Complaint Review: Compass Bank - Phoenix Arizona

- Author Confirmed

- Compass Bank 22601 N 19th Ave, STE 120 Phoenix, Arizona U.S.A.

- Phone: 623-58-1002

- Web:

- Category: Banks

Compass Bank Charge excessive NSF fees even when money was available to pay the debit. Phoenix Arizona

*Consumer Comment: Compass Bank

*Consumer Comment: Compass Bank Charges

*Consumer Comment: Terms and conditions

*Consumer Comment: Missing The Point

*Consumer Comment: Response...

*Consumer Comment: Response

*Consumer Comment: Gripe Not Valid

*Consumer Comment: Response...

*Consumer Comment: Not valid in the least.

*Consumer Comment: I think his gripe is valid...

*Consumer Comment: Dude...wait...what?

*Consumer Comment: Hmmm...

*Consumer Comment: A couple of things about your threat...

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

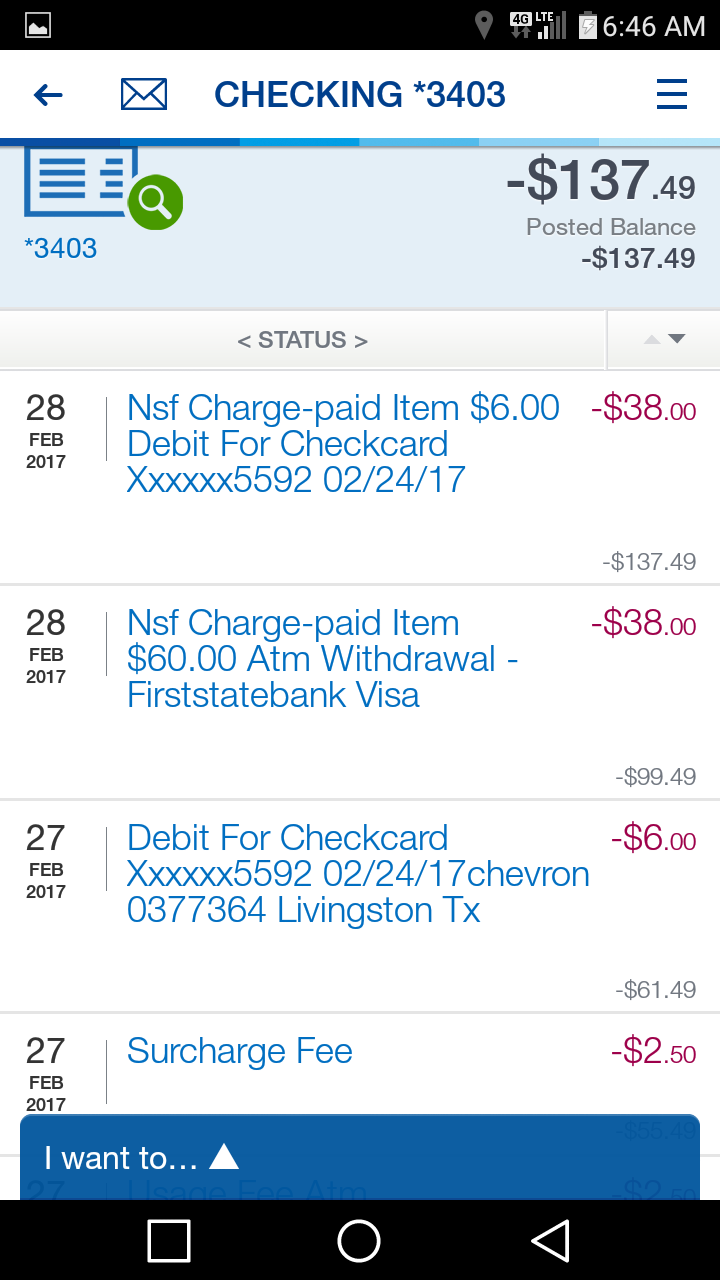

I have a Compass Bank checking account, and my $74.23 student loan payment is auto debit on the 25th of each month. I forgot to enter that in my register this month, and that resulted in an overdraft, with a NSF charge of $38.00. My bad.

The problem I have is that at the same time, a $$4.24 debit cleared, for which there was plenty of money to pay, for which they also charged me a $38.00 NSF fee.

As a result of that action, my check for $28.00 to Christian Children's fund bounced, and resulted in yet another $28.00 NSF fee. That's a total of $114.00 in NSF fees.

