Complaint Review: Compass Bank - Gilbert Arizona

- Author Confirmed

- Compass Bank 77 S. Val Vista Dr. Gilbert, Arizona U.S.A.

- Phone: 800-822-5127

- Web:

- Category: Banks

Compass Bank Compass Bank process largest debit first regardless of what order the debits come in causing more NSF on thier customers. Gilbert Arizona

* : No Laws Broken Here

*Author of original report: In Response to Ken

*Consumer Comment: What are you going to report?

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

Compass Banks policy is to process the largest debit first, so if you have $200 in bank and you have 3 debits or checks out one for $4.00 one for $7.00 and one for $201, guess which one they process first? Thats right they process the $201 one first causing all three to bounce and then they charge you $38.00 for each one. Even if you can prove with debit slips that the lower amount purchases were made before the larger amounts, they still won't change there policy. Kind of sucks being $12.00 short and then get stuck with $114 worth of NSF fees.

This has got to change, many other banks do it this way as well. So beware before you write a check or use your debit card.

And if this has happened to you REPORT THE BANK TO THE Better Business Bureau maybe if they get enough complaints against them they will change there policies.

Joe

Gilbert, Arizona

U.S.A.

This report was posted on Ripoff Report on 09/03/2008 03:26 PM and is a permanent record located here: https://www.ripoffreport.com/reports/compass-bank/gilbert-arizona-85296/compass-bank-compass-bank-process-largest-debit-first-regardless-of-what-order-the-debits-369459. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#3

No Laws Broken Here

AUTHOR: ken - (USA)

SUBMITTED: Thursday, September 17, 2009

As the original responder sated, You have still not proven any law being broken here. I may also add that you need not fire back some over the top attitude laden response to the people that reply to your reports. All you are doing is painting a picture of yourself as some over the edge, screaming at the teller, and can't be helped nutcase. Your first problem in a court case here, would be proving wrong. Your second problem in a court case here, would be proving you are not just an unbalance loon. And yeah, they can subpoena the forum postings, and most people on a jury would read into your writings as the rantings of someone who will just be an arse to anyone when he doesn't get his way.

#2 Author of original report

In Response to Ken

AUTHOR: Hotforstangs - (U.S.A.)

SUBMITTED: Tuesday, September 09, 2008

"What are you going to report?

The bank isn't doing anything wrong. They are processing items in the order they told you they would when you opened the account. The order of items shouldn't matter anyway if you have the funds in the account to cover them. If you don't, it is YOU that just broke the law by negotiating a bad check.

This just underscores the fact that not keeping a register and balancing your account, is very expensive."

"They are processing items in the order they told you they would when you opened the account."

