Complaint Review: Compass Bank - Flower Mound Texas

- Author Confirmed

- Compass Bank 2631 Cross Timbers Road Flower Mound, Texas U.S.A.

- Phone: 800-COMPASS

- Web:

- Category: Banks

Compass Bank Illegal processing of debits before credits Dallas Texas

*General Comment: Change banks

*Consumer Comment: Bank rip-offs

*Consumer Comment: Fiduciary Responsibility

*Consumer Comment: Fiduciary Responsibility

*Consumer Comment: Don't banks have a Fiduciary Responsibility to their customers?

*Consumer Comment: Banks use creative accounting to get overdraft fees

*Consumer Comment: Its not illegal....

*Consumer Suggestion: How about trying a Different Bank

*Consumer Comment: Good to know someone still uses sense

*Consumer Comment: My 2 Cents, shop around. There are banks that are more consumer-friendly

*Consumer Suggestion: I thought of something else.

*Author of original report: Superb response

*Consumer Comment: I'm not ranting at you... I just used your name

*Consumer Suggestion: Credit purchases with debit card are not really "offline".

*Consumer Comment: So, after all that...

*Consumer Comment: So, after all that...

*Consumer Comment: So, after all that...

*Consumer Comment: So, after all that...

*Author of original report: One more thing, specific to Ken's rebuttal

*Consumer Comment: You're wrong, Ken

*Consumer Comment: About that law, Kevin..