I'll admit I made a mistake, and deserve to be punished. I think the $38.00 NSF fee for the mistake is punishment enough.

The other $76.00 is a blantant ripoff. Their customer service rep said it was their policy to post the largest transactions first because that is what their customers prefer. She also pointed me to an obscure paragraph in the customer service agreement that states that is what they will do.

I don't know why anyone would want to pay more NSF fees than necessary, but I clearly do not!

Beware of Compass Bank. They lie in wait for you to make a mistake, and the pounce swiftly. They grab your money as their just reward for your mistake, and gleefully explain that that's the way you like it.

That's a free account. I'm going to leave it open for the rest of my life. I will have a stament mailed to me every month, and order free checks frequently. They will pay, not to me, but I am going to cost them more than they got from me.

Richard

Phoenix, Arizona

U.S.A.

This report was posted on Ripoff Report on 05/29/2009 07:56 AM and is a permanent record located here: https://www.ripoffreport.com/reports/compass-bank/phoenix-arizona-85027/compass-bank-charge-excessive-nsf-fees-even-when-money-was-available-to-pay-the-debit-pho-456465. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#13 Consumer Comment

Compass Bank

AUTHOR: Phoenix Arizona - (U.S.A.)

SUBMITTED: Friday, June 12, 2009

I had a similar situation but I went in to a teller and made a deposit. I asked specifically If I went to the store now after the deposit had been made and made a purchase then everything would be covered. She said of course we always process deposits first before debits. I then left secure in the knowledge my deposit had been made and I had funds available.

Boy was I wrong. I bought milk, filled up on gas and stopped and picked up some dinner. I got bounced check fees for all even though the teller told me my deposit was made and I would have no problems. I called the bank customer support and they told me the teller was wrong and the fee's stood.

They like to make money off of you. I then paid those fee's and waited until all my current debits and checks came through and then I closed my account. I waited 2 weeks without writing anymore checks etc as I had already started a new account at Chase bank. Once I was 100% certain that all had gone through I closed my acct and took out the little bit of money that was left.

four years later I get a letter stating I have fee's to pay them. Funny they hadn't been worried for the past four years about anything I owed. I owe them nothing as I paid it all. I didn't run or hide and have had listed phone and address for the last 4 years, 2 of which was in the same apt that they had in their records.

#12 Consumer Comment

Compass Bank Charges

AUTHOR: Bronxboi - (U.S.A.)

SUBMITTED: Wednesday, June 10, 2009

There is no way that I would look at the OD fees as a deterrent they now only exist for pure profit. Banks have positioned themself in a way appear that they are doing things for one purpose but in all actuality their actions only inflate their bottom line. If OD and account was looked upon negatively then why do they authorize charges well over your account balance. Why would they process payments in such a way to maximize the number of items that are left in negative status if a low balance exists. Banks want customers to OD so that they can get as many fees from each customer. When the banks were healthy they used to be lenient with OD fees they would take away one or two if you complained. Now they basically tell you tough. It is all about the money.

So lets get on with Compass Bank, yes I read their fee schedule and was not surprised by their charges but once thing I can tell you is that they have one of the most unethical fee structures that I have come across. I have banked with many banks in many different regions and I have never seen such a plethora of fees in my life. I just recently got out of a bad relationship and my "other" took my ATM card and hauled out as much as they could out of my account over a two day period, it actually started at 10pm into the next morning. By the time I checked my account compass at ok'd cash withdrawals that left my account with -410.00. I had three pending transactions and I called customer service and they said well you will need to file a police report. You know I know it is theft but I really just can't bring myself to introducting someone into the criminal justice system unless it is for something downright severe. Moving on, after all charges and I did forget one more I had a negative balance of 610.00. I transferred 600.00 into the account and guess what they levied a 42.00 OD fee and then started 7.00 per day OD fee (including weekends). Now yes I know the schedule says they can do it but does it make it right. It just feels wrong. Also, the original OD actually was erased 6 days later but due to a final item on the 7th day it pushed the OD further out to ten days. So technically my overdraft should not be dated as over 7 days so that they can levy their 7 day fee on the amount. But guess what they don't care they just want the money. I will stick it out with them for another three months till I leave the area but I don't want to do any business with them again. By the way I had the account for 1 year and never overdrafted so this is not a common thing for me.

#11 Consumer Comment

Terms and conditions

AUTHOR: Flynrider - (U.S.A.)

