Complaint Review: Compass Bank - Mobile Alabama

- Author Confirmed

- Compass Bank compassbank.com Mobile, Alabama U.S.A.

- Phone: 251-297-3000

- Web:

- Category: Banks

Compass Bank ripoff Mobile Alabama

*Consumer Comment: R - Aloha, Oregon

*Consumer Comment: Why are so many people defending Compass Bank

*Consumer Suggestion: You got a good deal

*Consumer Suggestion: You got a good deal

*Consumer Suggestion: You got a good deal

*Consumer Comment: Losing your temper got you nowhere

*Author of original report: Mark, Mark, Mark , What I find offensive is that you find it difficult to understand that someone would not stand by and be taken advantage of

*Consumer Comment: Wrong again Mark.

*Consumer Comment: Robert, Robert this guy has to be a Compass employee.

*Consumer Comment: There must be another side to this story.

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

Compass Bank and the Holier than Thou Attitude....

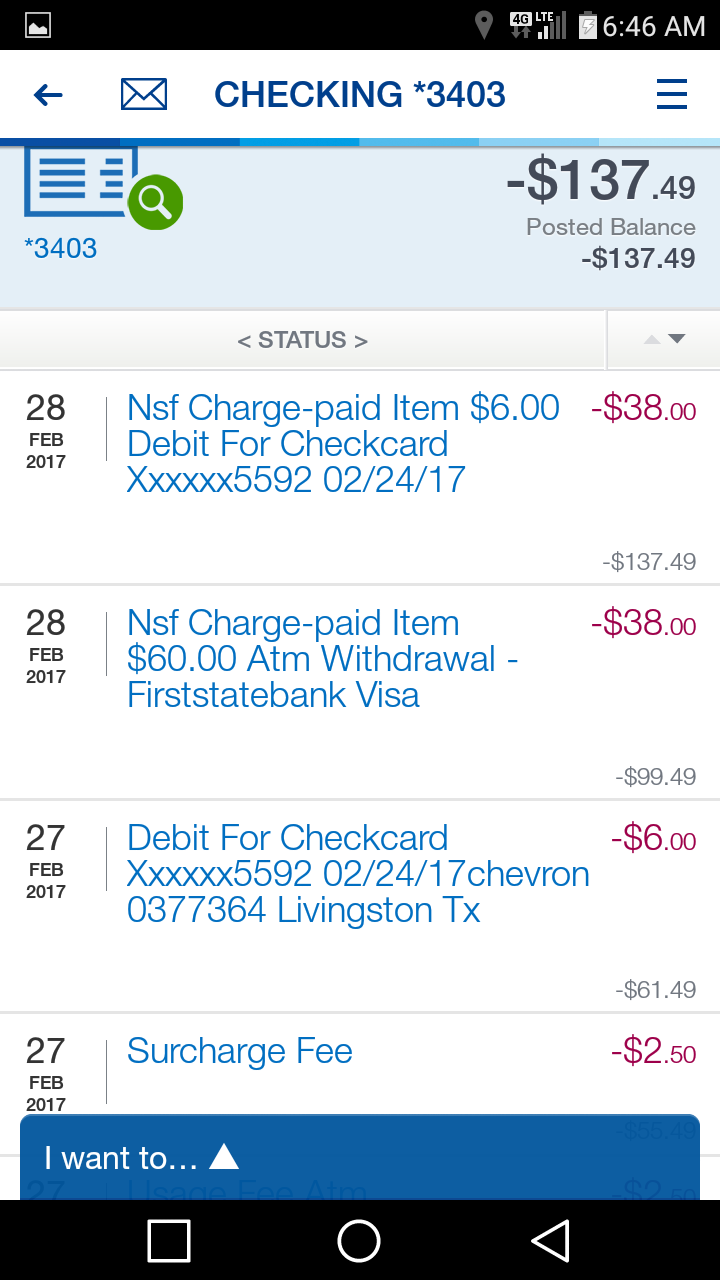

As stated in a previous complaint made by Erin in Houston I too got screwed by Compass bank and their accoutning practices... I had a deposit that went in electronically on Thursday night and did not get "posted" until Saturday.. however they did place the money in the "available" balance... when all my purchases went in on Friday they charged me 36.oo NSF fees for all transaction because the balance was not "officially" posted until Sat. When I complained I got the ususal corporate run around I finally got to speak with the regional president Mr. Mike Grainger in the Mobile office.... after explaining my situation he stated "that it was not his fault that I was incompetent and did not understand the banking business.

