Complaint Review: SunTrust Bank - Charlottesville Virginia

- Author Confirmed

- SunTrust Bank Barracks Road Branch Charlottesville, Virginia United States of America

- Phone: 434-295-3494

- Web:

- Category: Banks

SunTrust Bank Cannot stop transactions from my accessing my checking account. Cannot close account. Exorbitant overdraft fees incurred. Charlottesville, Virginia

*Consumer Comment: Are you voluntarily enrolled in "overdraft protection?

*General Comment: A couple of things...

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

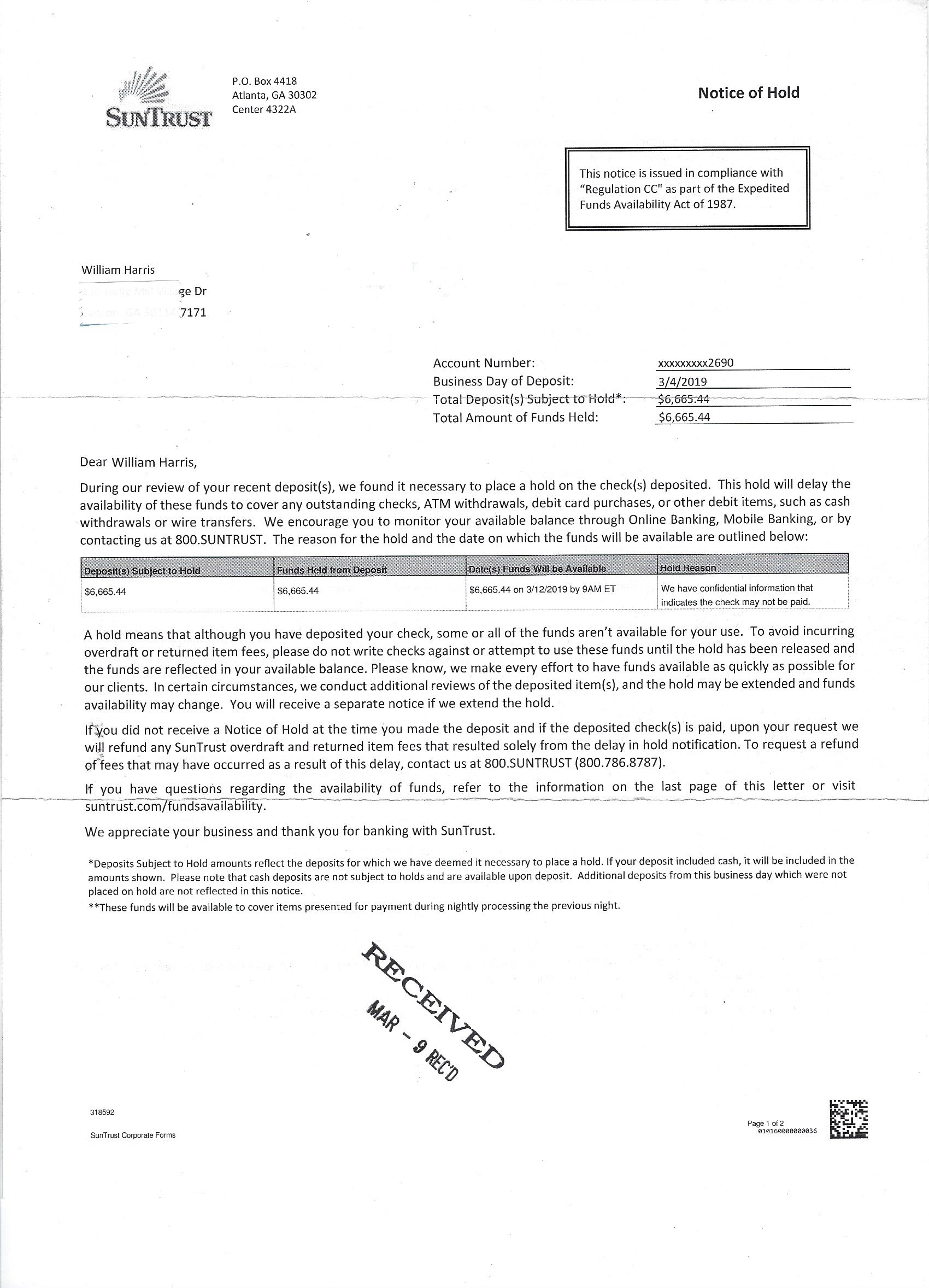

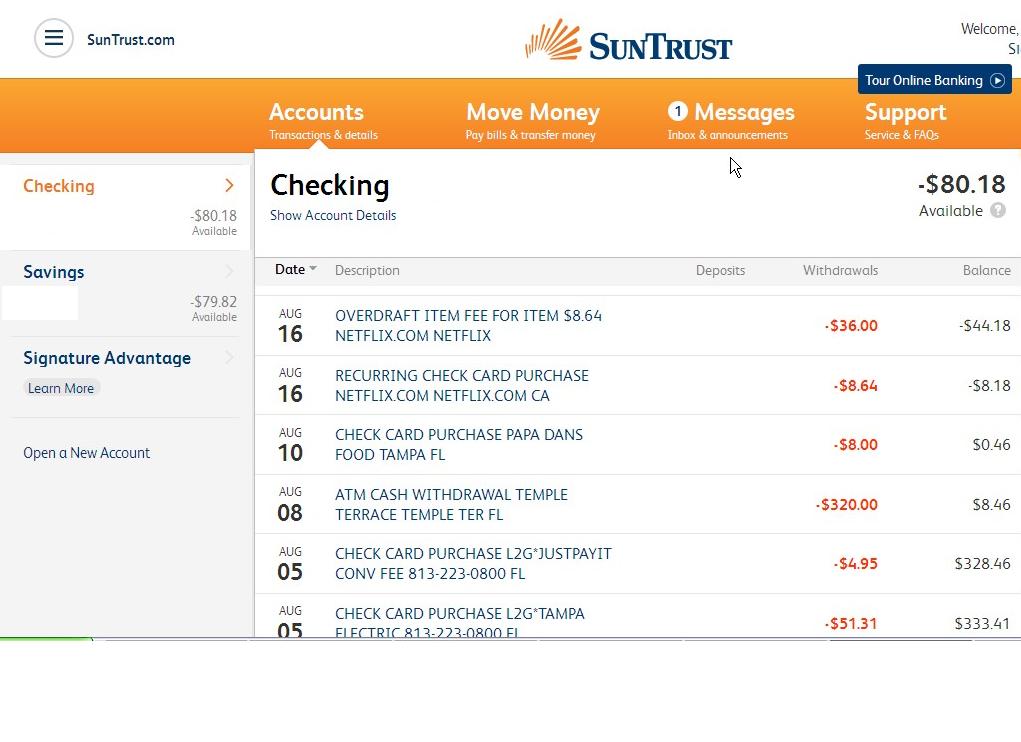

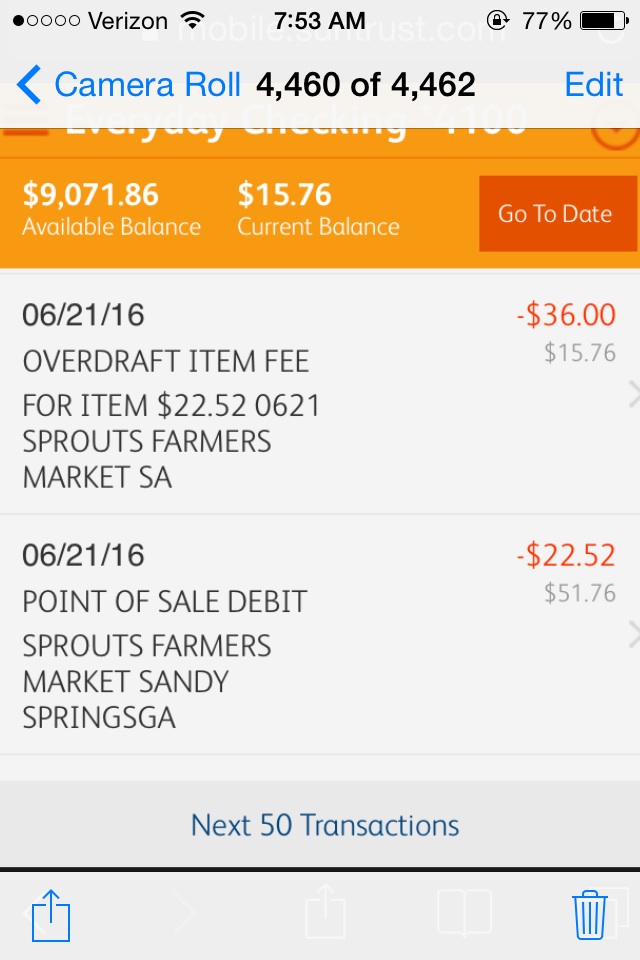

I had many pending ACH transactions posting against my checking account. I arranged for add'l funds to be deposited in my account to cover a rent check. Theadd'l funds were not released to my account in a timely manner and the bank processed the rent check first and caused all my pending items to either be paid or returned incurring high overdraft fees.

I could not get the bank to refund very many of the charges. They refunded $36.00, then billed me another $72 then forgave $72. Meanwhile, I had around $600 of fees. The ACH transactions going against my account can not be stopped by the bank. I could not get the bank to close the account. Even if the account were to be closed, any transaction posting against the account within 5 days would cause the account to be re-opened and more fees assessed.

I don't have the money to pay down all the fees and more are accumulating due to the banks inability or desire to do ANYTHING. This bank has ruined me financially.

How can a bank NOT be able to prevent my account from having add'l transactions posted to it? I will be contacting any and all government and consumer groups and further explain the horrendous behavior of this bank.

*EDitor's Suggestions on how to get your money back into your bank account that someone

wrongfully takes it from you!