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

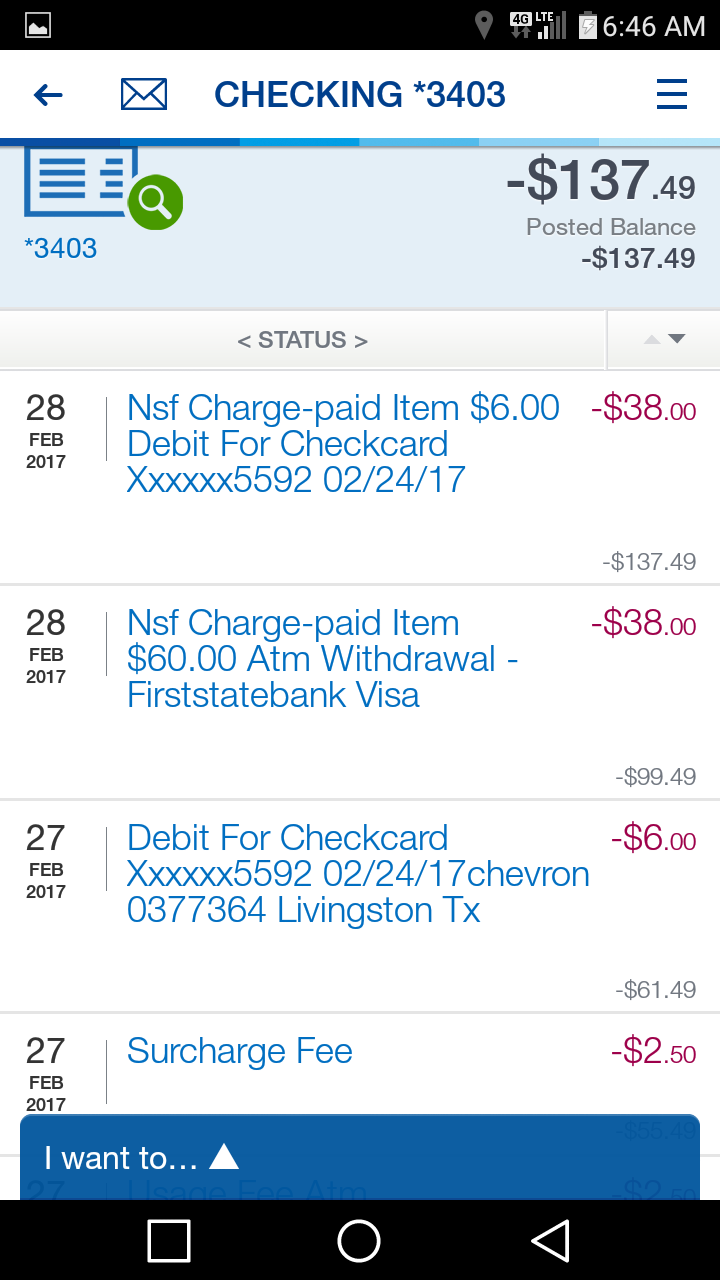

Compass Bank processes transactions based on transaction date and note the date the article is presented to the bank for payment. Specifically, offline (debit card Credit) transactions are sent to the bank at midnight of the next day for payment from the bank. It's just like a check. If you have a direct deposit waiting to post also at midnight, then the bank will still process the debits in the order of the transaction time and not in credit-then-debit order. Compass bank actually refers to these "pre-post" transactions because they quickly learned that they could possibly charge you overdraft fees regardless of any deposits you may be trying to make.

So, deposit your $100 check today with a balance of $5 and it won't post until midnight. After you deposit your money, go to the grocery store and charge (as a Credit transaction) a $10.00 in groceries. Compass Bank will run the transactions such that your grocery transactions posts first and the deposit posts last. Therefore, although your intention was to have $100 to cover your extra $5 in groceries - the bank realizes they can take out the groceries first, charge you $38 for an overdraft and then post your deposit and STEAL your money without you being able to do anything about. You wake up tomorrow thinking you have $90, and you really now only have $52 because the bank screwed you while you slept.

When you call them and ask what happened, they kindly explain that you don't understand what your doing and you should manage your transactions better. They also won't refund the money. And when you ask for a supervisor, they say they will have one call you back. But they never do. And when you call to ask them why they never returned your call, they say they can't find any note of a call in your file. Time and again, the note for a supervisor to call me is never noted in my electronic file (they must you use cheap sticky notes that don't stick very well - but with $38 for an overdraft, you'd think they could afford relatively sticky notes).

So, they manipulate transaction posting to maximize overdraft fees. However it best suits their income needs is the way they'll process it. I thought the law was to post deposits first and then debits when the requested time of posting is equal (midnight).

KEVIN

Flower Mound, Texas

U.S.A.

This report was posted on Ripoff Report on 01/20/2007 06:55 PM and is a permanent record located here: https://www.ripoffreport.com/reports/compass-bank/flower-mound-texas-75028/compass-bank-illegal-processing-of-debits-before-credits-dallas-texas-231712. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#21 General Comment

Change banks

AUTHOR: Kim - (U.S.A.)

SUBMITTED: Friday, July 30, 2010

My advice is stay away from Compass Bank. Personally I feel their banking tactics are unethical. Close your account and run away fast. Compass bank does not care about the customer.

#20 Consumer Comment

Bank rip-offs

AUTHOR: Rushman - (U.S.A.)

SUBMITTED: Friday, December 14, 2007

Learn to manage your money better. It's that simple. Stop writing checks or debits BEFORE your account has been credited. Sometimes this is hard to do. Been there. Just understand, the banks [and not just Compass] will screw you at every opportunity. It's all about the money, not customer satisfaction.

#19 Consumer Comment

Fiduciary Responsibility

AUTHOR: Jim - (U.S.A.)

SUBMITTED: Thursday, December 13, 2007

...extends only as far as maintaining the accuracy of the transactions posting and their validity based on (1) information presented, and (2) policies in place. That responsibility doesn't extend to the order in which the transactions are processed; only that they are processed. That is all any bank customer is owed (and I include all banks in this) as part of their fiduciary responsibility. The bank discloses its policy of posting in its account agreement and it gives them the right to post transactions in any way they wish - even it profits the bank to a greater extent than any other posting method.

The courts generally side with the banks in every case like this, with the exception of cases in which there was inadequate disclosure - those suits were settled long ago and banks corrected the wrongs associated with the claims in the lawsuit. The court even confirmed in the case the bank lost - that the posting order is at the bank's discretion. In doing so, the courts limited the fiduciary responsibility to accuracy ONLY and to end the responsibility there.

The bank also has a duty to its shareholders to maximize profits and return dividends to them. These are whom the bank benefits, not the customer.