After a few more exchanges he also stated "that I have had to deal with idiots like this before" I asked for the corporate phone number and he said that "since you are so smart look it up in the phonebook." I did find out that the corporate number is not listed.. so I called that Alabama Banking Commission and they gave me the number. I spoke with a low-level peon named Burt Yates and he called me back later that day and stated that he would put the NSF charges back into my account but that Mr. Grainger had closed that account. He told me to take that offer or they would not put the money back into the account and still would close the account. I called the corporate office again and asked a Ms. Karen Roper if that is how they did business by closing the accounts of all people who complained. She said that they did not do business that way and would take care of the situation. She did not return my calls and did not call back. After 2 days I called the office again after I got a letter stating that they would be closing the account and that I was not allowed to come onto Compass Bank properties.

I spoke with a Ms Marilyn in the legal department and she was so helpful...she told me that the only way that I would be barred was if I had made a scene in the bank..I told her that I had not been into the bank..she said that it made no sense and she would check into it for me..she did call me back and state that she would have the NSF charges put back into the account but that Mr. Grainger would not under any circumstances keep the account open...her opinion was that I stepped onto to many toes and they were "pissed off" My reply was that I did want to talk with Mr. Jones the Chairman of the Board for Compass Bancshares....but unfourtunatly he is obviously to busy to listen to a customer...all I have to say is watch out for this scam...oh yeah did I mention that the money they took out for NSF was the amount that I had written a check for...and they cleared that check and still had to audacity to charge me 36.00 for NSF...how is that for sticking it to you.

Wayne

Mobile, Alabama

U.S.A.

This report was posted on Ripoff Report on 08/07/2005 07:28 PM and is a permanent record located here: https://www.ripoffreport.com/reports/compass-bank/mobile-alabama-36604/compass-bank-ripoff-mobile-alabama-152855. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#10 Consumer Comment

R - Aloha, Oregon

AUTHOR: Hunter - (U.S.A.)

SUBMITTED: Tuesday, June 20, 2006

Thanks for contributing to this report by saying that he did a lot of redneck cussing you troll. That's such a "tolerant" response from the "tolerant" Northwest of the USA.

To the original poster, I don't doubt what you are stipulating because they did the same to me in the same exact manner. Compass basically delays as you rightly suspect, the deposits it receives, and then misleads the consumer by posting it in the available balance. Usually at banks, the Ledger Balance is the one that banks will tell you may not represent your true balance in your account.

However, Compass demonstrates all too well that it's the reverse, and thus, they have a NSF fee party at your expense. I think it's disgusting and the guy closing your account was way out of line.

Frankly, I would report that individual personally to the Banking Commission in your state. Securities Reps have a form where all customer complaints show up so I suspect that bankers have them too. Good Luck!

Hunter

Denton, TX

#9 Consumer Comment

Why are so many people defending Compass Bank

AUTHOR: David - (U.S.A.)

SUBMITTED: Monday, October 17, 2005

It is very interesting to me that so many people are sending a reponse to defend Compass Bank -- smacks of an orchastreted effort to discredit people with valid complaints.

On this tread, I did not see one person actually ask to fully understand the original complaint, just to critize.

In my dealings with Compass Bank, I do not believe they are criminally liable, but HAVE NO MORAL FIBER, and, as a result of the "predatory" NSF fee "agreements" they are making tens of thousand of "valued customers" suffer every day.

Compass Bank should be investigate by Congress, FDIC, ABA, BBB, DOJ, SEC and every other agency that SHOULD BE PROTECTING the consumer -- but, you and I both know that the Board of Directors, and all the execs, making millions, and contributing the the corrupt "dubya" - that's "George dubya Bush the 113th or whatever" are not going to allow the federal government agencies to perform an unbiased investigation.

My suggestion is for every Compass Bank customer, who has EVER gotten an NSF, to write to their Senator, and Congressman, requesting that Banking regulations be changed to prevent the "predatory" NSF fee collection from banks such as the immoral Compass Bank.

#8 Consumer Suggestion

You got a good deal

AUTHOR: R - (U.S.A.)

SUBMITTED: Sunday, October 02, 2005

You were probably doing a lot of redneck cussing (I usually can't understand a d**n word you people say) and made a huge scene. I wouldn't be surprised if you actually issued some veiled threats. No ones going to put up with that from some hillbilly loser such as yourself.

They gave you your fees back and told you to screw. I think that's a good deal.

I would have called the cops on you.

#7 Consumer Suggestion

You got a good deal

AUTHOR: R - (U.S.A.)

SUBMITTED: Sunday, October 02, 2005

You were probably doing a lot of redneck cussing (I usually can't understand a d**n word you people say) and made a huge scene. I wouldn't be surprised if you actually issued some veiled threats. No ones going to put up with that from some hillbilly loser such as yourself.