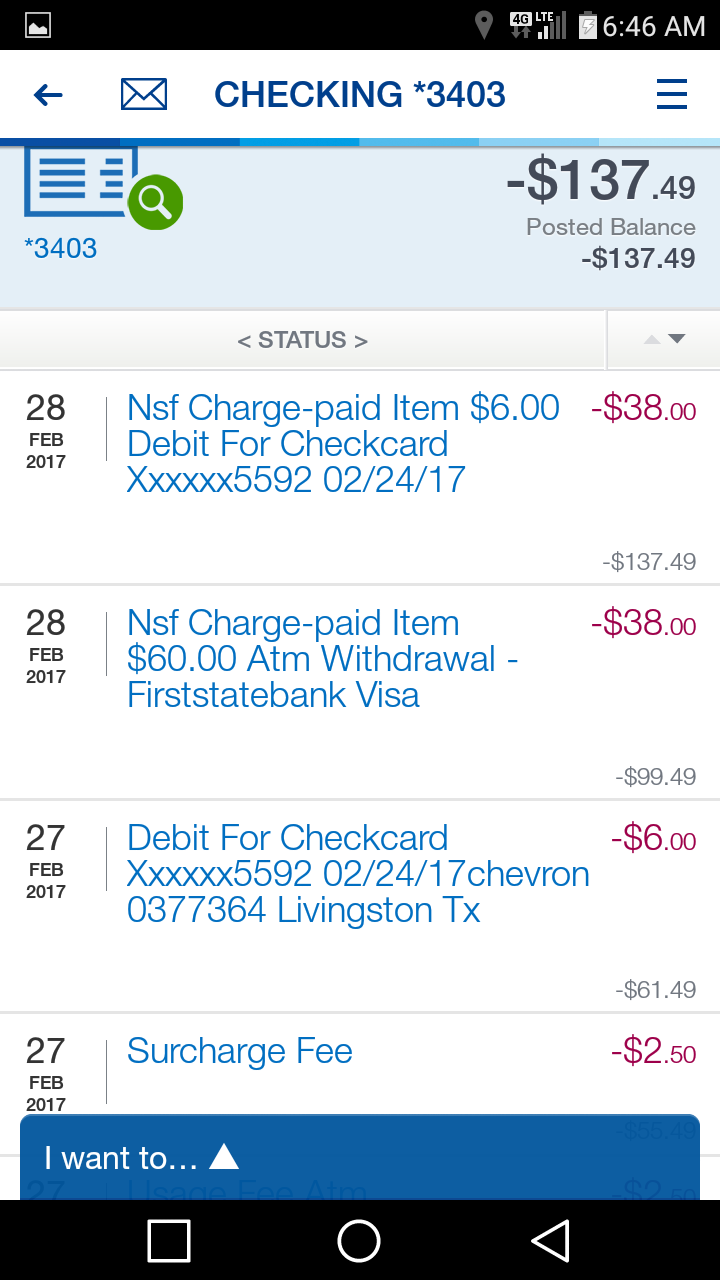

Why thanks for pointing out the fact if you have the funds in the account to cover the items it wouldn't matter anyway. Well no s**t Sherlock. I was completely unaware of this. Again I thank you for pointing this out. And the fact of the matter is, if you really must know, I didn't have a problem with keeping a properly balanced check book, what screwed me was a check I deposited that had been returned for insufficient funds, which caused my register balance to be off. Oh and get this it took them 14 days to figure out that the check was no good. So I get to eat $114 dollars because of this??

"They are processing items in the order they told you they would when you opened the account."

I didn't see anything in their most recent account disclosure about the way they process debits nor could I find anything in the terms and agreement things they send with your account statements. You wanna know the excuse the bank gives the consumers as to how they process the debits?? "We process the debits that are most important first." That's what the customer service tells you. How in the hell are they supposed to know what is more important? And besides the point, I never initially opened a Compass Bank account, The first bank account I opened was with Arizona Bank which became Norwest Bank, which then became Compass Bank. So I just kinda got stuck with this bank. And with Arizona Bank and Norwest Bank they did not use this practice, they processed debits, credits as they were received. I also have a checking account with a credit union, and guess what? They don't process the way Compass Bank does either. So I guess your statement is wrong cause they never told me or sent me anything stating as to how they would process the debits, I assumed it would be the same as the previous banks for which they took over.

So Ken are you gonna tell me next that I shouldn't spend money just in case one of the checks that was written to me may bounce? So I have to wait 14 days just to be sure it doesn't?

And you wanna know another thing Ken, they also process debits before deposits, which can also have some unsuspecting consumer to receive NSF charges.

I know Ken, they should have gotten to the bank and made the deposit the day before so that wouldn't happen. Not saying I had this problem but kinda would suck if the consumer got flat tire or got stuck in traffic due to an accident etc... which caused there deposit occur the following business day. What suck about this is you could make a cash deposit at 3:00 pm, make a debit card purchase at 9:00pm on same day and guess what will happen first? Ding ding ding yep you got it process the debit first. No tell me Ken should that be legal?

Below is Compass Banks Account Disclosure, where in there does it say how they process debits?

Build-to-Order Checking

Account Disclosure - Arizona

PLEASE RETAIN A COPY OF THIS DISCLOSURE FOR FUTURE REFERENCE.

Standard Benefits/Requirements

* Requires $25 minimum deposit to open.

* Checks posted to the account are not returned in the monthly statement, but photocopies are available. Charges for photocopies are $3.00 per posted item.