#18 Consumer Comment

Fiduciary Responsibility

AUTHOR: Jim - (U.S.A.)

SUBMITTED: Thursday, December 13, 2007

...extends only as far as maintaining the accuracy of the transactions posting and their validity based on (1) information presented, and (2) policies in place. That responsibility doesn't extend to the order in which the transactions are processed; only that they are processed. That is all any bank customer is owed (and I include all banks in this) as part of their fiduciary responsibility. The bank discloses its policy of posting in its account agreement and it gives them the right to post transactions in any way they wish - even it profits the bank to a greater extent than any other posting method.

The courts generally side with the banks in every case like this, with the exception of cases in which there was inadequate disclosure - those suits were settled long ago and banks corrected the wrongs associated with the claims in the lawsuit. The court even confirmed in the case the bank lost - that the posting order is at the bank's discretion. In doing so, the courts limited the fiduciary responsibility to accuracy ONLY and to end the responsibility there.

The bank also has a duty to its shareholders to maximize profits and return dividends to them. These are whom the bank benefits, not the customer.

#17 Consumer Comment

Don't banks have a Fiduciary Responsibility to their customers?

AUTHOR: Bob - (U.S.A.)

SUBMITTED: Thursday, December 13, 2007

I believe all banks have a fiduciary responsibility to their customers. To me the reordering of debits and credit by a bank to benefit them would be putting the banks interest before the customer, and would be a violation of the banks fiduciary responsibility. Just because a bank puts something into a disclosure statement that says they're going to process debits first then fees (if applicable) and finally credits, does that mean they don't have to honor their fiduciary responsibility? I would hope not. It would seem to me that regardless of what they say in any disclosure statement, if that statement is in violation of the law it can (and should) be challenged.

#16 Consumer Comment

Banks use creative accounting to get overdraft fees

AUTHOR: Phil - (U.S.A.)

SUBMITTED: Wednesday, December 12, 2007

Banks use creative accounting methods to help put accounts into the red, so they can get the maximum number of overdrafts fees that they can. The reorganization and order of how the debits and credits are applied to accounts is just one of their magic accounting techniques.

These practices should be illegal and changed. But, the way it stands right now, "the Banks steal, and our Congress is driving the getaway car."

#15 Consumer Comment

Its not illegal....

AUTHOR: Tony - (U.S.A.)

SUBMITTED: Friday, June 29, 2007

The government has no law on how any bank processes their transactions, the bank make them and state it in their policies that are disclosed to you when you open an account, read your brochures.

#14 Consumer Suggestion

How about trying a Different Bank

AUTHOR: Noel - (U.S.A.)

SUBMITTED: Friday, April 13, 2007

I had a similar experience with Compass Bank in Phoenix,AZ. But the they only got away with it once. I moved to Desert Schools Credit Union and I couldn't be happier. They even refunded my NSF charges the one time I made a mistake because they could see that I had accidentally transfered the funds from the wrong account. So not all Banks are crooks, and if enough people switch maybe Compass will change their tune.

#13 Consumer Comment

Good to know someone still uses sense

AUTHOR: Kevin - (U.S.A.)

SUBMITTED: Tuesday, January 23, 2007

Thanks Chip. I'm glad to know some banks still operate old-fashioned-ly. My dad's bank ALWAYS ran credits before debits... for the simple fact of helping out the customer. I mistakenly thought all banks operated that way. But then again, that was a podunk private bank in a podunk town.

You get in a metropolis like Dallas, and there's not too many podunk banks with common sense left. But thanks Chip, for letting me know there's still at least some. If I can find one, I'll use it... if they'll have me now. Any chance the bank you use has a branch in the Dallas/Fort Worth area?

But it won't be long before they lose their brains. If you saw every guy on your block getting away with rape - would you go rape someone? Of course not. But a bank would.

In fact, the class action lawsuit against Bank of America is a great example. Bank of America settled our of court without any admission of fault - because they didn't want a ruling to come out that would effect the entire industry (they didn't want their buddies to get caught too). Instead, the idiots in that class action suit took a payoff and went away quietly. Had they stuck to their guns, they could have taken a step to change an industry.

