Complaint Review: BBVA Compass Bank - Mesquite Texas

- Author Not Confirmed

- BBVA Compass Bank 311 N. Galloway Ave. Mesquite, Texas United States of America

- Phone: 9727054362

- Web:

- Category: Banks

BBVA Compass Bank Manipulate Check/Deposit Order to Extract More NSF Fees Mesquite, Texas

*Consumer Suggestion: Get results

*Consumer Suggestion: Force compliance on compass bank

*Consumer Comment: Looks like just 268 other people who don't maintain accurate check registers!

*Author of original report: FINAL UPDATE

*General Comment: Once more...

*Consumer Comment: Ya Know !!!

*Consumer Comment: The OP still doesn't get, probably never will.

*Consumer Comment: Quick question

*Consumer Comment: That did not happen the way you claim it did

*Consumer Comment: My favorite

*Author of original report: Clarification: Entitlement, no. Outrage, yes.

*Consumer Suggestion: Simple solution. Maintain an ACCURATE checkbook register!

*General Comment: My, aren't we just full of entitlement ...

*Consumer Comment: Simple resolution

*Consumer Comment: Shocking..

*Consumer Comment: question

Show customers why they should trust your business over your competitors...

listed on other sites?

Those sites steal

Ripoff Report's

content.

We can get those

removed for you!

Find out more here.

Ripoff Report

willing to make a

commitment to

customer satisfaction

Click here now..

Compass Bank routinely changes the order in which it processes the checks in personal checking accounts; the reason is clearly to obtain more NSF fees. At $38 each, the total climbs very quickly. I have a program (ScreenShot) on my computer that allows me to take a snapshot of any screen, so I've learned to check my account online daily and use that program to take a shot of my account. By doing this and comparing the print-outs, I discovered that Compass was changing the order of the checks.

Compass does not deny this practice; in fact, every representative I've spoken to defends it as being "consumer friendly." They claim that changing the order to pay the largest check first is strictly in the consumer's interest, as mortgage and utility bills are usually large amounts. I say BALONEY! This is strictly in the bank's interest - by juggling the checks' order and paying the largest amounts first, Compass is ensuring that it will receive the maximum number of NSF fees. I've argued with Compass about this without success, and I've even written to them, expressly directing them NOT to tamper with the order of my checks. In that letter, I instructed them to either process them exactly as they arrive, or process them in the order of the smallest amount first. They never responded to my letter, and they continue to do exactly as they please. Recently, they did their juggling act and charged me for 3 NSF fees; if they'd left the checks in the order in which they actually arrived, I would have incurred a single NSF fee.

When recent federal regulations changed the amount banks could wring out of consumers in other fees, Compass stepped up its "let's juggle those consumer checks" program. The State of Texas is of no help whatsoever, as Compass is apparently under the Alabama Banking Commission, which is disinclined to do anything to upset its corporate masters.

Other banks across the country have been the target of class action suits for this kind of check juggling and have been penalized for such naughtiness. Why hasn't Compass been stung yet? Are there any other ticked off little bees out there who want to join me? Buzzz!!!

This report was posted on Ripoff Report on 04/11/2012 08:50 PM and is a permanent record located here: https://www.ripoffreport.com/reports/bbva-compass-bank/mesquite-texas-75150/bbva-compass-bank-manipulate-checkdeposit-order-to-extract-more-nsf-fees-mesquite-texas-867315. The posting time indicated is Arizona local time. Arizona does not observe daylight savings so the post time may be Mountain or Pacific depending on the time of year. Ripoff Report has an exclusive license to this report. It may not be copied without the written permission of Ripoff Report. READ: Foreign websites steal our content

If you would like to see more Rip-off Reports on this company/individual, search here:

#16 Consumer Suggestion

Get results

AUTHOR: Theresa - (USA)

SUBMITTED: Friday, March 03, 2017

Theresa, Livingston Tx...file a detailed complaint with the federal reserve..they regulate all banks. They did this to me..ONCE... I wrote 2 checks with my doctors on a wednesday..I told them the money would not be in my account until friday..both doctors said that their next deposit day is not until monday and it should be fine. When the checks came in on Monday..on a large positive balance..they still charged an nsf for each check based on the date of the check rather than the day..monday...that they hit the bank. I filed a complaint with the federal reserve and they made them promptly refund the money. Good luck!