* An image statement is available for a service charge of $3.00 per month. An image statement includes reduced pictures of cancelled checks in numerical order. The paper copies of cancelled checks will not be returned in the statement for this account.

* Free safekeeping of checks.

Definitions

* Account Anniversary: The Account Anniversary is the month and day you opened your Build-to-Order Checking account or convert to a Build-to-Order Checking account.

* Feature Year: This is a period of twelve statement cycles between Account Anniversaries, beginning with the statement cycle in which the Account Anniversary falls. Certain Premium Features may be tied to the Feature Year. Please see the description of Premium Features below.

* Premium Features: These are the additional features you can select to customize your Build-to-Order Checking account, and they are listed below.

Premium Features: Select 2 Premium Features at no charge. (See charges for additional features below).

* No fee for using another bank's ATM

* Rebate of ATM fees that other banks charge

In order to receive rebate, ATM receipts showing ATM fees or account statements showing ISF fees must be mailed within 90 calendar days of the ATM transaction to Compass Bank . Rebate will be directly deposited into the checking account within 10 business days of receipt. Compass does not rebate International Service Fees for Point of Sale transactions (for example, purchases from a foreign merchant using your Check Card).

* Interest on your checking balances

If you select this feature, the following terms apply:

The daily balance method is used to calculate the interest on your account. This method applies a daily periodic rate to the daily collected balance in the account each day. Interest on deposits begins to accrue no later than the business day on which we receive credit for the deposit. Accrued interest is credited to the balance in the account on the last day of the statement cycle. Accrued interest that is credited to the balance in the account begins to earn interest no later than the next business day and compounds with each statement cycle. Statement cycles are generally monthly, unless otherwise disclosed. If you close your account or convert your account to a non-interest earning account before accrued interest, if any, is credited, you will not receive the accrued interest. A taxpayer identification number will be required to earn interest on these accounts.

* Cash Bonus on your account anniversary (up to $25)

o This bonus must be selected for twelve consecutive statement cycles and the account must be active each of those twelve consecutive statement cycles to receive the full $25 bonus. A portion of this bonus (approximately $2.08) is accrued for each statement cycle in which the feature is selected and your account is active. An "active" statement cycle for purposes of this bonus is a statement cycle in which there is at least 1 customer-initiated deposit or withdrawal during the statement cycle. If there is no deposit or withdrawal during the first statement cycle, which can be less than 30 days, the bonus will not be accrued for that first statement cycle.

o Build-to-Order Checking Account must be open on the Account Anniversary for this feature to be paid. If the Build-to-Order Checking Account is closed before the Account Anniversary, the cash bonus accrued to that point will not be paid.

o Bonus will be paid on the Account Anniversary. (If the Anniversary Date falls on a holiday, weekend or non-processing day, the bonus will be paid the next processing day.) Bonus is paid only from time of the most recent selection of the bonus feature, meaning the pro-rated feature will be paid only for the period in which the feature is selected consecutively up to the Account Anniversary. If the cash bonus feature is selected at account opening and subsequently de-selected prior to the Account Anniversary the cash bonus accrued prior to the de-selection of the feature will not be paid. Cash bonus will be directly deposited into the Build-to-Order Checking Account. Bonus may be subject to IRS tax reporting.

o Limit 2 bonus features per customer.

* Double Visa Extras points

Visa Extras program enrollment required. Standard Visa Extras points will be earned. On the month following your Visa Extras account update, Compass will match those points earned in the previous month, thereby giving double the rewards. Points are paid only on Qualifying Purchases. A "Qualifying Purchase" is any signature-based purchase, Internet purchase, phone or mail-order purchase, bill payment, contactless purchase (purchases made by holding your Visa card or other device up to a secure reader instead of swiping your card), or small dollar purchase for which you are not required to sign, made with an enrolled Visa card, that is processed or submitted through the Visa U.S.A. Inc. payment system. A Qualifying Purchase does not include a purchase made using a Personal Identification Number (PIN) or purchase you initiate through identification technology that substitutes for a PIN. Additional restrictions apply. For more information on qualifying purchases, see program terms and conditions.