#12 Consumer Comment

My 2 Cents, shop around. There are banks that are more consumer-friendly

AUTHOR: Chip - (U.S.A.)

SUBMITTED: Monday, January 22, 2007

There IS such a thing as "offline" transactions. I know this because my old credit union had this practice. If I used my debit card as a credit card, the transaction did not post until they received the batch. Even if I swiped the card, there was no "hold" or "pending" transaction. That said, it didn't matter because the minute I swiped the card, I deducted the transaction from the balance in my register. My current bank does not operate this way. Every time I use my debit card, there is a hold on that amount until midnight. The hold is then released and the amount is not deducted from my balance until the transaction posts, usually 48 hours after I used the card. Again, this does not matter. The minute I use the card, I deduct that from my balance.

Also, I think banks have different policies regarding the posting of debits and credits. My bank posts credits BEFORE debits. Say, for example, I have a scheduled online payment for my mortgage. Those are deducted first thing in the morning -- around 8 am. There was one instance where I made a mistake, and my account was actually negative a couple hundred dollars after an online payment was processed. I went into the bank that same day and deposited a check to cover that. I avoided an NSF fee much to my surprise because that night, the bank posted the CREDITS before the DEBITS, even though the debit transaction occurred before the credit transaction.

So shop around. There are banks that are more consumer-friendly, as much as an oxymoron as that sounds. And I doubt Compass is doing anything illegal. The posting of the highest to lowest transaction -- I do think that's a universal bank practice these days to, as we all know, increase profits. But you can avoid that simply by using a register. Banks only get as many NSFs out of you as you allow them to.

#11 Consumer Suggestion

I thought of something else.

AUTHOR: Nikki - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

Some banks do this practice, but not all. Hope this helps some people reading this.

Say you have $150 in the bank and a $120 check, a $30 check, and a $20 check get posted. The bank adds together all the checks ($170) and puts your account at negative $20 for the days work. The next day your account will show the $150 added back in (because they returned the checks), then subtract 3 NSF fees. They bounce all three checks because you didn't have enough money to cover the entire day's batch of checks.

They back it up by saying, "If we pay the $120 check and the $30 check, you don't have enough money left for the NSF fee on the $20 check. So we then have to bounce the $30 check to make sure we can recover the NSF fee for the $20 check. However, now we have to bounce the $120 check to make sure we can cover the NSF fees for the $30 check and the $20 check". That's why they bounce all three.

#10 Author of original report

Superb response

AUTHOR: Kevin - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

That was a perfect explanation Nikki. I appreciate that. I sort of already knew it, but you spelled it out nicely. And I'm glad that you don't agree with their practices. And if you hadn't noticed, you're not the only other "long winded" one around here. I can type about 100 words a minute. so it's more like the thoughts stream into the computer, and away I go. huh, Ken. ha ha. By the way, I'm hungry and I hate the bank. Now I've gotta go steal a pack of turkey tomorrow.

#9 Consumer Comment

I'm not ranting at you... I just used your name

AUTHOR: Kevin - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

I have a problem with it when it results in leaving a person without a penny to feed his family with. I strongly disagree with that. In the case of a direct deposit and offline transactions, a $100 deposit, $25 in debits, equals -$150 and counting. You can take all the disclosures, terms and conditions and throw them straight out the window. Show some common sense.

If the fees result in leaving a count negative, when otherwise the customer would have had money to cover his debits then put the fees into another account and settle up with their next direct deposit but give the consumer time to prepare. don't leave them stranded, broke and begging because you had to take your fees right then and there.

#8 Consumer Suggestion

Credit purchases with debit card are not really "offline".

AUTHOR: Nikki - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

Credit purchases made with a debit card are not really "offline" transactions. They are done in real time which is why there is a hold against your balance, hence the available balance. In addition, checks cashed against your account at the teller window are done in real time, as well as the Check21 systems now being used. The only real "offline" transactions are deposits and checks to be posted.

