousand dollars in cash for deposit into my account. At 9:00pm that same day I can make a purchase of $5.00 on my debit card. The next day I will have a $36.00 NSF fee because the $5.00 debit will be removed before the thousand dollar deposit is posted. Was Compass Bank taken advantage of because I made them pay for $1.00 of my purchase? I don't think so; they actually had the money in their bank (earning interest for them) without giving me credit for the deposit on my account. The only reason they charged me the fee is because THEY elected not to post the cash to my account when THEY received it.

I completely agree that this is not an illegal practice. I am only merely pointing out that this practice is NOT the normal practice of the banking industry and that consumers should be aware of this before they choose to do business with Compass Bank. Yes, Yes, Yes, I know the bank gives you a pamphlet with much legal jargon typed in microscopic print that CLEARY (?) outlines their intent to legally borrow your money for one day and charge you as many fees as they can in the process. This brochure does make it legal, but does it make it the right thing to do? We can agree to disagree about that, but my opinion is no. When was the last time you read the entire contract on the back of the form you signed to buy a cell phone, finance a car, or get a mortgage? If you can honestly say you read and understand each and every contractual agreement you enter into on a daily basis than you are the most anal person with way to much time on your hands that I have ever met. Right or wrong, most consumers agree to terms and conditions because they trust the party they are entering the agreement with and know that they would not be able to complete the transactions without agreeing to terms.

If you notice, my post never complained about the bank ripping me off. I did not file the complaint to get back my $36.00. I just want consumers to be aware of this practice so they can make an informed decision. Every bank seems to have complaints filed against them on this website, but Compass Bank clearly has a theme in there complaints. Try to find another bank that has as many complaints about this issue, you can't. While I choose to take my business elsewhere because of this, I am not looking to personally put Compass Bank out of business, but as a consumer it is my right to express my outrage and concern about the way a company does business. Only public pressure and loss of income will make Compass Bank change their ways and this can't and won't be accomplished by a few customers complaining. Convincing a company to change their policies requires a forum such as this to bring attention to the matter.

I understand that you are not going to change your opinion about Compass Bank and you will continue to spend a lot of time educating these poor misguided soles that feel they have been wronged by Compass Bank that it is all their fault (even though you allegedly have no interest in Compass Bank). While I don't have the time or motivation to find any evidence of this, I would warn Compass Bank that this practice of theirs has probably had a greater impact on lower income and minority customers and could very easily become a civil rights issue with a thorough investigation done by the proper authorities. So if you like Compass Bank, God Bless You, use them to your hearts content. I however, will not do business with this company any longer and will let as many people as I can know my opinion. You continue to do the same.

#1 Consumer Comment

There are things you can do.

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Wednesday, May 17, 2006

Compass seems to be unusual in that they process debits first then credits. Most banks do the opposite.

As for largest to smallest debits, most banks process their transaction that way. If you intend to close your account and open one in another bank, be sure to read through the banks terms and conditions before opening an account to determine their method of processing transactions. Don't rely on what the bank personal tell you. You are bound by the actual account terms and condition not what someone verbally tells you unless they are willing to put it in writing and have it signed by upper management.

If you are keeping your account at Compass, I would suggest waiting until the deposit posts to your account before you start drawing on it. That way it doesn't matter what order they process debits in. Check you account terms and conditions since there is a certain wait period for check deposits before you can draw on those funds. EFT, direct deposits, cash deposits, cashiers and government checks are usually available to draw against on the day they post to you account. Again you will need to check your account terms and conditions.

Also keeping a check register helps you to maintain an accurate account balance. Don't rely on ATM or online balance information. It is usually inaccurate.

Unfortuantely, a banking customer can not assume anything regarding their account. If you were to maintain an accurate account register, read through the terms and conditions for your account (you may be surprised at what they are allowed to do) to become familiar with your banks procedures you should be easily able to maintain a free checking account without incurring any fees.

Good luck.

Related Reports

07:47 PM

06:16 PM

08:22 AM

12:27 PM

06:08 PM

09:17 PM

12:07 PM

05:27 PM

07:09 AM

10:56 AM

11:36 PM

04:06 PM

08:17 AM

06:10 PM

01:48 PM

01:42 PM

12:01 PM

07:33 PM

08:57 PM

07:29 PM

06:46 AM

04:10 PM

12:03 PM

11:28 AM

Advertisers above have met our

strict standards for business conduct.