* Cash Back on Visa Check Card transactions

o Available for the primary Check Card for the account only. Earn cash back on Qualifying Check Card Purchases* routed through Visa. (*See "Double Points on Visa Extras" for Qualifying Purchase definition.)

o $0.05 will be earned for every signature-based purchase (excluding teller cash disbursements and merchant authorizations that are not completed.).

o In addition, $0.05 will be earned for every two PIN-based purchases (excluding cash transactions, ATM transactions, quasi-cash transactions, payments made for pre-paid or re-loadable cards such as certain gift cards, Visa Buxx and similar cards, transactions conducted at Global Access Cash Terminals and pre-authorizations for transactions).

o Returns or debits of a Visa Check Card charge will be deducted from the cash calculation.

o Cash back rewards will be credited at the end of the statement cycle for the Build-to-Order Checking Account linked to the primary check card. The posting date for a qualifying transaction will determine the date of the transaction for purposes of this feature. Credits for the net purchase activity will be made at the end of the cycle period. If the Build-to-Order Checking Account is closed, the cash back rewards accrued in the current statement cycle will not be paid.

* One Overdraft Fee (NSF Charge) Forgiveness per year

Applies to one NSF Charge-Paid Item or one NSF Charge-Returned Item (see "Miscellaneous Fees"). The Overdraft Fee (NSF Charge) Forgiveness Feature must be redeemed during your anniversary year in which this feature is selected or it will be forfeited; this feature does not accrue or carry forward into subsequent years. Once you redeem this feature it will remain a selected feature until the Account Anniversary. You may cancel this feature after the Account Anniversary before you redeem it in the next Anniversary Year. If you select other features during the year, and have redeemed the Fee Forgiveness feature, they will be in addition to this feature. This feature may not be used for forgiveness of Extended Overdraft Service Charges.

The following chart shows the annual percentage yield and interest rate effective as of July 2008. At our discretion, we may change the interest rate for your account at any time. To obtain current rate information, contact us at 1-800-COMPASS.

Build-to-Order Checking

Daily

Collected Balance Interest

Rate Annual

Percentage

Yield

$75,000 and above 1.490% 1.50%

$25,000 - $74,999 1.243% 1.25%

$10,000 - $24,999 0.747% 0.75%

$2,000 - $9,999 0.499% 0.50%

$0 - $1,999 0.200% 0.20%

AS REQUIRED BY FEDERAL LAW, COMPASS RESERVES THE RIGHT TO REQUIRE AT LEAST SEVEN (7) DAYS NOTICE PRIOR TO WITHDRAWAL OR TRANSFER OF FUNDS FROM ANY INTEREST EARNING ACCOUNT

* Pricing:

o Two features provided free of charge.

o Additional features may be selected for an "Add-On Benefit Charge" of $2.00 each. ("Add-On Benefit Charge" will be the description on your monthly account statement.) For example, if five features are chosen, the account will be charged an "Add-On Benefit Charge" of $ 6 per month.

o The "Add-On Benefit Charge" will reflect the highest number of features selected during the given statement cycle, regardless of the number of days the features were in effect. The "Add-On Benefit Charge" will be incurred on the day the statement is generated.

o The features selected at 8:00 pm/CST at the end of a banking day will be the features given for that day. (Example: If double points are selected at 10:00 am, card is used during the day, and double points is changed to Interest in the evening of the same day, double points will NOT be awarded; rather the account will have Interest as the feature.)

o Note: Features are calculated based on statement cycle, not month.

Miscellaneous Fees and Charges

OTHER SERVICE CHARGES APPLICABLE TO ALL CONSUMER ACCOUNTS

Account Closed within 180 Days of opening $25.00

ATM/Check Card Replacement Fee

(applies to non-personalized Compass ATM/Check Cards) $5.00

Check Charges Personalized check orders are debited from your account when your order is received. Personalized check order charges vary by style, check design chosen by customer, and number of checks ordered.