If you make a deposit before 2:00, and know the money will be credited today, that really means late today. You cannot go out and spend the money 1 hr after you make the deposit, because 1hr (or 5 min, or 2 hrs, etc.) later, the money is not really in your account yet. It is posted as a deposit after the bank is closed. Then checks are posted in order of amounts.

However, with credit purchases on the debit card, they are technically "guaranteed" by the bank earlier in the day. Since the bank has guaranteed the funds by holding them against your balance, they are posted before your deposit. If you make a deposit at 1:00 pm, the bank has not guaranteed that your deposit is posted at 1:00 pm (unless you bank at an instition that posts it immediately). It guaranteed the deposit will be posted sometime today. If you make a credit purchase at 1:30 pm, the bank has guaranteed that charge to the merchant at 1:30 pm. Even though the merchant has not run their batch, the bank has still guaranteed the money. Therefore, the bank considers the credit purchase placed before the deposit and that's how they charge the fees. I don't agree with this in any way, that's just what they do to rack up the fees and it does stink. When I make a deposit, they have my money so I should be able to use it.

In addition, say I have $50 in the bank and I make a $10,000 cash deposit. Then the person behind me in line tries to cash a check in the amount of $200. The bank does not have to cash it because technically the check is being presented against an account with only $50 in it (some banks will override it because the deposit was made so close to the cashing of the check and they remember it). My $10,000 deposit is not posted until later. I have made cash deposits before, then later realized I needed some of the money for something.

When I went back to the bank to get some of that deposit out again, I was unable to because my deposit had not posted yet, even though they had my money. Same thing with credit purchases. If your bank has not posted your deposit, even though you already made the deposit, you cannot purchase against that money until that deposit posts.

Also, say it is Thursday and I have a direct deposit going through at midnight because I am paid on Friday. This does not mean any checks or charges that come through on Thursday at midnight are covered. The checks and charges that come through at midnight are posted with Thursday's date, and my direct deposit is posted with Friday's date.

Sorry, I tend to get a little "long winded".

#7 Consumer Comment

So, after all that...

AUTHOR: Ken - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

Where was I wrong? I never said that it was right or wrong, all I (correcty) said is that it is within the bank's right to process in the order they choose. By law, they have to disclose it when you open the account... but then again who can be bothered to read the documents you get when you open an account.

I recently asked ny bank for a copy of their disclosure, just to see what happened. The kind lady had a stack of them on her desk. In the disclose it states the following:

"Items are processed nightly in the following order: Debit items will be processed before credit items. Debit items are processed in the following order: unnumbered items (electronic transactions and counter checks) are processed first, then checks, in check number order."

Not as bad as some, not as good as my credit union, but the point is that I know in advance what's going to happen when I play the float.

You also have you 'batches' mixed up. All financial institutions operate in one of two modes: real-time, or batch. As a rule, savings banks and credit unions tend to run real-time, while commercial banks use batch. In my original post I made reference to transactions at a teller window. You brought electronic transactions into the conversation, but they were never at issue. The term 'batch' used here refers to a operating mode, not an item.

I have no real beef about the processing order, but I do think that legislation is needed to limit the number and amount of overdraft fees which can be incurred in a single day. Beyond that, I think banks should be required to close checking accounts as soon as a certain number of overdrafts have been reached. This would force them to try and work with the customer and help them manage their account. Failing that, it would limit losses by forcing the folks who just shouldn't have that type of account to use another method. For instance, a savings account and free money orders.

#6 Consumer Comment

So, after all that...

AUTHOR: Ken - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

Where was I wrong? I never said that it was right or wrong, all I (correcty) said is that it is within the bank's right to process in the order they choose. By law, they have to disclose it when you open the account... but then again who can be bothered to read the documents you get when you open an account.

I recently asked ny bank for a copy of their disclosure, just to see what happened. The kind lady had a stack of them on her desk. In the disclose it states the following:

"Items are processed nightly in the following order: Debit items will be processed before credit items. Debit items are processed in the following order: unnumbered items (electronic transactions and counter checks) are processed first, then checks, in check number order."

Not as bad as some, not as good as my credit union, but the point is that I know in advance what's going to happen when I play the float.