SUBMITTED: Wednesday, June 03, 2009

I opened a bank account last month. The "welcome" packet had about 20 pages of mostly junk, but the terms and conditions were 3 pages long. Easily read in a few minutes. If it had been 50 pages long, I would have just closed the account and gone elsewhere.

#10 Consumer Comment

Missing The Point

AUTHOR: Jim - (U.S.A.)

SUBMITTED: Tuesday, June 02, 2009

For the person from Canada, you're indicating the bank was unreasonable in the way it "stacked" NSF transactions. The truth is that there is nothing unreasonable about their actions. For it to be unreasonable and wrong would mean that they violated the terms of their agreement with their account holder. It didn't. The bank, like all others, followed the agreement to the letter. The problem here is people like the OP (and you - BTW) are trying to arbiter what exactly should be sufficient punishment. Neither the OP, you, or I can make value judgments about what is right or what is wrong; that's why there is an agreement. With a written agreement, there is no subjectivity. The agreement is the basis for what can be done and what can't be done.

The account agreement is not 50 pages or even 100. In fact, to show you how ludicrous your own point is, signing a mortgage document is about 75-100 pages and that will be the MOST complex document any consumer will have to read sign and most banks force you to READ that document before signing any of the pages. An account agreement doesn't come anywhere close to that number of pages; if it's even 7-10 pages, I would be surprised. The point here is that people don't read even the most basic of agreements when it involves their own money - it's no wonder why so many people who complain here don't understand how a bank could do this. It's simple - because they can based on the agreement you have with them and because they don't understand the consequences of (1) not keeping an accurate register (2) using a debit card when few people understand the consequences of that instrument, and (3) thinking a bank will toss out their own rules when it comes to their own situation.

The only determiner here is what is in the agreement and the OP doesn't like what happened. Too bad. Unfortunately, all banks are the same in this regard - they all have similar to almost 100% identical processes as this bank. Clsong the account and moving it elsewhere is a pointless exercise - as is leaving the money there to do nothing and sit there.

#9 Consumer Comment

Response...

AUTHOR: Edgeman - (U.S.A.)

SUBMITTED: Tuesday, June 02, 2009

"As one would tell the IHOP gravy lady, s**t happens. If you were to tell me you've never in your life had an overdraft, I would not believe you. Basically what you're saying is that if you make a mistake that is preventable, there should be no limit on the punishment rendered. That's unreasonable."

Response: As it happens, I received two overdraft fees when I was nineteen. At the time I couldn't afford to take a hit like that so I made sure to not let it happen again. And I didn't write anything along the lines of what you're claiming. I simply wrote that one can choose not to pay overdraft fees. Considering that the majority of account holders don't pay those fees, I'd say that most people do choose not to pay them.

"You should see the binder of stuff I got last time I opened a bank account. I think it was actually closer to 100 pages than 50. This may not go for every type of account at every bank. I didn't read it. Maybe I should have. I'll grant you that. It's still bad practice."

Response: Which bank? I've had accounts at many of them and no, I have never received anything that took a long time to read. I maintain that one should not sign a legally binding agreement before reading it.

"This would obviously be after the merchant submits the request to the bank. Something which should happen on the spot anyway, but that would be up to the merchant."

Response: After the merchant submits the charge it goes from their bank to the ACH and then to your bank. Five seconds is unrealistic.

"You're missing the point. He knows he screwed up. What was excessive was for the bank to stack NSF fees in the order that maximized their take. In theory, someone who has 100 transactions in a day averaging $20 each and a single transaction for over $2,000 that bounced would be hit with $3800 in NSF fees. That's an extreme case, but it demonstrates why this is wrong."

Response: Extreme case aside, it doesn't matter how transactions are processed so long as you stay within your available account balance. If one agrees to the terms that say the bank can process transactions in any order and then fails to properly manage their account, then he or she has set themselves up for a severe financial mishap. For the record, I don't like overdraft fees and I think that people shouldn't be paying them. It's obvious that you agree at least with that principle.

The good news is that overdraft fees can easily be avoided. The OP was charged overdraft fees due to his actions. On top of that, his plan for "revenge" will only damage himself. The time could be more productively spent.

#8 Consumer Comment

Response

AUTHOR: Myfutureselfnme - (Canada)

SUBMITTED: Monday, June 01, 2009

"Response: Well, I think that it's wrong to give billions of taxpayer dollars to companies that wind up going bankrupt anyways. We're both in for dissapointment. The difference is, people can choose not to overdraft their accounts."

As one would tell the IHOP gravy lady, s**t happens. If you were to tell me you've never in your life had an overdraft, I would not believe you. Basically what you're saying is that if you make a mistake that is preventable, there should be no limit on the punishment rendered. That's unreasonable.