EDitor's Suggestions on how to get your money back! HERE IS WHAT RIP-OFF REPORT SUGGESTS YOU DO:

Go to your bank within 60 days of the charge, or as soon as you know about the charge, don't delay, and tell them that there has been fraudulent activity within your account. Explain that you wish to file a dispute, and demand that they assist you in accordance with Federal Regulation E.

According to the majority of victims interviewed by Rip-off Report, those who immediately called their banks to dispute the charges did not get very far. Many victims got the following responses from their banks: we could not do anything for you or you waited too long; it has been more than 60 days.

If the bank is says that you have waited too long, explain to them how you called their 800 number as soon as the charges were found, and were told by the bank that nothing could be done. Remind the bank that they failed to assist you properly at the 800 #, and instead, provided you with an inadequate explanation of your right to dispute. Tell the bank that it's their fault time has expired, and since they gave you the wrong info to begin with, they will just have to deal with it, take the loss and reverse the charges.

Tell them the truth; this was unauthorized and your account was NOT to be charged! Keep emphasizing how you never authorized anything! Direct them to the hundreds of victims reports that were filed on Rip-off Report.com. And if you're at the bank, walk them over to their computer and make them go to this site! If you are on the phone with them, tell them you will wait while they access this site! Either way, be persistent!

DO NOT TAKE NO FOR AN ANSWER!

Let them know nicely, that you were advised to Report them (the Bank) and this situation to the Banking Commission in your state. Since each state has a different name for the agency/controller over banks, find that name before you call or get to the bank so you can throw it in their face. The more knowledgeable you appear to be, the further you will get.

And just continue to demand the Federal Regulation E form! The bank CAN, MUST and WILL reverse the charge! But, you must be persistent; ask to speak to the supervisor or the area manager for all the branches in the state.

Let the bank personnel know you are meeting with the media later in the day, that you would much rather they do the right thing (as most other banks have) by looking at the complaints and immediately reversing the charge(s) to your account; no matter how long ago it was. Be sure to call the Media if necessary so you are telling the truth.

If you have to, be loud (but nice) in front of other customers. If you are just calling by phone, the above tactics should still work. The bank can easily fax or mail to you the Federal Regulation E dispute form.

This report was posted on Ripoff Report on 04/24/2012 12:36 PM and is a permanent record located here: https://www.ripoffreport.com/reports/suntrust-bank/charlottesville-virginia-/suntrust-bank-cannot-stop-transactions-from-my-accessing-my-checking-account-cannot-clos-873088. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#2 Consumer Comment

Are you voluntarily enrolled in "overdraft protection?

AUTHOR: Ronny g - (USA)

SUBMITTED: Tuesday, April 24, 2012

Only reason I ask is because you state a lot of fees ($600.00) were charged to your account because you bounced some ACH payments and they posted it first.

If you were not voluntarily opted into overdraft protection they can not charge you a dime in fees other then "per" whatever "ACH" payments were submitted when your account balance could not cover it. Legally they can not charge you a dime in fees for any transactions other then ACH if not opted into OD protection for example any debit card transactions since it would be the banks responsibility to decline it at the time if funds were not available. This is why when you swipe the card it instantly either "accepts" or "declines" the transaction. For your own good actually since humans do on occasion make mistakes especially if financially struggling paycheck to paycheck or had some kind of unauthorized/unknown "hold" or "charge" placed on the account they were unaware of.

Just something to consider other then being a LOT more careful not to pay a bill via ACH when your account can not cover it. Because the only possible outcome is the bank will cover it and charge you $25 to $35 per violation...or worse, they will not cover it and still charge you $25- $35 per...plus whatever negative impact is applied by the payee which could not only be additional fees of whatever they state..but tank whatever is left of your credit rating and that in the long run can really, really hurt you financially.

#1 General Comment

A couple of things...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Tuesday, April 24, 2012

A stop payment on an ACH transaction is very similar to a stop payment on a check. One major difference is that with an ACH transaction, one from that company must have posted to your account to allow the bank to get the company number. The stop is then placed on the company number, company name and amount. It is not effective for the date you request the stop. Most banks also have a 6 month time frame and then the stop expires allowing that ACH to be processed.

However, like a check stop payment there is a fee to place the stop. You must have the money available in your account to pay the stop fee before the bank will place the stop. If you don't have enough or your account is in the negative, the bank won't place the stop.

Banks will not close an account with a negative balance at the account owners request. As you stated any transactions coming in will force the account reopen and cause additional fees.

I'm sorry to hear of your situation but the bank didn't cause your "financial ruin". That was caused by someone writing checks and authorizing ACH debits when the money wasn't available to cover them. All banks are pretty much the same so if/when you get this squared away it could easily happen again at another bank. Sorry but not a ripoff.

Related Reports

09:06 PM

11:29 PM

11:31 PM

12:17 PM

08:04 AM

10:38 AM

06:54 AM

02:30 PM

12:08 PM

09:36 AM

02:39 PM

09:51 AM

03:00 PM

04:42 PM

07:04 PM

09:21 PM

08:12 AM

06:36 AM

01:25 PM

04:20 PM

08:20 AM

10:51 AM

01:10 PM

11:38 AM

08:32 PM

Advertisers above have met our

strict standards for business conduct.