#15 Consumer Suggestion

Force compliance on compass bank

AUTHOR: Theresa - (USA)

SUBMITTED: Monday, February 27, 2017

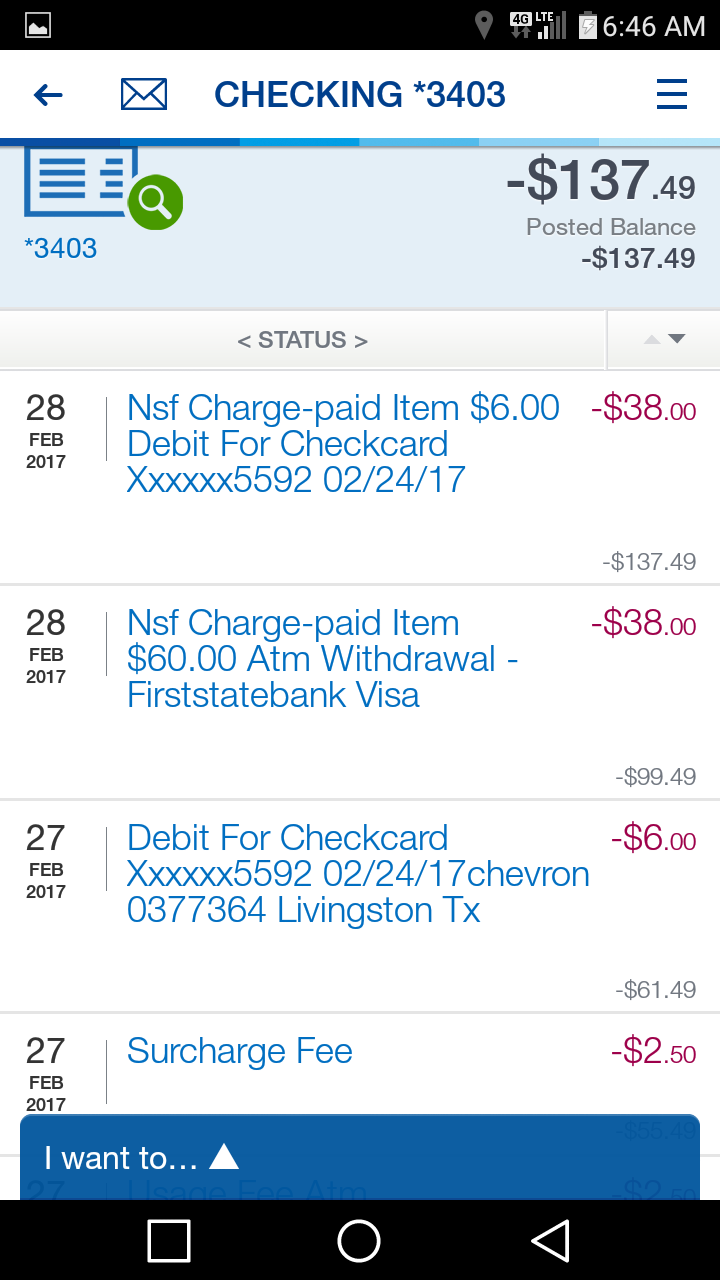

I constantly have a problem with compass bank manipulating and changing transaction dates to enable them to charge a 38.00 nsf fee, unwarranted. The last time , I wrote 2 checks to my doctors on the 29th. I told them the money would not be in my account until the 3rd. Both understood and said they would not be making another deposit until Monday..(which was the 3rd) and assured me it would be fine. The third rolls around and my direct deposit was made in the morning. I had several transactions after the deposit..and around 4 pm the checks showed up. They followed the 2 checks with 2, - $38.00 nsf fees totalling 76.00 in nsf fees , and charged this based on the date on the checks rather than the day they recieved them..which was well after my deposit. I made a complaint to the FEDERAL RESERVE. They righted this wrong and the 76.00 was immediatly refunded to my account. I advise everyone that has a legitimate complaint on compass bank to report to the federal reserve. Since this, the bank still tries to manipulate my account to collect nsf fees but I have to watch my account like a hawk..and I screenshot every transaction as it happens. I make night deposits and I video making that drop. So far..ive had to call them to the table on tricky banking 4 times and each time the account was returned to correct before they changed dates to benifit them and every time so far the money was refunded without my having to contact the federal reserve a second time. I am currently watching them as I type...I had a balance of 9.51 on feb. 24...I did a transaction on 24th of 6.00..my account showed a balance of 3.51. (I screenshotted this)On the 27th...I had to use the line of credit (od protection) for 60.00. for an emergency.. It posted on the 27th., and incures an overdraft charge of 38.00 . today..the 27th, they have changed the date on the 6.00 transaction to the 27th and put it in after the 60.00 transaction in which left this way will incure 2- $ 38.00 nsf fees. So far the fees have not been added to my account..Im waiting to see how they are going to list them. If they list the 6.00 first..there will only be one fee. We will see. INFORM THE FEDERAL RESERVE OF YOUR TROUBLE.