You also have you 'batches' mixed up. All financial institutions operate in one of two modes: real-time, or batch. As a rule, savings banks and credit unions tend to run real-time, while commercial banks use batch. In my original post I made reference to transactions at a teller window. You brought electronic transactions into the conversation, but they were never at issue. The term 'batch' used here refers to a operating mode, not an item.

I have no real beef about the processing order, but I do think that legislation is needed to limit the number and amount of overdraft fees which can be incurred in a single day. Beyond that, I think banks should be required to close checking accounts as soon as a certain number of overdrafts have been reached. This would force them to try and work with the customer and help them manage their account. Failing that, it would limit losses by forcing the folks who just shouldn't have that type of account to use another method. For instance, a savings account and free money orders.

#5 Consumer Comment

So, after all that...

AUTHOR: Ken - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

Where was I wrong? I never said that it was right or wrong, all I (correcty) said is that it is within the bank's right to process in the order they choose. By law, they have to disclose it when you open the account... but then again who can be bothered to read the documents you get when you open an account.

I recently asked ny bank for a copy of their disclosure, just to see what happened. The kind lady had a stack of them on her desk. In the disclose it states the following:

"Items are processed nightly in the following order: Debit items will be processed before credit items. Debit items are processed in the following order: unnumbered items (electronic transactions and counter checks) are processed first, then checks, in check number order."

Not as bad as some, not as good as my credit union, but the point is that I know in advance what's going to happen when I play the float.

You also have you 'batches' mixed up. All financial institutions operate in one of two modes: real-time, or batch. As a rule, savings banks and credit unions tend to run real-time, while commercial banks use batch. In my original post I made reference to transactions at a teller window. You brought electronic transactions into the conversation, but they were never at issue. The term 'batch' used here refers to a operating mode, not an item.

I have no real beef about the processing order, but I do think that legislation is needed to limit the number and amount of overdraft fees which can be incurred in a single day. Beyond that, I think banks should be required to close checking accounts as soon as a certain number of overdrafts have been reached. This would force them to try and work with the customer and help them manage their account. Failing that, it would limit losses by forcing the folks who just shouldn't have that type of account to use another method. For instance, a savings account and free money orders.

#4 Consumer Comment

So, after all that...

AUTHOR: Ken - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

Where was I wrong? I never said that it was right or wrong, all I (correcty) said is that it is within the bank's right to process in the order they choose. By law, they have to disclose it when you open the account... but then again who can be bothered to read the documents you get when you open an account.

I recently asked ny bank for a copy of their disclosure, just to see what happened. The kind lady had a stack of them on her desk. In the disclose it states the following:

"Items are processed nightly in the following order: Debit items will be processed before credit items. Debit items are processed in the following order: unnumbered items (electronic transactions and counter checks) are processed first, then checks, in check number order."

Not as bad as some, not as good as my credit union, but the point is that I know in advance what's going to happen when I play the float.

You also have you 'batches' mixed up. All financial institutions operate in one of two modes: real-time, or batch. As a rule, savings banks and credit unions tend to run real-time, while commercial banks use batch. In my original post I made reference to transactions at a teller window. You brought electronic transactions into the conversation, but they were never at issue. The term 'batch' used here refers to a operating mode, not an item.

I have no real beef about the processing order, but I do think that legislation is needed to limit the number and amount of overdraft fees which can be incurred in a single day. Beyond that, I think banks should be required to close checking accounts as soon as a certain number of overdrafts have been reached. This would force them to try and work with the customer and help them manage their account. Failing that, it would limit losses by forcing the folks who just shouldn't have that type of account to use another method. For instance, a savings account and free money orders.

#3 Author of original report

One more thing, specific to Ken's rebuttal

AUTHOR: Kevin - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

Specifically, Ken - there ARE "offline" transactions that DO NOT occur at the Bank's teller window. These transactions are sent to the bank in batches. For some transactions, such as Credit purchases on a debit card and for check's you write, they are processed in batches. And yes, most banks are capable of making a teller's windows workstation an "online" transaction center... good for them. But that has nothing to do with batched, offline transactions and the way those transactions are posted.