"Response: You're exaggerating about the 50 pages of legalese. It shouldn't take longer than ten or fifteen minutes to read through the terms and conditions. I work full time and I'm a student and I can find a few minutes to read the leases, loan agreements, etc. I can't think of a good reason to not read a legally binding agreement, especially when your money is at stake."

You should see the binder of stuff I got last time I opened a bank account. I think it was actually closer to 100 pages than 50. This may not go for every type of account at every bank. I didn't read it. Maybe I should have. I'll grant you that. It's still bad practice.

"Response: And how would the government be able to force merchants to submit all of their payment requests within five seconds?"

This would obviously be after the merchant submits the request to the bank. Something which should happen on the spot anyway, but that would be up to the merchant.

"Response: I think that the time would be better spent brushing up on financial management techniques. The problem will simply follow him to the new bank if he doesn't."

You're missing the point. He knows he screwed up. What was excessive was for the bank to stack NSF fees in the order that maximized their take. In theory, someone who has 100 transactions in a day averaging $20 each and a single transaction for over $2,000 that bounced would be hit with $3800 in NSF fees. That's an extreme case, but it demonstrates why this is wrong.

#7 Consumer Comment

Response...

AUTHOR: Edgeman - (U.S.A.)

SUBMITTED: Monday, June 01, 2009

"I think it's wrong for banks to post transactions from largest to smallest. They do this for the specific reason that it allows them to charge the maximum number of overdraft fees. This is a strategic move, the reasons are obvious, and I think that most banks do it."

Response: Well, I think that it's wrong to give billions of taxpayer dollars to companies that wind up going bankrupt anyways. We're both in for dissapointment. The difference is, people can choose not to overdraft their accounts.

"The fact that it was disclosed to him in what was likely 50 or more pages of legalese should not be considered an excuse. I don't have time to read 50 pages of legalese when I open an account. Maybe you do, but I don't. In my opinion, any transaction that involves a consumer should involve 300 words or less of contract. I think that should be the law. If they can't fit it into 300 words, it shouldn't happen, period."

Response: You're exaggerating about the 50 pages of legalese. It shouldn't take longer than ten or fifteen minutes to read through the terms and conditions. I work full time and I'm a student and I can find a few minutes to read the leases, loan agreements, etc. I can't think of a good reason to not read a legally binding agreement, especially when your money is at stake.

"Further, I think that the ABA system is grossly outdated. I don't know about you, but it's been years since I've written a paper check. Everything is an EFT these days, and for some reason EFT's are left to rot for as long as a couple days in the banking system before they actually clear. And it's only as fast as it is because the government mandates it. In my opinion, the government should mandate that it take no longer than five seconds."

Response: And how would the government be able to force merchants to submit all of their payment requests within five seconds?

"This is all my opinion. Sorry about the loss of the original poster, but some of us have lost much more in the past and I think rather than try to get vengeance on the bank, he should eat the loss and spend some time researching which other bank would be best to switch to."

Response: I think that the time would be better spent brushing up on financial management techniques. The problem will simply follow him to the new bank if he doesn't.

#6 Consumer Comment

Not valid in the least.

AUTHOR: John - (U.S.A.)

SUBMITTED: Monday, June 01, 2009

There are millions that do not overdraft every single day.

The fee is meant as a deterrent.......in other words, you get hit with the first one or three and you are suppose to say 'how did I do this? Let me look at my register........oh that's right.....I don't keep one. Maybe I should. I always had to before.'

Then, you see where you erred and learn how to stop doing it.

If you didn't learn after the first time, that's your fault.

#5 Consumer Comment

Gripe Not Valid

AUTHOR: Jim - (U.S.A.)

SUBMITTED: Monday, June 01, 2009

It doesn't matter how a bank orders transactions unless you don't have enough money in the bank. The lesson here is to keep an accurate register, resist the use of debit cards, and minimize the number of ACH debits running through your account if you think for a moment you're going to have trouble tracking your balance. So far, the OP has 2 of the latter that overdrew his account. Time to assess how "convenient" this sort of banking is for you?

BTW - Striderq is right. Once a bank determines the account is dormant, they will close the account and send the money to the Treasurer of the State you live in; the money won't go to you. If you want to see how hard it will be to get that money back, try that! It doesn't cost a bank anything to maintain an inactive account - only an active one. And at that - iit doesn't cost the bank much...