#14 Consumer Comment

Looks like just 268 other people who don't maintain accurate check registers!

AUTHOR: Southern Chemical and Equipment LLC - (USA)

SUBMITTED: Tuesday, April 17, 2012

Complaints mean absolutely nothing unless they are valid complaints.

From my years of being involved here on ROR, I can tell you that most of the complaints filed against banks are by those people who do not maintain accurate checkbook registers.

Take a good look at them. Most are for OD/NSF fees, posting order, etc.

All nonsense.

Learn how to properly maintain your check register and you will have no problems.

In addition to limiting your debit card usage with 2 people using the account.

Plan your purchases together, and don't use your debit card for small purchases. Use cash.

#13 Author of original report

FINAL UPDATE

AUTHOR: FelineHostage - (United States of America)

SUBMITTED: Tuesday, April 17, 2012

There are 268 complaints against Compass Bank on this website; 267 were filed prior to mine.

Statistically, only one person complains for every 45 people who experience a problem.

Do the math.

For those people who actually believe a bank has the right to do anything it wants, by all means, run right over and open up an account. You're okay with the fact that Compass merged with a South American banking entity without telling its customers, right? (Don't believe me? Do the research yourself.) You don't mind that your personal financial information could be floating around South America, do you? Great! Enjoy your banking experience with Compass. Honestly, the customer service people are terrific - they really are. It's the bank itself, with its consistently anti-consumer stance that stinks.

This website exists for the purpose of consumers posting a complaint against a business (often a mega-corporation like Compass), and explaining what happened. That's exactly what I did. I admit, I should've spent more time composing my post, in order to make it read smoother. Had I realized that an entire herd of people, none of whom were brave enough to use their real names, were just waiting to pounce with speculation and nasty comments, I would've spent more time on my post. I enjoy debate when both parties work on facts. That's not what this is. The people commenting weren't there, and cannot speak with authority about what happened. They're being rude, nothing more.

I don't intend to respond again. Go wild, children.

I encourage others who would complain to do so. Don't be intimidated by meaningless comments.

#12 General Comment

Once more...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Saturday, April 14, 2012

"For example, I have direct deposit. I've checked to make sure my deposit has gone in on time, and the deposit is in the posted transactions on the third of the month. The following day, no change. But on the sixth of the month, a check I've written on the fifth suddenly displays in the posted section - BEFORE my direct deposit. Do you see the problem here?"

You didn't say what month this happened but I'm willing to bet it was March 2012. The problem with your reasoning is that the 3rd was a Saturday, banks do NOT post on the weekend. So your direct deposit dated for deposit on the 5th would have shown as available on Saturday the 3rd. When the bank did the processing on the night of the 5th, they would post per policy. Since you say the check posted before the deposit I believe that Compass does debits first and then deposits. So when they processed your check being a debit would come out and then your deposit would go in. The deposit was available for use but not to cover any transactions posting before it. So they only "ripoff" would be you writing checks on an account that didn't have the money to cover it.

#11 Consumer Comment

Ya Know !!!

AUTHOR: Golfer - (United States of America)

SUBMITTED: Saturday, April 14, 2012

Basic early education, add, subtract and what do you have. Can't get any simpler than that.

#10 Consumer Comment

The OP still doesn't get, probably never will.

AUTHOR: Southern Chemical and Equipment LLC - (USA)

SUBMITTED: Saturday, April 14, 2012

Managing a checkbook is such a simple task that so many people simply cannot comprehend.

It simply amazes me.

First of all, 2 people using the same checking account on a daily basis is the recipe for disaster here.

Minimize your ATM and Debit card usage. Use cash.

Communicate with each other on all transactions, and decide which one of you will manage the account.