They gave you your fees back and told you to screw. I think that's a good deal.

I would have called the cops on you.

#6 Consumer Suggestion

You got a good deal

AUTHOR: R - (U.S.A.)

SUBMITTED: Sunday, October 02, 2005

You were probably doing a lot of redneck cussing (I usually can't understand a d**n word you people say) and made a huge scene. I wouldn't be surprised if you actually issued some veiled threats. No ones going to put up with that from some hillbilly loser such as yourself.

They gave you your fees back and told you to screw. I think that's a good deal.

I would have called the cops on you.

#5 Consumer Comment

Losing your temper got you nowhere

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Sunday, October 02, 2005

Many years ago, I had an account with NCNB. They are now BoA. I had an ATM card that had a flaw in the strip. It would deduct a $19 fee every time I used it. I had NSF fees every month, but couldn't figure it out.

It took nearly a year, and an untold amount of money to find out what was doing it. I walked into the bank and told the teller I wanted all of my money, and that I was going to another bank. She asked why, and I told her. She got the manager and both of them told me there was no way the ATM card could do that. I said "watch this" and went to the ATM outside the front door. I put it in, and got a balance. I did this until the balance read $0. When I went back in, they refunded my $19/per inquiry and offered to give me another card. I asked about all the money they stole during the previous months. They said there was nothing they could do about those. I got my money and left.

Getting hostile in a place where you are going to lose is useless. As for the immediate assumption that I just take alot of stuff off people, yeah, that would explain my two trials for "aggrivated assault with a deadly weapon"(found not guilty) and the one for what I like to call "hunting down a dog"(ditto). I take nothing off of anyone, but I also know when to back off from the situation. You should look into some anger management if dealing with the bank employees gets you riled up to the point where they banish you.

#4 Author of original report

Mark, Mark, Mark , What I find offensive is that you find it difficult to understand that someone would not stand by and be taken advantage of

AUTHOR: Wayne - (U.S.A.)

SUBMITTED: Sunday, October 02, 2005

Thanks for knowing me so well...considering that I have never overdrawn my account and that the amount of my direct deposit was actually in the available balance column that morning...What I find offensive is that you...just an average joe....find it difficult to understand that someone would not stand by and be taken advantage of..I would love to have kept my account...and had Mr. Grainger not been so smart a*s and condesending towards me and had I not been given the run-around for over 2 hours....you are right I might not have been that pissed off and probably would have been alot kinder...but what is even more amazing is that any corporation would cut and run just because 1 customer complained..no matter how loud he yelled...but then since you are so average then you wouldn't know about any problems because you probably never have had any trouble with being taken advantage of...and by the way..where are your comments about the other problems concerning Compass Bank...is there something going on with you and the local branch down here?

#3 Consumer Comment

Wrong again Mark.

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Sunday, October 02, 2005

Whenever someone has no logical argument to support their claim of a ripoff they fall bank to accusing you of being an employee.

I am not employed by any bank now or in the past. I'm just an average joe, making ends meet and maintaining a bank account with no NSF fees.

#2 Consumer Comment

Robert, Robert this guy has to be a Compass employee.

AUTHOR: Mark - (U.S.A.)

SUBMITTED: Saturday, October 01, 2005

He feels the need to defend them on many posts.....I just posted a comment yesterday re:compass and he was on it. I used to think bankers were higher on the foodchain but now lawyers are looking pretty tame...good luck.

#1 Consumer Comment

There must be another side to this story.

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Monday, August 08, 2005

If a bank takes that drastic an action as to close your acount and barr you from their property, you must have been incredibly hostile in your "exchanges".

If you had read the terms and conditions you received when you opened your account, it probably states that Compass Bank has the option to pay the overdraft or not. If they hadn't have paid the overdraft, you would have had additional fees on top of the NSF fee. It also details their policies on deposits and funds availablity. If you had read it and they had violated their policy, you would have been a better position to argue your case instead of just blowing off steam.

Hopefully you'll be more successful with your new account.

Related Reports

07:47 PM

06:16 PM

08:22 AM

12:27 PM

06:08 PM

09:17 PM

12:07 PM

05:27 PM

07:09 AM

10:56 AM

11:36 PM

04:06 PM

08:17 AM

06:10 PM

01:48 PM

01:42 PM

12:01 PM

07:33 PM

08:57 PM

07:29 PM

06:46 AM

04:10 PM

12:03 PM

11:28 AM

Advertisers above have met our

strict standards for business conduct.