I went on a little rant in my last rebuttal because I cannot believe how many humans are willing to be so inhumane. What is this syndrome in America where people want to believe Corporations are always right, not the people. So many employees of collection agencies, credit card companies and banks are willing to be so inhumane as long as they don't lose their own job. Let them get laid off and become one us poor Joe's... and their tune will change. People are willing to throw their common sense out the window as long as they're getting paid... "Look lady, I don't care that you can't feed your child. You couldn't manage your checkbook so we took whatever money you had left. Go beg or something, but leave me alone... I'm just doing my job! Plus, my wife's waiting for me in Tampa."

HELLO! Companies are ran by humans for humans, yet they (the humans) all act like preprogrammed robots. It's a shame and quite disgusting to me.

Let's say you had a heart attack because you accidently forgot to bring your blood pressure medicine with you on a business trip. When you get to the hospital, they refuse to treat you because you failed to take your blood pressure medicine. "It's your own fault, sir. You should have taken your medicine as we outlined in our Terms and Conditions document that even I don't understand." It's absurd. That hospital wants that person to leave their facility in as good condition as they possibly can... so that they can come back again in the future. They know it's inevitible that you'll be back... they're gonna get paid... why kill you now. Banks and hospitals aren't so different, because people CANNOT remain healthy without money.

Banks, credit card companies and collection agencies throw all their common sense out of the window for the all mighty dollar. They act like if they don't take your money NOW, they'll never get it. Are you kidding me? This society FORCES banking on you - you have no choice... direct deposit requirements, debit cards, pay-by-phone, etc... Let the banks be a little more creative and know that if they don't get your money NOW, they'll get it later in another form. If you leave that person with a little money to buy food, then they'll remember that and they'll be back. The banking industry is foolish... they're like crack dealers. They don't care about you and your family... they would just as soon use your body as a stepping stone on the way to their beach front house.

I'm not saying there aren't criminals. There are criminals with malicious intent who purposely open credit accounts without the slightest intention of paying it back. There's identity theives and many immoral souls floating about. But I believe that the majority of the pople that the banks are screwing over are people with good intentions... people that never intended the bank any harm. I believe most of us are glad that banks are profitible, give good jobs to people and donate lots of cash to charities. I don't want my actions to "bring the bank down". Accidents happen, yet the bank will leave you swinging in the gallows as long as they walk away with the cash in their pocket. It's a shame and this great country should be ashamed that it condones it.

My father was a bank president. When I was a child, we received many death threats against our entire family because my dad had foreclosed on someones home, or denied a loan that could have saved their business. And naturally, I thought they were all dead beats that couldn't add. I was wrong - and many times my dad was wrong too. I believe he went to his grave with regret because he had taken so many people down. At the time, he was doing his job... for the people paying his salary. When he died, he was just another person that had passed out just as many heartaches as the criminals he despised. It's a shame - he lost sight of what was important, he told me so. How many other people are doing the same thing? Grow a heart - don't kick people when they're down... help pick them up so they can come back. It's simply counter-intuitive to the long term success of the human race.

#2 Consumer Comment

You're wrong, Ken

AUTHOR: Kevin - (U.S.A.)

SUBMITTED: Sunday, January 21, 2007

Ken, I've learned how they do business by being repeatedly raped by them, not because any disclosure put it in a form that is understandable by a normal person or can even be found by a normal person. I can go to one branch and get on explanation and go to another branch and get a totally different explanation. The employees aren't even sure how it works. The employees are trained to think the Bank IS ALWAYS RIGHT... how could the bank not be right? It's THE BANK after all... large corporation with lots of attorneys that are looking out for the consumers best interest, right Ken? No, those lawyers are looking for loopholes in the regulations and laws so that they can maximize how much the bank can steal from consumers "according to their interpretation of the law". The Bank's lawyers are paid (and given bonuses based on their ability) to find ways to screw the consumer... it's plain and simple, and anyone is a fool to believe otherwise. Attorney Joe knows that if he can expose this law such that the bank can now generate an extra 1.5 million in overdraft fees, then Joe figues he's got a good chance of making VP next year.