Second, if you actually keep an accurate, up to date register, you would never have to even look at online banking to "check your balance". This is the root of your problems!

Go only by what your checkbook says!!

It is very clear here that you have developed very poor financial habits and do not have any discipline.

That is why you pay fees.

The posting order of transactions means absolutely nothing if you maintain an accurate register.

I cannot see why so many cannot comprehend this very simple concept.

And, I speak from experience, in over 30 years of multiple checking accounts, I have NEVER had an overdraft or NSF charge.

Never.

Therefore, I can say with absolute certainty that my method works.

You need to re-train yourself.

Get some professional financial counseling if you cannot manage this yourself.

Most banks actually offer free classes in managing your checkbook and finances.

#9 Consumer Comment

Quick question

AUTHOR: Jim Martin - (USA)

SUBMITTED: Saturday, April 14, 2012

Did you actually write the check on the 5th or did you post date the check for the 5th? There's a big difference. I find it hard to believe that you wrote a check on the 5th and it was already posted on the 6th. Most checks will take at least 2 or 3 days to post.

My guess is you post dated a check for the 5th and sent it out. Then, the company it was made out to sent it through, disregarding the date on the check, and it was processed before your paycheck. This is more believable than the bank actually going backwards in time and processing the check 2 days before you wrote it.

Of course, that's just speculation, but is it really that far from the truth?

Oh, and if you don't have Quicken on your computer, Excel works really well too. That's what I use for mine.

#8 Consumer Comment

That did not happen the way you claim it did

AUTHOR: coast - (USA)

SUBMITTED: Friday, April 13, 2012

"the deposit is in the posted transactions on the third of the month.. on the sixth of the month, a check I've written on the fifth suddenly displays in the posted section - BEFORE my direct deposit"

You are implying that the bank posted a check on the 3rd even though you wrote that check on the 5th. The date of deposit is stamped on the back of the check. If that date is after the date the check was posted then you would be able to prove an error by the bank.

#7 Author of original report

Clarification: Entitlement, no. Outrage, yes.

AUTHOR: FelineHostage - (United States of America)

SUBMITTED: Friday, April 13, 2012

The post I'm replying to said, in part:

"The posting of checks is not set it concrete until after they go through processing, usually starting at midnight each business day. You may be able to see (and take your snapshot) of some checks pending throughout the day. This are checks the bank has received and knows are going to process that evening."

I understand that. Compass has two portions, Pending and Posted. Pending debits are, as you said, not set in concrete. The amount of the pending debits will reflect in the available balance, but those transactions still have to process that evening. Posted debits are the ones that have already been through this processing. What I'm upset about is that Compass is not just rearranging the order of debits that are pending; it's rearranging debits have been POSTED - already processed.

For example, I have direct deposit. I've checked to make sure my deposit has gone in on time, and the deposit is in the posted transactions on the third of the month. The following day, no change. But on the sixth of the month, a check I've written on the fifth suddenly displays in the posted section - BEFORE my direct deposit. Do you see the problem here?

Look, when my husband or I screw up with our checking account, we expect to be penalized - it's just a fact of life. When you make a mistake, you pay for it.

But Compass' argument about protecting the customer is bogus. Everyone I know has overdraft protection, so checks are not going to be returned. Banks push OD protection hard, especially after recent legislation.

I'm not protesting Compass charging an NSF fee for an overdraft. I'm protesting Compass deliberately manipulating the order of debits, including already-posted debits, for the express purpose of extracting as many fees as possible from customers.

I have a regular check register. I use the online banking system to check the register. Anytime you have two people using one account, you need every backup possible. And since we have Compass, I have to check online every day to see what surprises the bank has in store for me.

Posting snarky or insulting comments to me does not change the fact that Compass Bank is embracing unethical practices.

#6 Consumer Comment

My favorite

AUTHOR: Ramjet - (U.S.A.)

SUBMITTED: Friday, April 13, 2012

This is actually my favorite line the the OP's post: In that letter, I instructed them to either.......

The OP actually thinks they have the ability to "instruct" the bank on their policies. Pretty funny.

#5 Consumer Suggestion

Simple solution. Maintain an ACCURATE checkbook register!

AUTHOR: Southern Chemical and Equipment LLC - (USA)

SUBMITTED: Friday, April 13, 2012

It amazes me how the simplest solutions are beyond comprehension of the masses.

Simple solution:

Maintain an accurate checkbook register.