Collection Items

* Incoming - $20.00

* Outgoing - $20.00

* International - $20.00 + costs

Compass Fee for Using Another Bank's ATM $2.00/transaction

Deposit Correction Fee $2.50/item

Deposits to Closed Accounts $25.00/deposit

Dormant Accounts $5.00/month

Extended Overdraft Service Charge $42.00

Should your account become overdrawn and continue with a negative balance for six (6) consecutive calendar days, an extended overdraft fee of $42 will be charged. Thereafter, if your account continues to maintain a negative balance, a fee of $7 per calendar day will be assessed beginning on the seventh (7th) calendar day and will continue until day thirty (30) of overdraft status or until the account is brought to a positive balance, whichever occurs first. This extended overdraft fee is in addition to any NSF fees you may incur as a result of items being presented against insufficient funds.

Garnishments, Levies, Court Orders $75.00 plus attorney fees

Inactive Account Charges Inactive accounts are service charged in accordance with the normal charges for the type of account

Inter-Account Transfer Fee $10.00/transfer - Transfers funds from customer designated account to cover potential overdrafts in checking account.

ISF Fee International Transactions are those transactions using your debit card made outside of the United States. An International Service Fee ("ISF") amounting to 1% for ATM transactions and 3% of the transaction amount for transactions made some place other than an ATM will be posted to your account for any International Transaction, even those in US dollars. A full description of the currency conversion process is contained in the agreement that will come with your debit card.

Item Presented For Payment Against Insufficient Funds (NSF)

* NSF Charge - Paid Item - $38.00

* NSF Charge - Returned Item - $38.00

These charges are applied for processing items presented for payment against insufficient funds (NSF) with a maximum of six (6) charges per day. These charges are imposed on items created by check, in-person withdrawal, ATM withdrawal, or other electronic means.

Non Staff-Assisted Call $1.00/call over 15/month

Personalized Check Card fee $10.00

Reconcile Statement $25.00/hour

Research $25.00/hour, $3.00/copy or fax

Return of Cancelled Checks $5.00/month

Returned Deposited Item $6.00/item

Returned Deposited Foreign Item $25.00/item

Rerun Deposited Item $7.00/item

Special Statement* $5.00

Staff-Assisted Call $1.00/call over 5/month

Stop Payment Request $30.00/request

Telephone Transfer Fee $3.00/transfer

Wire Transfers

* Incoming (Customer) - $10.00

* Manual Outgoing (Customer) - $20.00

* Manual Outgoing (Repetitive) - $19.00

With Confirmation

* Fax/Email - $23.00

* Mail - $25.00

* Phone - $25.00

* Manual Outgoing (Non-Customer) - $45.00

International:

* Incoming Customer - $15.00

* Outgoing - $45.00

Confirmation of Incoming or Outgoing:

* Fax/Email - $3.00

* Mail - $5.00

* Phone - $5.00

*A special statement may include, but not be exclusive to the following: daily statements, duplicate statements, hold statements and statement printouts.

Effective June 1, 2008

NOTE: The above noted fees and service charges are not set bank-wide. These prices are driven by the competition in your local market.

AS REQUIRED BY FEDERAL LAW, COMPASS BANK RESERVES THE RIGHT TO REQUIRE AT LEAST SEVEN (7) DAYS NOTICE PRIOR TO WITHDRAWAL OR TRANSFER OF FUNDS FROM ANY INTEREST EARNING ACCOUNT.

Rev. 4/08

#1 Consumer Comment

What are you going to report?

AUTHOR: Ken - (U.S.A.)

SUBMITTED: Thursday, September 04, 2008

The bank isn't doing anything wrong. They are processing items in the order they told you they would when you opened the account. The order of items shouldn't matter anyway if you have the funds in the account to cover them. If you don't, it is YOU that just broke the law by negotiating a bad check.

This just underscores the fact that not keeping a register and balancing your account, is very expensive.

Related Reports

07:47 PM

06:16 PM

08:22 AM

12:27 PM

06:08 PM

09:17 PM

12:07 PM

05:27 PM

07:09 AM

10:56 AM

11:36 PM

04:06 PM

08:17 AM

06:10 PM

01:48 PM

01:42 PM

12:01 PM

07:33 PM

08:57 PM

07:29 PM

06:46 AM

04:10 PM

12:03 PM

11:28 AM

Advertisers above have met our

strict standards for business conduct.