There are regulations which mandate when deposits must be posted to an account. Banks cannot process deposits in ANY manner they wish. They can order a batch of debits in any way they wish (largest check first scam). But if a deposit is marked for posting at midnight and a debit is marked for posting (or payment) at midnight... at effectively the same time... then you want to tell me that the bank can do whatever they please. So obviously, the bank arranges processing such that any possible overdraft will be bled out of those transactions.

So Ken - tell me. Could the banks not find equally impressive ways to help their consumers rather than rape them? Wouldn't it make sense to a make it consumer friendly rather than step on the throats of the people who are financially strapped? Where's the ethics? Where's the humane treatment of people? It takes money to buy groceries and feed yourself, not to mention paying for a roof over your house and heat so you don't freeze. But a bank has no problem taking someone's last $100 to feed its overdraft habit, rather than worrying about whether those people can eat. Hell, it's the consumer's fault, right Ken? We're the idiots that can't balance a checkbook, yet you tell me the percentae of accounts at any one bank that HAS NOT had an overdraft posted to their account. Accidents happen - and sometimes they happen more than once. You find me someone with an overdraft and that person is simply lucky - that's all. It's not because they balanced their check book 7 times a day and stayed on top of their finances. It's because an accident didn't happen. But when an accident does happen, the bank wants to take 45 days to make a judgment and correct the mistake. How do I eat during those 45 days, Ken?

If the banks can spend millions to screw customers over, which is what they do. Then why can't they spend millions to make the most consumer friendly model they can make? If you come to me with a deposit, and I'm holding 5 checks written to your account - I can quickly see that if I were to deposit your money FIRST, then those 5 checks will have no problem clearing. I'm holding them all right then - the checks aren't posted yet... I do that. The deposit isn't posted yet, I do that too. So it's completely up to me how I process them. You find me any human that will look the other human in the eye and say, "Sir, I'm sorry - I see that your deposit will cover the money to paid by these checks, but I'm simply not going to process it that way. I'm going to run the checks first so that we generate overdraft fees on the last 3. AND THEN, I'll post your deposit so that it can pay for all the fees we just charged you." The bank wouldn't have employees if that were the case - nobody is going to screw a person that's standing in front of them in that way.

And hence, our problem Ken. Bank's have removed the human dimension out of it. They've made it as cold and calculating as possible so that they can maximize their profit and all their executives can get the biggest bonuses possible and can retire with a beach front home in Tampa. Are the banks not clever enough to create income without being inhumane? Are they incapable of finding good investments for the money they already have, or is it really necessary to get that extra $1.5 million on a bottom line that reaches will over $1 BILLION dollars? When's enough money enough, Ken? These overdraft fees are feeding on the people in the most precarious and unstable financial situations in our economy. Does it really make sense for the bank to effectively drive them into financial ruin? It seems to contrary to me. The bank would be best served by making sure all their customers are as well off as they can be, so that they'll be happy customers with money for years to come. But no - the bank wants to manipulate the regulations and interpret the laws in such a way that they break anyone on the edge. Let's not give them a hand Ken... You step on their throats while I dig their grave... sounds like a plan, right?

#1 Consumer Comment

About that law, Kevin..

AUTHOR: Ken - (U.S.A.)

SUBMITTED: Saturday, January 20, 2007

You'd be wrong. The bank can process items in any manner they choose, as long as they disclose the way they handle them. Since you seem to be aware of how they process items, it seems to have been disclosed to you.

If you look around, you can find banks or credit unions that do not process in batch. In these places, your transaction is completed while you are at the teller window.

Related Reports

07:47 PM

06:16 PM

08:22 AM

12:27 PM

06:08 PM

09:17 PM

12:07 PM

05:27 PM

07:09 AM

10:56 AM

11:36 PM

04:06 PM

08:17 AM

06:10 PM

01:48 PM

01:42 PM

12:01 PM

07:33 PM

08:57 PM

07:29 PM

06:46 AM

04:10 PM

12:03 PM

11:28 AM

Advertisers above have met our

strict standards for business conduct.