#4 Consumer Comment

I think his gripe is valid...

AUTHOR: Myfutureselfnme - (Canada)

SUBMITTED: Monday, June 01, 2009

I think it's wrong for banks to post transactions from largest to smallest. They do this for the specific reason that it allows them to charge the maximum number of overdraft fees. This is a strategic move, the reasons are obvious, and I think that most banks do it.

The fact that it was disclosed to him in what was likely 50 or more pages of legalese should not be considered an excuse. I don't have time to read 50 pages of legalese when I open an account. Maybe you do, but I don't. In my opinion, any transaction that involves a consumer should involve 300 words or less of contract. I think that should be the law. If they can't fit it into 300 words, it shouldn't happen, period.

Further, I think that the ABA system is grossly outdated. I don't know about you, but it's been years since I've written a paper check. Everything is an EFT these days, and for some reason EFT's are left to rot for as long as a couple days in the banking system before they actually clear. And it's only as fast as it is because the government mandates it. In my opinion, the government should mandate that it take no longer than five seconds.

This is all my opinion. Sorry about the loss of the original poster, but some of us have lost much more in the past and I think rather than try to get vengeance on the bank, he should eat the loss and spend some time researching which other bank would be best to switch to.

#3 Consumer Comment

Dude...wait...what?

AUTHOR: Edgeman - (U.S.A.)

SUBMITTED: Saturday, May 30, 2009

I want to make certain that I understand this before commenting further.

1. You overdrafted your account which in turn caused two other pending transactions to overdraft as well.

2. You are upset at the bank because they processed the transactions in the way that they disclosed to you in the terms and conditions that you agreed to when you opened the account.

3. Your plan for revenge is to order checks that you think are free but will actually be charged to your account. You are also going to let the account go dormant and be charged the associated fees and have your credit score go down which will cause your interest rates to go up. In other words, you will damage yourself while having no discernible effect on the bank.

Is there anything else? This seems like a silly course of action to take and all of this could have been avoided with a little more care when managing your finances.

#2 Consumer Comment

Hmmm...

AUTHOR: Flynrider - (U.S.A.)

SUBMITTED: Saturday, May 30, 2009

"She also pointed me to an obscure paragraph in the customer service agreement that states that is what they will do."

Let me guess, you consider this paragraph to be obscure because you did not bother to read it, right?

When you quit using Compass bank, be sure to come back and tell us the "obscure" transaction posting policy of the next bank you deal with. We will wait in amusement.

Striderq : You gave away the punchline. I was certain we'd be hearing back from this guy in about a year, complaining how they charged him NSF/OD fees on his inactive account. I know it's bad, but sometimes I like to see the results when these self styled geniuses decide they've figured out how to get revenge on a bank.

#1 Consumer Comment

A couple of things about your threat...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Friday, May 29, 2009

You may want to check the price of checks before you order them. In most banks, the free checking refers to no balance requirement and no monthly service fees. Not free checks every time you order.

Additionally, each state has a time limt for an account being declared dormant. This means if there are no customer generated activity (teller/ATM deposits or checks/debit card purchases) within a set time limit then the account is declared dormant. Most banks then access a dormant fee until the time limti in that state for the account to be declared abandoned and sent to the state unclaimed property section. However, any money in the account it deducted for the dormancy fees or these fees cause the account to be overdrawn eventually leading to the account being closed due to the overdraft. So if you have enough money in it to keep it from being closed, then you will lose that money to the dormancy fees. If the account is closed as overdrawn, there is usually an additional fee and then this account is reported to Chexsystems and possibly the credit agencies. Either your money is tied up and you lose some and then have to claim it from the state or the account goes negative and you are liable for the negative balance and all fees accessed.

Basically, if you don't like the way the bank does business, the best thing to do is to close your account, find another bank, ask how they do business, when you find one you can deal with then open an account. However I'll give you a tip. Most banks conduct business the same way with the biggest difference being does the bank post credits before or after the debits each night during processing. But good luck with your plan, please keep us informed as to how it works out for you.

Related Reports

07:47 PM

06:16 PM

08:22 AM

12:27 PM

06:08 PM

09:17 PM

12:07 PM

05:27 PM

07:09 AM

10:56 AM

11:36 PM

04:06 PM

08:17 AM

06:10 PM

01:48 PM

01:42 PM

12:01 PM

07:33 PM

08:57 PM

07:29 PM

06:46 AM

04:10 PM

12:03 PM

11:28 AM

Advertisers above have met our

strict standards for business conduct.