Problem solved.

Guaranteed.

Online banking was NEVER intended to replace a manual checkbook register.

Online banking is a convenience only, and you CANNOT rely on it to provide you with an accurate available balance as common sense would dictate, the bank would have no way of knowing what checks you have written, or what electronic transactions you have authorized.

It seems like our younger generation has absolutely no idea of what a checkbook register is, or how to maintain a checking account.

This is a crying shame.

I had a checking account when I was 14 years old, so I could learn how to manage my money.

In high school, we learned how to maintain a checkbook register.

Do they not teach any of these basic skills in school anymore?

Our country is in trouble if this is the educational level and overall mentality of future generations.

#4 General Comment

My, aren't we just full of entitlement ...

AUTHOR: Striderq - (U.S.A.)

SUBMITTED: Thursday, April 12, 2012

It doesn't matter how you want the bank to post the checks. The banks can (by law) post them any way they want AS LONG AS they provide account holders with notification of the policy. The posting of checks is not set it concrete until after they go through processing, usually starting at midnight each business day. You may be able to see (and take your snapshot) of some checks pending throughout the day. This are checks the bank has received and knows are going to process that evening. However, when the processing starts the bank will put the transactions in order per their policy. Some banks post daily deposits first, others post the deposits last. All banks that I'm aware of will post the debits from largest to smallest. And yes, actually this is for customer convenience. Would you rather your mortgage payment get returned unpaid causing one fee or have two smaller grocery purchases be returned causing two fees. Most customers will accept the two fees to prevent the hassle of having a mortgage or car payment returned.However, if you properly maintain your register and not spend money not available in your account you won't cause yourself any fees.

Disclaimer: yes, I used to work for a bank but not this bank. However the only real difference in bank processing is whether the deposits go in he account before or after the debits come out. Keep the register balance positive and it doesn't matter how they post as you won't cause yourself the fees.

#3 Consumer Comment

Simple resolution

AUTHOR: coast - (USA)

SUBMITTED: Thursday, April 12, 2012

"I have a program (ScreenShot) on my computer" I have a program on my computer too. It's called Quicken. You may want to check it out.

"I've learned to check my account online daily" Maybe you should learn to maintain a check register.

To avoid overdraft penalties don't write checks against unavailable funds. Easy fix.

#2 Consumer Comment

Shocking..

AUTHOR: Robert - (U.S.A.)

SUBMITTED: Wednesday, April 11, 2012

- Wow that is shocking that they didn't respond. Too bad, because if that worked I would write them telling them that they are to immediately put $1000 in my account each and every day.

They never responded to my letter, and they continue to do exactly as they please.

- Actually they continue to do exactly as is stated in the terms of the account.

Now, I am going to give you a secret on how to avoid these NSF fees all together, and this not only works for them but ANY bank or credit union.

The first thing you have to do is stop using On-Line/ATM/Phone or any "automated banking" to manager your account. These systems were never meant as a way to manage your account. This is because the bank doesn't know what you have spent until they receive it, and in the cases of checks that may be anywhere from 2-3(or more) days before they get the check.

Next start using a Written Register. This is so that you can write down every transaction you make when you make it. This way you know what you have spent and don't have to rely on the bank. If you don't know how to use a register go into one of the branches and they will be glad to show you how to use it, they may even give you a register to use. Now, there is one part that you can use On-Line banking for. That is to verify that any deposits have been posted and are available.

This also has added benefits. You now have a record of what you spent so you can match what you have spent with what On-Line banking shows you have spent. Making any fraudulent charges stand out because you would not be expecting them.

Then perhaps the most important part. Never spend more than you have currently available in your account.

If you do the chances of you over drafting your account is practically zero.

#1 Consumer Comment

question

AUTHOR: Stacey - (U.S.A.)

SUBMITTED: Wednesday, April 11, 2012

What did you check register say your balance was?

Related Reports

07:47 PM

08:22 AM

12:27 PM

06:08 PM

09:17 PM

05:27 PM

07:09 AM

10:56 AM

11:36 PM

08:17 AM

01:48 PM

01:42 PM

12:01 PM

08:57 PM

07:29 PM

04:10 PM

12:03 PM

11:28 AM

07:51 PM

09:49 AM

08:34 AM

10:07 AM

10:06 AM

10:55 AM

Advertisers above have met our

strict standards for business conduct.